S&P 500 and chill or not

Morning Observers,

S&P 500 and chill, and earn 10% annually until you retire? There’s a 96% chance that it won’t happen.

If you want to model when you can retire, or what your net worth might look like some time from now, the textbook formula is simple.

You take your current investments, add expected contributions, and compound everything forward based on historical returns.

There’s just one problem: average returns almost never happen.

That magical 10% number is the average S&P 500 return since 1926. Not 10 years, 20 years; not even an average human lifespan. It’s a full century.

Flash news: few people live that long, let alone invest that long unless they are born with great genes and a trust fund.

So the real question is: what are the chances that the average investor actually averages 10% over their investing lifespan? Short answer: very slim.

Over the past 100 years, the S&P 500 has finished within 2 percentage points of its long-term average only four times. So if we define “average-ish” as roughly 8% to 12%, the market missed that range in about 96% of calendar years.

Now that doesn’t mean your return will necessarily be lower.

If we take 20-year rolling returns (which is my favorite timeframe because 20 years is more or less how long the average investor can realistically take risk with an all-stock portfolio), the S&P 500 earned more than its long-term average 56% of the time.

But there’s also been 20-year periods when stocks averaged 2% before inflation and ended up deep in the red after inflation.

For example, it took the S&P 500 more than 20 years to break even on inflation after the 1970s inflation shock, and more than 15 years after the dot-com bust.

That doesn’t happen often, but it does happen. And it likely will happen again at some point.

I belong to a generation of investors that hasn’t really seen a true crisis as adults. Every bear market, every recession came with some kind of backstop.

And now there’s always this quiet comfort in the background: if things get really bad, someone will step in, whether it’s the Fed, Trump, or whoever else is in charge at the time.

And it feels like a whole generation of investors (myself included) has been raised on training wheels.

That idea keeps forcing me to ground myself in one uncomfortable truth: the regime we grow up in as investors, and take for granted, is just a phase in the grand scheme of things.

Things can change fast, and so can “average” returns.

- Dan Runkevicius, Editor

Five things to know before opening bell

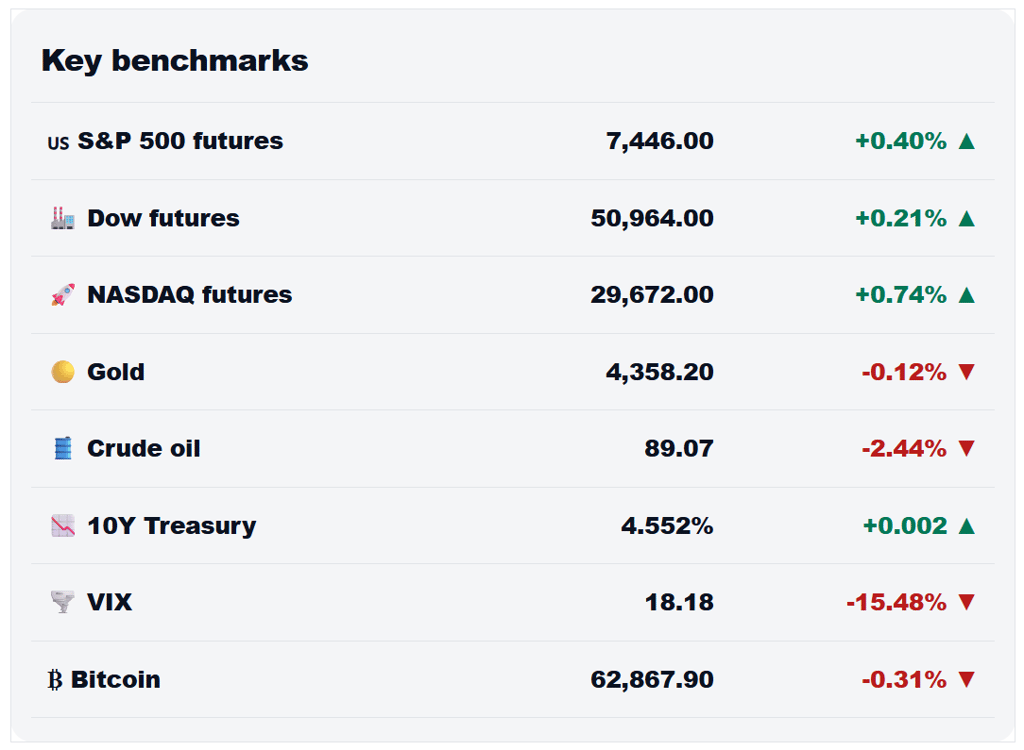

📈 Stocks rebound from worst rout of the year

U.S. stocks started the week higher after last week’s selloff. The S&P 500 rose by 0.3%, recovering from its worst rout of the year, while the Nasdaq 100 gained 0.9% after posting its biggest weekly decline since April 2025. Large technology stocks led the rebound, with Nvidia helping lift a basket of Mag 7 companies.

