South Korea goes all-in on memory chips

Morning Observers,

The AI memory chip deficit is so bad that South Korea is changing its whole industrial policy around it.

South Korean president Lee Jae Myung announced this morning that Samsung and SK Hynix are planning to spend about $518 billion to build four new semiconductor fabs.

The plan is to double DRAM production around Seoul while building out the rest of the AI supply chain across the country as part of a regional development strategy.

He also wants to add 18.4 gigawatts of AI data-center capacity by 2035, which will require roughly 18 big nuclear reactors’ worth of power.

That means this push will also expand into energy because existing chip fabs around Seoul are already hitting electricity and water limits, and Lee said Korea needs new sources of power across the country.

Let’s just put it this way…

This is a country planning hundreds of billions in chip fabs, new memory hubs, new packaging centers, data centers, new power infrastructure, and an entire industrial policy and regional development plan around the AI supply chain.

These kinds of mega-projects don’t happen for no reason. But also these are exactly the kinds of mega-projects that tend to happen near the top of an investment cycle.

In the dot-com era, the ChatGPT moment happened around 1996 with a technology called Wavelength Division Multiplexing (WDM), which allowed multiple wavelengths, or data streams, to travel through a single fiber instead of just one.

That dramatically increased the bandwidth and cost-efficiency of fiber optic infrastructure, convincing investors that the internet was real.

In the next five years, telecoms poured over $500 billion into laying fiber optic cables, adding switches, and building wireless networks, most of which was debt-financed and frontloaded.

After the dot-com bust, dreams of internet bandwidth "tripling every few months" quickly unraveled, leaving behind a glut of unused fiber that was later dubbed “dark fiber.”

By various estimates, 85% to 95% of fiber laid in the ’90s remained unused after the bubble burst.

- In 1999, bandwidth demand was “insatiable” vs. today’s memory chip crunch being called a “hundred-year flood”

- Internet bandwidth was supposed to "double every three months" vs. AI compute is supposed to double every four to seven months

- Every company was supposed to become an internet company, and every middleman, including real estate agents and travel agents, was supposed to get disintermediated vs. half of white-collar entry-level jobs will now be gone in a few years

Nobody doubts AI will change the world. The real question is whether it can be adopted on the timeline priced into the market.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🛢️ Oil resumes slide as Hormuz fears ease

Oil prices extended their decline late last week, with U.S. crude falling back below $70 a barrel and Brent slipping under $72 as tanker traffic through the Strait of Hormuz continued to normalize despite lingering tensions between Iran and Israel. Adding to the pressure, Saudi Aramco is expected to sharply cut the official selling price of its flagship Arab Light crude for Asian buyers.

🔻 Chipmakers cool after AI surge

Semiconductor stocks ended the week more than 6% lower as investors questioned whether the AI-fueled rally had run too far, too fast. The Philadelphia Semiconductor Index has now fallen more than 8% from its recent record high, though it remains up roughly 87% over 2026. The pullback suggests investors are becoming more selective after one of the market’s strongest runs.

🚢 U.S. trade deficit hits 14-month high

America’s goods trade deficit widened to $105.8 billion in May, the largest in 14 months, as businesses accelerated imports while exports weakened. Economists believe companies rushed to secure inventory ahead of potentially larger disruptions and higher energy costs stemming from tensions in the Middle East. Because imports subtract from GDP in the national accounts, the wider trade gap prompted several economists to lower their second-quarter U.S. growth estimates.

🚀 SpaceX gives back post-IPO gains

After a blockbuster market debut that briefly pushed shares above $200, SpaceX stock has fallen back near its IPO price of $150. The retreat reflects cooling investor enthusiasm following the initial excitement surrounding the listing, although the company still commands a market capitalization above $2 trillion, keeping it among the world’s most valuable publicly traded companies.

🙂 Consumer sentiment rebounds, but inflation fears linger

U.S. consumer sentiment improved modestly in June as falling oil prices lifted confidence from May’s record low, according to the University of Michigan’s latest survey. The consumer sentiment index rose to 49.5 from 44.8, but inflation concerns remain elevated. Consumers now expect prices to rise 4.6% over the next year, suggesting households still anticipate a challenging inflation environment despite recent improvements.

