Report: Microsoft took 17 years to recover from the dot-com crash. Will history repeat for AI stocks?

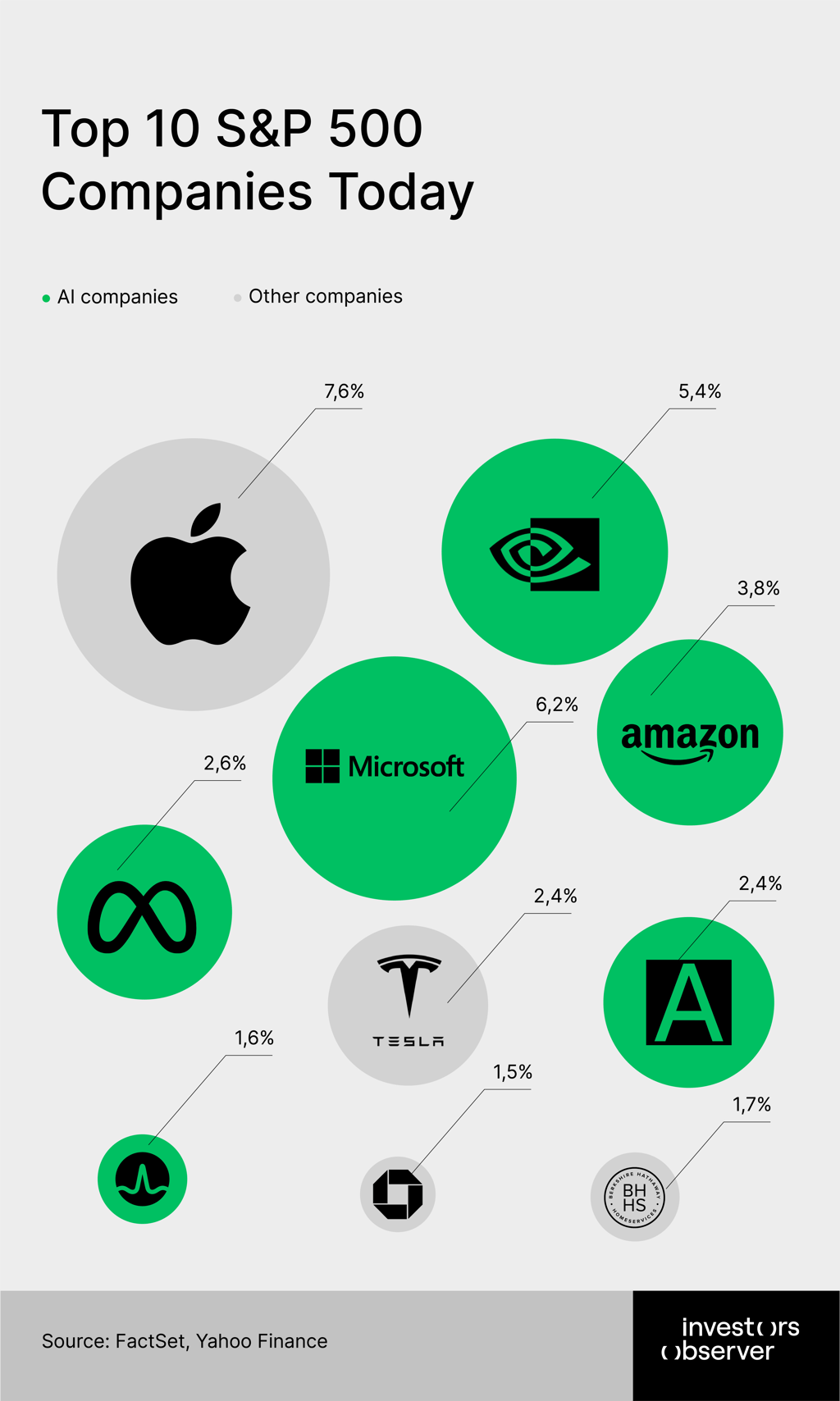

The S&P 500 is now in one of its most concentrated periods in history. The top 10 companies now make up 33% of the index’s total market capitalization.

This echoes the dot-com boom of the late 1990s not just because of the high concentration, but also because today’s biggest companies share similar traits.

During the dot-com peak in 2000s, 6 of the 10 largest firms were internet-related, while today, six of the top ten are AI-driven.

