🛢️ Oil is back to pre-war levels

Morning Observers,

It’s official! Oil is back to pre-war levels.

Although there are still a lot of unknowns about what the final Iran deal will look like, Hormuz is open (at least to the extent vessel operators trust Tehran will make good on the MoU) and that shows.

According to Kpler data, oil shipments through the Strait reached 4.8 million barrels per day, the highest flow since the beginning of the Iran war.

Highest during the war, yes, but still nowhere near the 20 million barrels a day that moved through Hormuz before the war.

The consensus from commodity analysts in my inbox is that it will take around two months for oil flows through the Strait to normalize, assuming Washington and Tehran play nice.

The lag to bring exports back to par is dual-sided: logistical and production.

Bank of America says mine clearance could take months. Then shipowners could still err on the cautious side while Washington and Tehran duke it out during the negotiation window.

Upstream in the supply chain, BNP Paribas commodity analysts flagged about 12 million barrels a day of shut-in production. By their estimates, bringing that back could take a few months, and that’s in a “best case” scenario.

The good news is that global oil flows have already started filling part of the vacuum created by Hormuz.

- Saudi Arabia has ramped up exports through its pipelines, while the UAE is leaning on routes that bypass Hormuz

- And the U.S., Brazil, Kazakhstan and Venezuela have ramped up exports

But a lot of the "cushion" also came because nations dipped into their emergency reserves, drawing down an average of 3.8 million barrels a day since the start of the conflict.

And finally, although no major economies have fallen into recession yet, demand destruction is happening.

According to IEA estimates, global oil demand is expected to drop by almost 5 million barrels a day in Q2 compared to its pre-war baseline.

So what the market is pricing for now is that alternative export sources, emergency reserves, and demand destruction will be enough to pick up the slack while Hormuz grinds back to normal.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🪙 Gold plunges below $4,000 an ounce

Gold fell below $4,000 a troy ounce for the first time since November as investors continued to adjust to expectations for a higher-for-longer interest rate environment. Spot prices dropped 3% to as low as $3,964, while silver sank more than 5% to below $60 an ounce. Higher interest rates tend to reduce the appeal of precious metals because they don’t generate income, making yield-bearing assets more attractive.

🛢️ U.S. crude slips below $70 a barrel

Oil prices continued to fall after the U.S. and Iran separately confirmed that the Strait of Hormuz has reopened to commercial traffic. West Texas Intermediate crude fell nearly 5% to $69.73 a barrel, its first move below $70 since March 1, while Brent crude dropped to $73.46. Meanwhile, EIA data showed U.S. crude inventories declined by 6.1 million barrels last week, a smaller draw than the previous week’s 8.3 million-barrel decline.

📈 Stocks stabilize after tech-led selloff

U.S. stocks stabilized on Wednesday after a decline earlier in the week driven by weakness in the semiconductor sector. The Dow Jones Industrial Average rose nearly 500 points before trimming some of its gains, while the S&P 500 and Nasdaq surrendered earlier advances as continued pressure on technology and energy stocks weighed on the broader market.

🏦 Bank of America now forecasts three rate hikes this year

Bank of America has dramatically shifted its outlook, going from expecting no interest rate hikes this year to predicting three 25-basis-point increases in September, October, and December. If that happens, the federal funds rate would rise to 4.5%. The new forecast shows just how quickly expectations have shifted following Kevin Warsh’s first meeting as Fed chair.

🤖 OpenAI and Broadcom unveil new chip

OpenAI introduced its first custom artificial intelligence chip, developed alongside Broadcom, as the company looks to reduce its reliance on traditional AI processors. OpenAI says the chip delivers roughly 50% lower operating costs than conventional graphics processing units and will be used across Microsoft-backed data centers. Broadcom stock rose about 2% following the announcement, reflecting optimism around growing demand for custom AI hardware.

