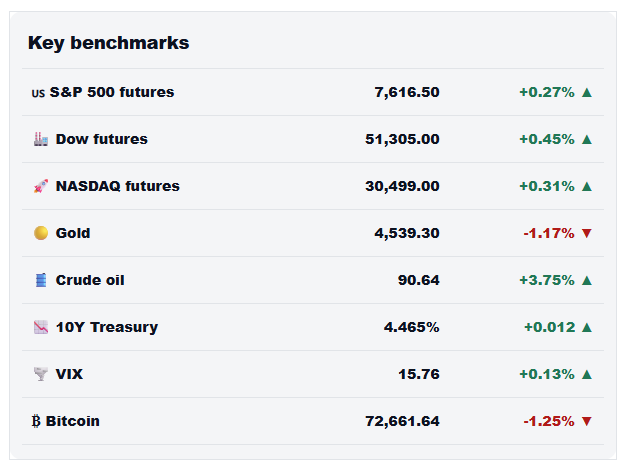

Stocks most expensive in history

Morning Observers,

U.S. stocks are officially the most expensive in history. By nearly every mainstream valuation measure, today’s prices have passed the dot-com peak and pre-Great Depression mania.

Three reasons (among others).

First, Trump looks boxed into a corner on Iran and all the signs suggest he will try to reach some kind of deal one way or another. That means the doomsday energy scenario is off the table, at least for now.

Second, corporate America is still making way more money than expected. The percentage of companies beating earnings this season is the highest in nearly two decades.

And although valuations have stretched lately, most of this year’s stock market gains have come from rising earnings.

Finally, there’s speculation that new Fed chair Kevin Warsh will look past summer inflation and keep rates lower.

During his Senate confirmation hearing, Warsh called for “regime change” at the Fed, including how it sets rates.

Although he has criticized the Fed’s flexible Covid-era inflation framework, which allowed inflation to temporarily run above target, he also wants the Fed to rethink how inflation is measured.

The Wall Street Journal reported that Warsh is looking at indicators like the trimmed mean inflation rate, which is currently lower than core inflation.

Last year, he also slammed Powell for ignoring AI-driven productivity as a major deflationary force. So the bet is that he may use that same argument to push back against more rate hikes.

“We expect him to argue that the last thing good policy would do is work to restrain the investment today that might represent tomorrow’s disinflation,” UBS economist Jonathan Pingle said in a recent note.

Of course, there’s a counterargument to each of these positives, but here's a fun fact.

Since 1988, the S&P 500 has been higher one year after hitting an all-time high nearly 85% of the time.

85% of the time!

— Dan Runkevicius, Editor

Five things to know before opening bell

🚀 SpaceX targets $1.8 trillion valuation

Elon Musk’s SpaceX is targeting a valuation of roughly $1.8 trillion ahead of its planned initial public offering. While the final figure has yet to be determined, Musk has shown little interest in lowering expectations, putting the space and artificial intelligence company on track for what could become one of the largest public market debuts in history.

💾 Micron gets another major Wall Street upgrade

Less than a week after UBS tripled its price target on Micron, Susquehanna followed suit on Friday, lifting its target to $1,750 from $600. Micron, which produces memory chips including DRAM and NAND flash storage, has become one of the biggest beneficiaries of the AI boom as cloud providers and developers lock in long-term supply agreements to secure critical semiconductor capacity.

🍁 Canada slips into a technical recession

Canada’s economy contracted at a 0.1% annualized rate in the first quarter after shrinking 1% in the previous quarter, pushing the country into a technical recession. Economists largely blame growing uncertainty surrounding U.S. trade policy, which has caused businesses to delay investment decisions and weighed on export activity. Given Canada’s heavy reliance on the U.S. market, even small shifts in the trade outlook can ripple through the broader economy.

⛽ U.S. distillate inventories fall to a two-decade low

America’s stockpile of distillate fuels, which includes diesel and heating oil, just fell to its lowest level since 2003. Inventories dropped by 2.1 million barrels in the week ending May 22 as strong exports and ongoing disruptions around the Strait of Hormuz reduced supplies. Diesel is often viewed as a proxy for economic activity because it's used to move goods across the economy, meaning sustained shortages could put upward pressure on transportation costs and consumer prices.

💴 Japan’s currency intervention keeps falling short

Japanese authorities have spent roughly 12 trillion yen, or $74 billion, supporting the yen in currency markets, but the effort has done little to reverse its decline. The dollar remains above 159 yen, a level many economists view as likely to trigger further intervention. A weaker yen raises import costs for energy and food, fueling inflation and squeezing households, which is why policymakers are trying to slow the currency’s slide.