🤖 Apple signals long-awaited AI push

Apple’s Worldwide Developers Conference is expected to focus on artificial intelligence, including upgrades to Siri and new AI-powered features across its products. For shareholders, this week’s announcements could be an important test of whether Apple can catch up with its rivals.

🛢️ Oil slips despite Iran uncertainty

Oil prices fell Tuesday, giving back part of Monday’s surge even as Iran talks remain stuck and the Strait of Hormuz remains a major source of uncertainty. Brent crude dropped to about $92.92 a barrel, while U.S. West Texas Intermediate fell to around $89.57, after Iran and Israel announced a pause in hostilities following Trump’s appeal for restraint.

⛽ Department of Transport confirms airline fuel cost surge

The U.S. Department of Transportation says airline fuel costs jumped 78% in April as higher oil prices filtered through the industry. Airlines spent an estimated $6.5 billion on fuel during the month, helping explain why airfares rose 20.7% year over year in April’s CPI report. Globally, the industry is expected to face roughly $100 billion in additional fuel costs in 2026.

🥇 Gold, silver turn negative for the year

Gold and silver have now both turned negative for the year after posting massive gains just a few months ago. In January, silver was up 64% while gold gained 25%. Gold is now trading around $4,330 a troy ounce, while silver has fallen below $69, both well below their January highs.

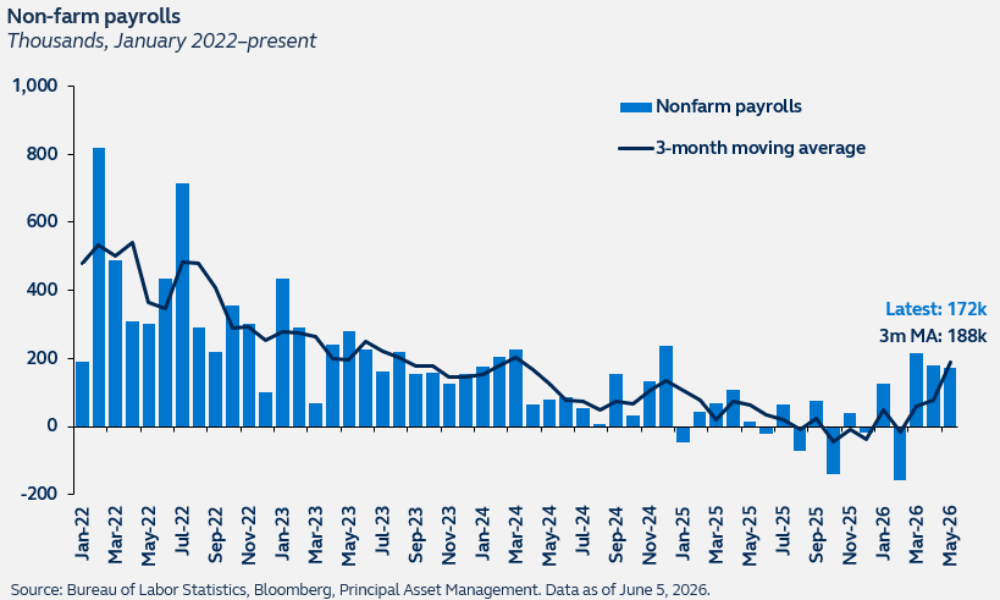

U.S. nonfarm payrolls had a secret ingredient: soccer

Friday’s nonfarm payrolls report looked like a huge win for the U.S. economy.

Employers added 172,000 jobs in May, roughly double what economists expected, sending investors scrambling to price in more aggressive rate hikes.

But a closer look suggests they may have confused a sporting event with an economic boom.

A bartender economy

The biggest story in the report wasn’t technology, manufacturing, or construction, but leisure and hospitality. The sector added 70,000 jobs in May, about five times more than usual, according to BLS data.

Food and beverage services alone accounted for 48,000 new hires.

The timing isn’t a coincidence. The U.S., Canada, and Mexico are all ramping up preparations for the World Cup, creating a wave of hiring across restaurants, bars, hotels, and entertainment venues.

Those jobs count the same as any others, but they’re temporary, lower-paying, and tied to a one-off event rather than a broad economic acceleration.

The wage data pointed in the same direction, with average hourly earnings cooling to 3.4% from 3.6%.

Don’t trust the first print

There’s another reason to be cautious. Nonfarm payrolls have developed a habit of looking much stronger in real time than they do months later, after revisions.

Last year, for example, initial estimates showed 584,000 jobs created before revisions reduced that figure to just 181,000.