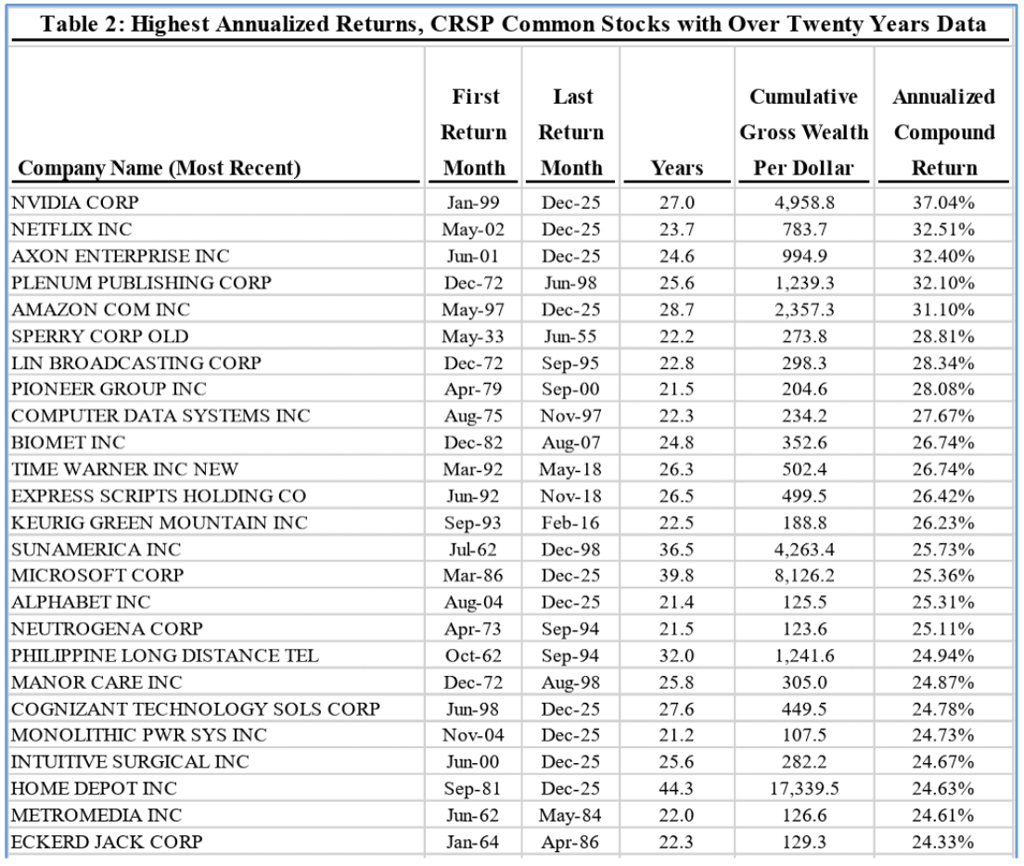

A finance professor proves most stocks can’t even beat T-Bills

Buying stocks has been one of the best ways to build wealth over the past century. Buying the average stock hasn’t.

Most publicly traded companies haven’t even outperformed one-month Treasury bills over their lifetimes, which is a remarkable outcome given that Treasurys are considered virtually risk-free.

Even going back 100 years, the stock market’s spectacular returns were built by only a tiny handful of extraordinary companies.

The stock market’s slim minority

A new study from Arizona State University finance professor Hendrik Bessembinder tracked nearly 29,000 U.S. stocks from 1926 to 2025. The results overturn the idea that buying individual stocks is a winning game:

- 59% of stocks failed to beat one-month Treasury bills over their lifetimes

- 37% outperformed Treasury bills, but collectively only offset the wealth destroyed by the other 59%

- Just 1,082 companies, or 3.7%, generated all of the market’s net shareholder wealth… and only 46 companies, or 0.16%, were responsible for half of it

The study is a great example of diversification and a case for owning the market instead of trying to pick its winners.

The S&P 500’s biggest criticism is also its biggest strength

The stock market’s concentration problem is hardly news.

Today, the S&P 500 Index’s ten largest companies generate 34% of its total profits, according to Apollo, and account for an outsized share of its returns.

Through the lens of Bessembinder’s research, however, that concentration looks less like a flaw.

Because the S&P 500 is weighted by market value, it automatically allocates more capital to companies that create the most value and less to those that don’t.