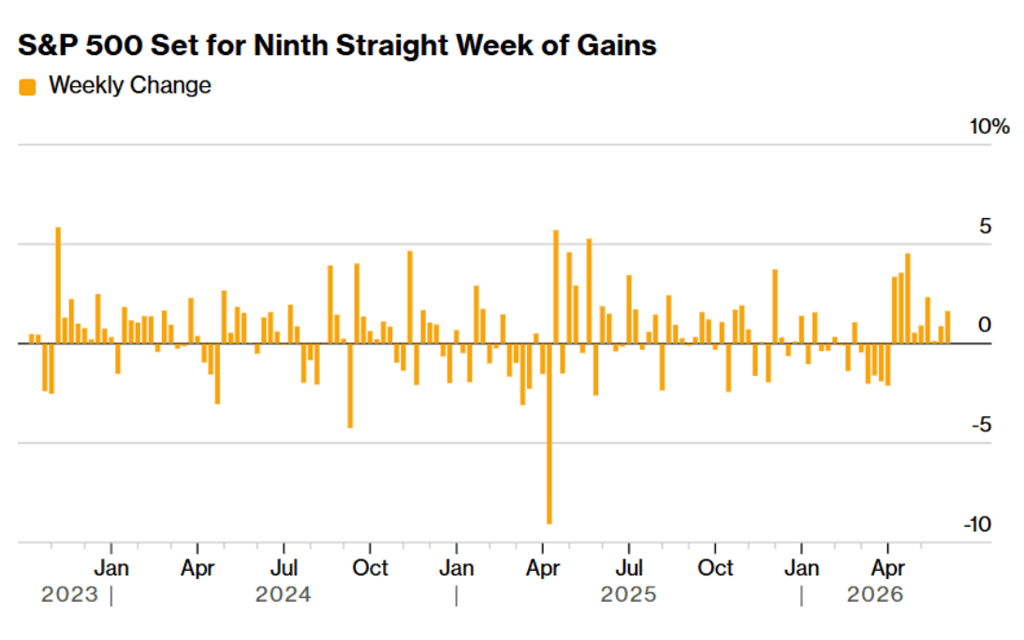

Sell in May? Wall Street did the opposite

For decades, Wall Street lived by a simple adage: Sell in May and walk away. And historically, that’s what investors tended to do.

But not this year.

Stocks have just delivered one of their strongest stretches since World War II, despite war, diplomatic chaos, and surging inflation.

Nine weeks. Almost nobody gets to ten

The S&P 500 has now risen for nine consecutive weeks, climbing above 7,500 and more than recouping the losses that followed the start of the war in Iran in late February.

The speed of the rebound suggests investors quickly abandoned fears of a broader regional conflict.

Semiconductors did most of the heavy lifting. The Philadelphia Semiconductor Index surged 69% during the streak, suggesting this rally wasn’t driven by broad economic optimism alone. AI did a lot of the work.

What’s remarkable is that the move occurred during one of the weakest periods for stocks. Since 1964, May has produced average returns of just 0.3%, making it one of the least rewarding months on the calendar.

By comparison, stocks have posted average returns of 1.6% in November, 1.2% in December, and 1.5% in April.

History says don’t get too comfortable

According to Bespoke Investment Group, a nine-week winning streak has occurred only ten other times since World War II. But only four of those streaks extended to a tenth week.

The bigger issue isn’t whether stocks can climb for a tenth week. It’s that the rally has already priced in the idea that the worst-case scenario is off the table. So future gains may be harder to find.

That’s one reason some strategists, including RIA Advisors’ Lance Roberts, expect profit-taking and portfolio rebalancing to emerge in June.

After a run this strong, many investors simply have more gains to protect.

📌 Bottom line: Nine-week winning streaks rarely last. The real test isn’t whether stocks pull back, but whether buyers continue to show up when they do.

$4.8 billion reason Costco beats S&P 500

Costco is one of the strangest businesses in America.

Most retailers spend decades trying to squeeze an extra percentage point of margin from suppliers, logistics, and pricing. Costco does the opposite.

It deliberately limits how much profit it can make on the products it sells.

The retailer that doesn’t optimize for retail

A recent price comparison from venture capital firm a16z found Costco’s prices run 21.4% below Walmart on average nationwide. That's cheaper than BJ’s (-21%), Aldi (-8.3%), and every major traditional grocer.

The gap becomes even more striking further down the list. Target’s prices are nearly 6% above Walmart’s. Kroger is almost 15% higher. Trader Joe’s is 25% higher. Whole Foods sits nearly 40% above Walmart.

Normally, a retailer would see that spread and start raising prices. Not Costco.

The company caps markups at roughly 14% on national brands and 15% on Kirkland products. Any item priced above those thresholds doesn’t make it onto the shelf.

By retail standards, that’s an extraordinary amount of profit to walk away from. Unless the shelves aren’t where the profits come from.

The customer-retention expense

While most retailers make money when customers buy something, Costco makes money when customers renew.

Its membership fees generated $4.8 billion last year. That's only a tiny fraction of revenue, but it accounts for the majority of operating profit. More importantly, renewal rates exceed 90%.

From this perspective, Costco’s 21% price advantage is a retention strategy. And that's why competitors struggle to follow.

Walmart and Kroger depend on margins earned at the shelf. Costco can subsidize those margins because its most important revenue stream begins before shoppers put anything in their carts.

For shareholders, the result has been one of the best business models in retail. Costco shares have returned more than 150% over the past five years, while the company has increased its dividend for 23 consecutive years.

What looks like a sacrifice at the checkout counter has produced one of the best-performing retail stocks of the past decade.

📌 Bottom line: Costco’s low prices are a marketing expense. Every discount helps convince customers to renew, and every renewal helps fund the next discount. That’s what makes the model so difficult to replicate.