SpaceX joins Nasdaq 100!

Morning Observers,

Nasdaq changed two fundamental rules earlier in May to get SpaceX into the index today.

The first, and the most well-known, is the timeline known as the “seasoning period.”

After Nasdaq introduced its “Fast Track,” SpaceX got an exception allowing it to join the index in 15 days, rather than waiting at least until October like ordinary stocks.

The second change is less known but far more impactful. Before the rule change, Nasdaq required every listed company in the index to have a free float of at least 10%.

That means every company in the index had to have at least 10% of its shares freely available to public investors.

That rule is now waived entirely, and SpaceX is getting in with one of the smallest pools of tradable shares relative to its size.

SpaceX is listed with around 4% of its total outstanding shares, which is roughly ONE-ELEVENTH of the average free float mega caps IPOd with in the past decade.

And here’s the irony in this whole situation.

The company gets special treatment and is weighted like a $2 trillion company, yet it's selling only a teeny-tiny slice of the company.

(Under the new rules, SpaceX will be weighted at 3x its free float.)

This matters because the bigger weight assigns more passive money to the company, while the smaller float means all that money is chasing a small pool of shares.

SpaceX is already down more than 10% from its day-one pop, meaning marginal buyers are disappearing. Perfect timing for another passive infusion of capital.

Let's dig in!

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🚢 LNG tanker hit near Strait of Hormuz

Tensions in the Strait of Hormuz flared again after a laden liquefied natural gas carrier was struck by a projectile near the Omani coast while exiting the waterway. The attack has rattled shipowners and is already testing a U.S.-Iran agreement meant to halt attacks in the strait.

📈 Dip buyers sent tech stocks higher, then Samsung dragged them lower

A rebound in major chipmakers lifted U.S. stocks yesterday. The Philadelphia Semiconductor Index jumped 2.2%, recovering some of last week’s losses. The S&P 500 gained 0.7%, while the tech-heavy Nasdaq climbed 1.1%. This morning, futures are down after a Samsung-led sell-off during the Asian trading session.

🤖 Foxconn posts another AI-fueled sales surge

Demand for AI hardware remains strong. Hon Hai Precision Industry, better known as Foxconn and one of Nvidia’s largest suppliers, reported a 40% jump in quarterly sales to NT$2.51 trillion (about $79 billion), topping analyst estimates as AI servers and cloud products continued to drive growth.

🏢 U.S. service sector loses momentum

The U.S. services sector, which accounts for roughly three-quarters of the economy, expanded at a slightly slower pace in June. The ISM Services PMI slipped to 54.0 from 54.5 in May, remaining comfortably above the 50 level that separates expansion from contraction. Meanwhile, the Business Activity Index, which measures current business output across the services sector, fell to 55.4 from 57.7, signaling growth is moderating.

💵 Dollar strength persists

The U.S. dollar extended its gains yesterday as investors continued to price in the possibility of a Federal Reserve rate hike this year. The U.S. Dollar Index (DXY) rose 0.2% to trade above 101, strengthening against the euro, while the Japanese yen slid to another four-decade low.

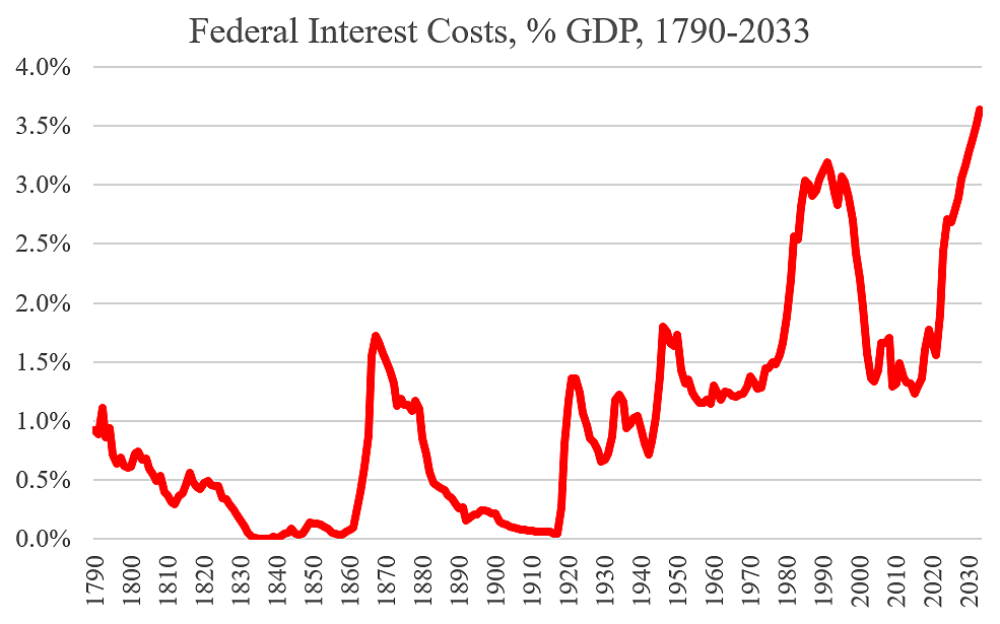

DOGE died before the 4th of July

July 4, 2026, wasn’t just America’s 250th birthday. It was also supposed to mark the end of DOGE, Elon Musk’s ambitious effort to shave more than $1 trillion off the federal deficit.