The question now is whether history is about to repeat itself, with similar consequences for investors and the broader market.

Key takeaways

- The S&P 500’s top 10 companies now make up 33% of the index’s total market capitalization – one of the highest levels on record.

- Just as the internet fueled the 2000s bubble, AI is propelling today’s market rally.

- “AI concentration” – top 6 AI development stocks – Nvidia, Microsoft, Amazon, Meta, Alphabet, Broadcom – now represent 23% of the S&P 500, surpassing dot-com levels.

- “Internet concentration” – top 6 internet stocks – made up 15% of the S&P 500 at the peak of the dot-com boom.

- Only two "internet-era" companies returned to their dot-com highs, and it took them more than a decade. What helped those companies was that both were already well-established players before the dot-com boom.

- Today’s leaders generate profits, but some – like Nvidia – have high valuations based on continued rapid growth.

- Market cycles are inevitable: AI is a long-term trend, but no sector dominates forever – investors should prepare for potential shifts into other industries.

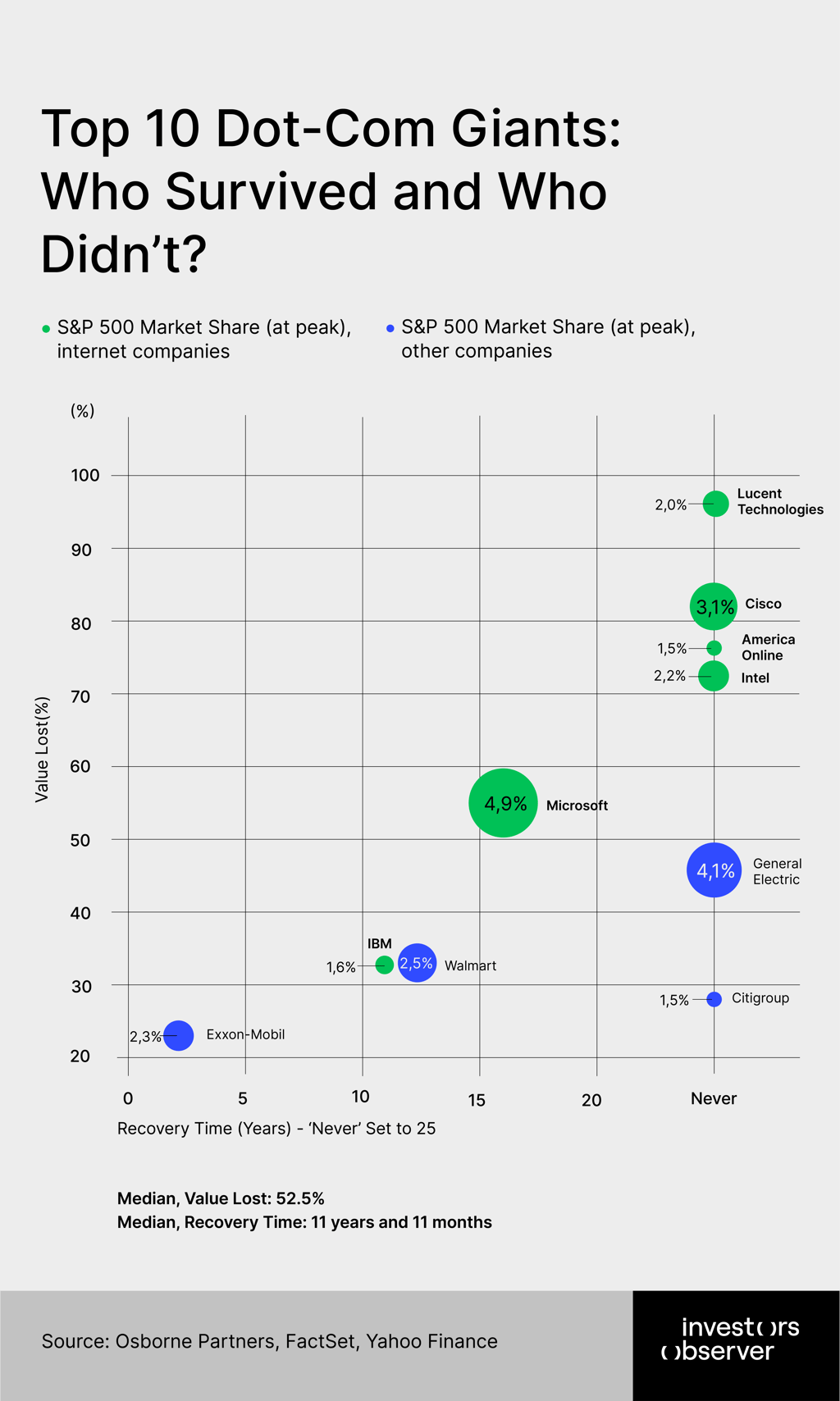

Top 10 dot-com giants and who survived

At the peak of the dot-com bubble, 6 of the 10 most valuable U.S. companies were internet-focused firms. Then the crash wiped out trillions. Some of them took years to recover, and others never did.

Microsoft

The company lost 58% of its value and took 16 years and 8 months to fully recover.

Microsoft was at the height of its power during the dot-com boom, dominating PCs with Windows and Office. But just as the bubble burst, the company was hit with a major blow: On March 20, 2000, Judge Thomas Penfield Jackson ruled Microsoft guilty of monopolization, triggering a one-day 15% stock crash.

The company struggled for more than a decade. Under Steve Ballmer (2000–2014), it failed to keep up with the internet and mobile shifts. The turnaround didn’t come until Satya Nadella refocused Microsoft on cloud computing and enterprise software. That shift, plus embracing open-source tools and subscription models, helped it become one of the world’s most valuable companies again, but it took nearly 17 years.

General Electric

The company lost 47% of its value and never recovered.

GE was the crown jewel of American industry during the '90s under Jack Welch. But when the bubble burst, Welch handed the reins to Jeff Immelt, who inherited a minefield: the dot-com collapse, 9/11, and an increasingly fragile balance sheet.