That’s why Minneapolis Fed President Neel Kashkari recently argued it’s still too early to talk about rate hikes despite energy prices pushing inflation higher.

“We need to keep watching the data and watching how the conflict in the Middle East unfolds before I want to make any adjustments,” he said.

📌 Bottom line: Rate hikes are still very much on the table, but May’s payroll report has little to do with it because nearly half of the surprise came from one seasonal, event-driven sector.

The best small caps aren’t public anymore

One of the main goals of small private companies used to be going public and attracting more capital. They would become small-cap public companies and eventually rise into mid- and large-cap names.

That was the progression that defined markets for decades, but it’s no longer the case.

Private markets took the winners

Venture capital and private equity now provide hundreds of billions of dollars every year, giving fast-growing companies little reason to list on public markets.

Instead of raising money from retail investors, they stay private while building scale. In 2025 alone, VC funding poured between $425 billion and $512 billion into startups and other private companies, according to Crunchbase data.

SpaceX is a good example. Although Elon Musk’s rocket company is expected to land a $75 billion IPO, it will have existed for more than two decades before going public.

In fact, its IPO would come roughly 17 years after it started generating meaningful revenue.

So while the average investor is finally getting access, they do so only after much of the company’s explosive growth has already happened behind closed doors.

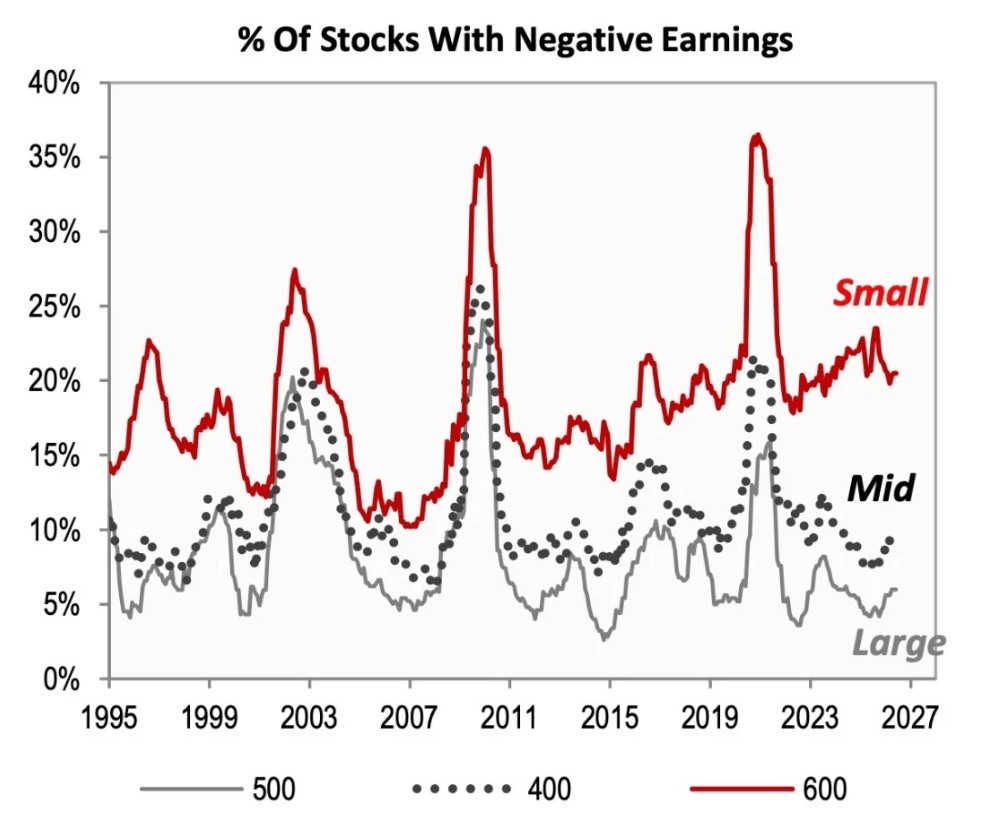

The Russell 2000 has a profitability problem

The result is that the Russell 2000 has become less of a gateway into future large caps and more of a home for companies that may not have been able to secure funding from VCs.

And that helps explain why this corner of the market has a profitability problem.

About 20% of Russell 2000 companies are currently losing money. That’s roughly twice the share among mid-caps and more than three times the share among large-cap stocks.

Small companies have always been riskier. They’re younger, borrow more, and have less predictable earnings.

That profitability gap may help explain why the Russell 2000 has lagged the S&P 500 for years. The index is up this year but has returned just 22% over the past five years, suggesting investors have become much less willing to pay for companies that still aren’t making money.

📌 Bottom line: Buying the Russell 2000 is no longer the same as buying America’s next generation of growth companies. Increasingly, the biggest winners stay private during their most explosive growth years.