Investors don’t have to predict the next Apple or Nvidia decades in advance. They simply own the market, and the winners earn larger weights as they grow.

“The S&P 500 is not a diversified index anymore,” wrote Apollo chief economist Torsten Slok. “It is dominated by a small number of extraordinarily profitable tech companies.”

📌 Bottom line: The biggest challenge in investing is finding the handful of companies that will generate decades of extraordinary returns. History suggests that’s almost impossible, which helps explain why broad market index funds consistently outperform most stock pickers over time.

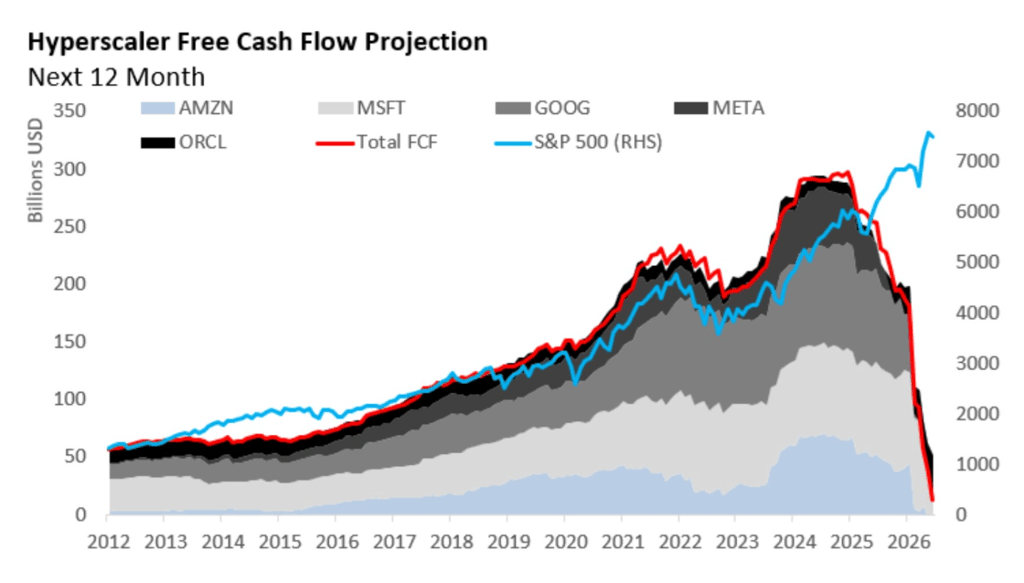

Big Tech has a free cash flow problem

For years, investors could ignore almost any concern about Big Tech because one number kept getting bigger: free cash flow.

It funded buybacks and acquisitions and helped justify the soaring valuations that made AI hyperscalers the market’s biggest winners. Now that number is in reverse.

The free cash flow squeeze

In a new analysis, Nomura estimates free cash flow across Amazon, Microsoft, Alphabet, Meta, and Oracle will fall over the next 12 months due to AI spending.

After climbing from roughly $50 billion in 2012 to nearly $300 billion today, aggregate free cash flow is projected to fall back to levels not seen in more than a decade.

Free cash flow is the cash left after a company pays its bills and invests in the business. That’s effectively the money that funds buybacks, dividends, acquisitions, and future growth.

In other words, AI spending is shrinking the pool of cash that can be returned to shareholders.

Wall Street is already adjusting

After leading the market for much of the year, hyperscalers have begun to stumble. The Mag 7, along with Oracle and Broadcom, have lost roughly $2.7 trillion in market value this month alone.

And every new dollar spent on AI raises the hurdle. The more hyperscalers invest today, the more revenue those investments must eventually generate to justify today’s valuations.

The squeeze may not end there. Goldman Sachs strategist Ryan Hammond expects AI spending to keep climbing and argues Wall Street is still underestimating how much hyperscalers will spend through 2027.

If he’s right, the pressure on free cash flow could persist for years.

📌 Bottom line: For the first time in years, hyperscalers are asking investors to accept less cash today in exchange for more cash tomorrow. That may force Wall Street to stop treating Big Tech like a cash machine and more like a capital-intensive industry.