Immelt’s tenure was defined by big swings that didn’t pay off. He doubled down on GE Capital before the 2008 crisis, made disastrous energy acquisitions, and overpromised on growth. By the time Larry Culp took over in 2018, GE was bleeding cash and had to spin off major divisions. GE Vernova and GE Aerospace are the remains of a once-dominant conglomerate.

Cisco Systems

The company lost 82% of its value and never fully recovered.

Cisco was the backbone of the internet – literally. It built the routers and switches that powered the web. At its peak, it was briefly the most valuable company in the world.

But Cisco was also the face of dot-com excess. Its valuation collapsed by over 80% after the bubble burst. While the company still sells networking hardware and has expanded into cybersecurity and cloud infrastructure, it never regained its former valuation. Today, Cisco is a stable tech company, but it’s no longer at the forefront of innovation as it was back in the day.

Walmart

The company lost 37% of its value and took 12 years and 7 months to fully recover.

Walmart didn’t ride the dot-com hype train, but it still took damage. The rise of Amazon and the shift to e-commerce forced the retail giant to evolve.

Over the past two decades, Walmart has heavily invested in digital services, online grocery, and integrating physical and digital operations. It may have been late to the party, but it caught up, and remains a formidable player in the retail space.

Exxon Mobil

The company lost 24% of its value and took 3 years and 10 months to fully recover.

Exxon was largely spared the dot-com bloodbath. As an oil giant with tangible assets and global reach, it avoided the inflated valuations plaguing tech stocks.

That said, Exxon has faced plenty of headwinds since, from climate activism to the clean energy transition. Its quick recovery from the dot-com crash didn’t shield it from the deeper energy disruption that came later.

Intel

The company lost 72% of its value and never recovered.

Intel was the engine behind the PC revolution, and that made it a dot-com favorite. But when the bubble burst and PC sales slowed, Intel took a hit. It also lost its manufacturing edge over time.

The company has since struggled to keep up with AMD and newer players using ARM architecture. Intel is still a key name in semiconductors, but it’s no longer the dominant force it once was.

Lucent Technologies

The company lost 97% of its value and never recovered (was restructured).

Lucent was one of the hottest telecom stocks of the dot-com boom, but the collapse in infrastructure spending wiped it out. In 2006, it merged with France’s Alcatel to stay alive. A decade later, Nokia acquired the combined company.

Lucent no longer exists. It’s a classic example of how even market leaders can vanish if they don’t adapt fast enough.