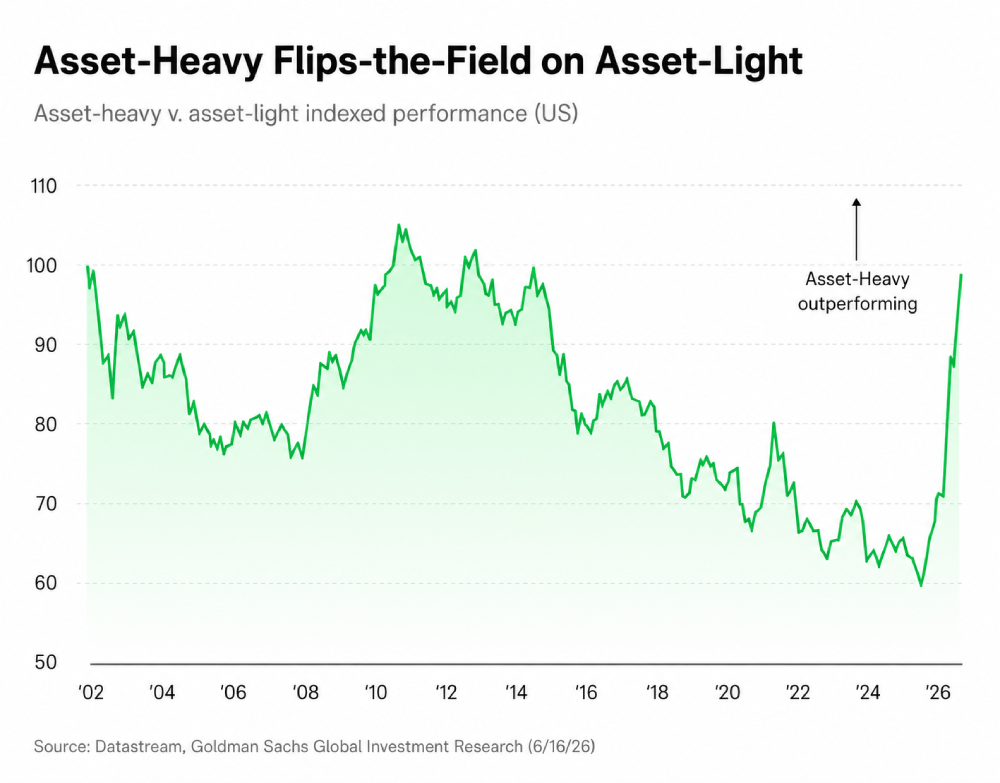

The U.S. stock market is getting “heavier”

For more than a decade, the stock market rewarded companies that needed very little to grow, like software companies. They could generate billions without building factories or power plants.

And when you have companies where every marginal customer adds little to no operating costs, businesses built on physical assets gradually fell out of favor.

This year that logic has started to reverse. Investors are now pouring billions into companies building physical infrastructure and dumping software.

Why factories are back in favor

In a recent analysis, Goldman Sachs grouped companies into two camps.

Asset-light businesses are mainly software and internet companies. Asset-heavy companies own factories, data centers, warehouses, power equipment, and other physical infrastructure.

Its index comparing the two groups has climbed from about 60 at the start of the year to nearly 100, recovering to levels not seen in more than a decade.

In other words, years of underperformance by asset-heavy companies have almost completely disappeared. The shift reflects the enormous amount of money being spent on building AI infrastructure.

The trend extends beyond public markets. Research from Andreessen Horowitz found that investors are also directing more capital toward “real-world” technologies in private markets, including robotics and other infrastructure-intensive businesses.

AI’s construction phase

The shift isn’t just showing up in individual stocks. ETFs that invest in infrastructure and industrial companies have outperformed the S&P 500 and many technology funds this year:

- Global X U.S. Infrastructure Development ETF (PAVE) is up 24%

- iShares U.S. Infrastructure ETF (IFRA) has gained 20%

- Vanguard Industrials ETF (VIS) has returned 17%

📌 Bottom line: Goldman’s data suggests one of Wall Street’s longest-running trends is beginning to reverse. If asset-heavy companies continue closing the gap, portfolios concentrated in software may lag the broader market.

The bond market is quietly calling the Fed’s bluff

Wall Street is increasingly betting the Fed will have to raise rates to contain inflation. But one overlooked corner of the bond market suggests the opposite may eventually happen.

If borrowing costs stay this high for much longer, the next move may be a rate cut instead.

It would mark another bizarre twist in a saga that has investors guessing whether policymakers will prioritize price stability or economic growth.

The yield that matters most

Everyone watches the Fed’s benchmark rate. Fewer watch real yields, which is a return investors earn after accounting for inflation.

Real yields measure the true cost of borrowing. When real yields rise, that means debt costs are rising faster than nominal household incomes and earnings.

That means mortgages become harder to afford, companies spend more on debt servicing, and Washington pays more to finance its deficits.

The 2-year real yield recently climbed to roughly 2.1%, its highest level in about two years. For an economy carrying record debt, that’s arguably more important than another quarter-point rate hike.

“This is exactly how you break an economy drowning in debt,” wrote Azuria Capital founder Otavio Costa.

According to Costa, if inflation-adjusted borrowing costs stay this high, they could slow spending and economic growth enough to push the Fed toward rate cuts instead.

A more skeptical look

Economist Peter Schiff shares a similar view. “The longer the Fed waits to hike rates,” he recently argued, “the more likely the next move is a cut.”

His reasoning is that if the Fed waits too long, it may eventually be forced to respond to slowing economic growth or falling asset prices as political pressure mounts.

That may also explain why gold mining stocks have remained resilient despite elevated real yields.

Normally, rising real yields are bad news for gold and gold miners because investors can earn higher inflation-adjusted returns in Treasurys instead.

Gold miners’ recent strength suggests some investors are already looking beyond today’s inflation concerns and positioning for lower rates down the road.

📌 Bottom line: Markets may be pricing in two different futures at once: higher rates in the near term, but lower rates once higher borrowing costs begin to weigh on an economy built on debt. Watching real yields may offer a better clue about which story wins.