The deficit won

America’s national debt has now surpassed $39 trillion, while interest payments are projected to exceed $1.03 trillion in fiscal 2026, turning debt service into one of the largest line items in the federal budget.

At this level, servicing yesterday’s spending starts competing with today’s priorities.

Even institutions that rarely use dramatic language are sounding the alarm.

Stanford’s Institute for Economic Policy Research calls the current path “unsustainable,” warning that it will eventually require an “ahistorical adjustment” to taxes, spending, or both.

The uncomfortable reality is that deficits have become politically easier to expand than to reduce. The skeptics say DOGE never really stood a chance in the first place.

When bondholders revolt

Congress can ignore economists, but it can’t ignore bondholders.

When investors lose confidence in Washington’s fiscal discipline, they demand higher yields to finance the government’s borrowing. The bond market has started sending that message.

By the end of June, Treasury yields had posted another quarterly increase. The 10-year yield rose 0.11 percentage point to 4.42%, while the two-year yield climbed 0.339 percentage points, its largest quarterly jump since 2024.

Most of that jump came from the premium rather than inflation expectations.

📌 Bottom line: DOGE’s failure matters because it suggests there may be no political constituency capable of shrinking America’s deficit. The trillion-dollar question now is where bondholders draw the line.

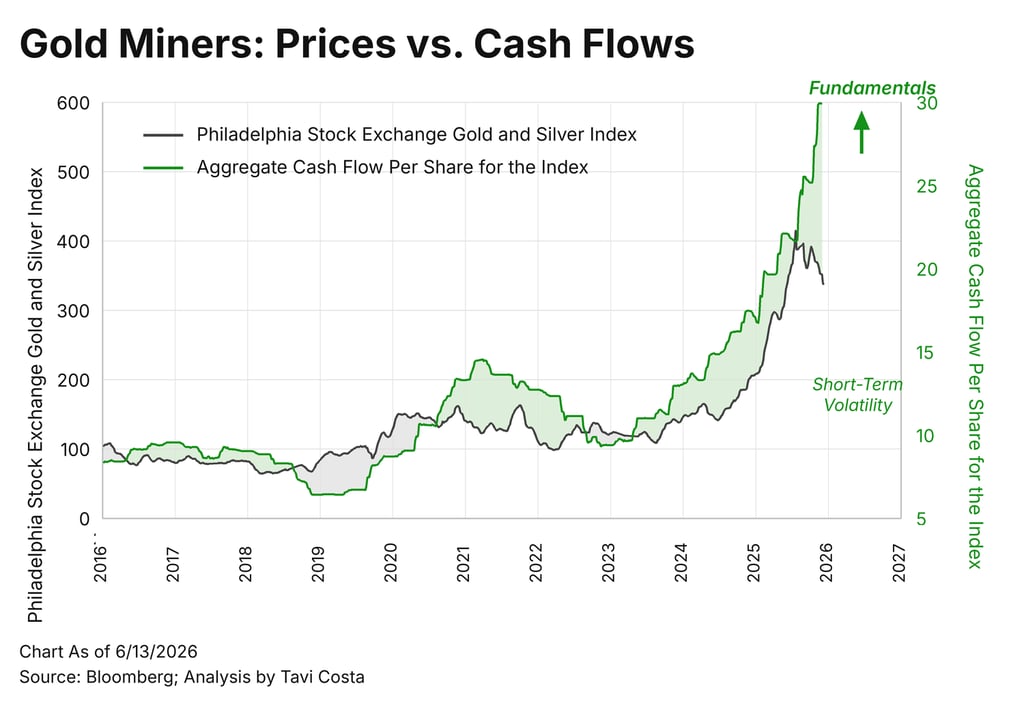

Gold miners are quietly becoming cash machines

Is the debate over whether gold has peaked a textbook case of missing the forest for the trees? Gold miners have rarely been this profitable, yet their stocks are acting as if the boom is over.

Gold miners are still printing cash

Azuria Capital founder Otavio Costa recently compared gold mining stocks to the sector’s aggregate cash flow per share, which measures how much cash mining companies generate.

His analysis shows aggregate cash flow per share has roughly tripled since 2023.

Even after gold’s pullback, miners remain far more profitable than they were just a few years ago because production costs have risen much more slowly than gold prices.

Stocks have corrected more than the business has

The recent selloff has pushed gold mining stocks into correction territory.

Since the start of the year, the VanEck Gold Miners ETF (GDX) is down 8.5%, the VanEck Junior Gold Miners ETF (GDXJ) has declined 10%, and the iShares MSCI Global Gold Miners ETF (RING) has fallen 9%.

Although all three ETFs remain up roughly 50% over the past year, this is not simply a case of front-loaded buying unwinding. Many of the companies inside these indexes continue to produce historically strong cash flows.

In other words, either stock prices are anticipating a brutal reversal, or the sector is increasingly undervalued relative to fundamentals.

📌 Bottom line: If gold merely holds near current levels, the recent pullback may end up looking more like a short-term bump than the start of a lasting downturn.