IBM

The company lost 36% of its value and took 11 years and 2 months to fully recover.

In the years since, IBM has undergone multiple reinventions. It pushed into cloud, AI, and business services. It spun off its infrastructure business (Kyndryl) and doubled down on hybrid cloud with Red Hat. It remains a legacy player, but one that has survived every tech wave so far.

Citigroup

The company lost 28% of its value and never fully recovered.

Citigroup wasn’t a tech stock, but it was deeply exposed to dot-com valuations through its investment banking business. After the crash, it stumbled into a far bigger disaster: the 2008 financial crisis.

Citigroup required a massive government bailout and has spent years selling off non-core businesses. It still exists but never recovered its market cap. It’s now a cautionary tale about the limits of scale and complexity.

America Online

The company lost 76% of its value and never recovered (was restructured).

AOL was the poster child of the internet boom. At its peak, it merged with Time Warner in what’s widely seen as the worst corporate deal ever.

When broadband overtook dial-up and the promised synergies never materialized, AOL’s business collapsed. It was spun off in 2009, sold to Verizon in 2015, and eventually ended up in private equity hands.

Today, AOL is just a footnote in digital media history—a symbol of how fast tech giants can rise and fall.

The S&P 500’s new reality: AI firms rule the top 10

Nvidia, Microsoft, Amazon, Meta, Alphabet, and Broadcom are some of the most prominent players in the development of AI technologies.

These companies are involved in areas such as machine learning, cloud computing, and semiconductor production, all of which contribute to the expansion of AI capabilities.

The market valuations of these companies are closely linked to the growing expectations around AI. As AI adoption accelerates, there is significant investor interest in companies positioned to benefit from this shift.

However, the extent and speed of AI’s impact on the market remain uncertain.

While these companies are heavily involved in AI, the future trajectory of AI growth, as well as its economic and technological effects, are still subject to change. The valuations of these companies may fluctuate as the market adapts to evolving AI trends.

Dot-com lessons for today’s AI firms

The dot-com bubble collapse left a lasting mark on the tech industry, with many once-dominant companies never fully recovering. Lucent and Cisco, for instance, saw their market value evaporate, while Microsoft took nearly 17 years to surpass its dot-com peak.

The lesson? Even industry leaders can falter when valuations outpace reality, and what once seemed like unstoppable momentum can reverse overnight.

Fast forward to today, and AI stocks – led by Nvidia, Alphabet, and Microsoft – are at the centre of a new tech boom. Unlike many dot-com-era firms, these companies are generating real profits, but investor enthusiasm has pushed some valuations to levels that assume years of uninterrupted growth.

Nvidia, in particular, has seen its market cap soar, only to experience a historic $600 billion single-day loss when investors questioned the sustainability of its dominance. The sell-off, triggered by DeepSeek’s announcement of a cost-efficient AI model, revealed the fragility of hype-driven valuations.

That said, the broader market is not displaying the same level of excess. While AI leaders command premium prices, many other tech stocks trade closer to historical norms, suggesting more reasonable valuations outside the AI frenzy.

For retail investors, this means there may be opportunities in underappreciated sectors that offer growth without the risks of overinflated AI bets.

The AI revolution is undoubtedly reshaping industries, but history warns against unchecked optimism. The question is whether today’s market leaders can sustain their dominance without facing the same pitfalls that toppled their dot-com predecessors.

As the recent Nvidia turmoil has shown, even the strongest companies are not immune to disruption.

Methodology

“Stock market concentration” refers to the percentage of the S&P 500’s total market cap held by its 10 largest constituents as of April 7, 2025

“AI concentration” refers to the percentage of the S&P 500’s total market cap held by AI buildout companies among the 10 largest constituents as of April 7, 2025

“Internet concentration” refers to the percentage of the S&P 500’s total market cap held by internet buildout companies among the 10 largest constituents at the peak of the dot-com bust in 2000.

"Value lost" refers to the difference between a stock's peak price during the dot-com boom and its lowest point in the aftermath of the dot-com bust, more specifically between the start of 2000 and the end of 2001.

"Recovery time" measures how long it took for the stock to surpass its dot-com peak, indicating the time required for the company to recover from the market crash.

All market data, except for “internet concentration”, is as of Apr 7, 2025.

Sources

- Factset market data

- Yahoo Finance market dat