📈 MEGA rotation is happening right now

Morning Observers,

Stocks are at record highs and AI is still all over the headlines, but there’s a mega rotation happening under the hood, which says this is more than just another AI rally.

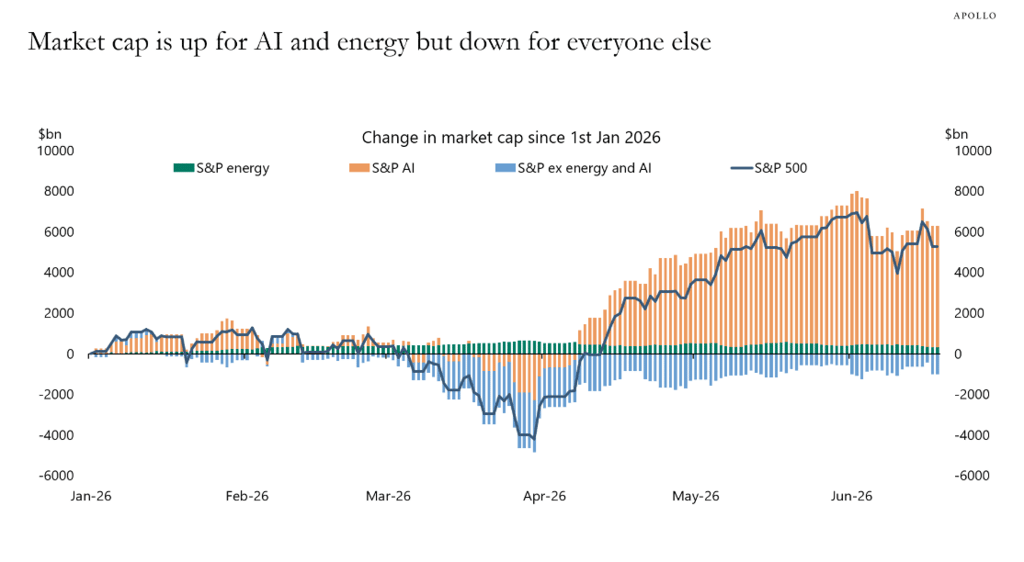

This morning, I came across an Apollo chart with market-cap growth in the S&P 500 since the start of 2026, broken down by AI and everything else (see first story).

And surprise, surprise, AI blows everyone out of the water.

Since the beginning of the year, AI stocks have added more than $6 trillion in market value, while the rest of the index has barely budged or lost value.

That looks like the classic AI concentration story pundits have been banging the drum on for years. But if you look beyond the cap-weighted S&P 500, the market is rotating into a whole different trade.

Here’s a quick rundown of the rotation:

- Small caps are outperforming large caps for the first time in years

- Value stocks are outperforming growth

- International stocks, especially emerging markets and the Asian AI supply chain, are outperforming the U.S.

- Cyclicals are beginning to outperform the S&P 500 this month

- And the Magnificent 7 are no longer looking so magnificent. The group is underperforming the broader market and are down for the year

There are a few reasons behind this mega rotation.

One is that investors are no longer banking only on a handful of headline AI stocks. They are diversifying down the supply chain and geographically. This is why Korean and Taiwanese stocks have been so hot this year.

Meanwhile, Europe and other international markets are closing the valuation gap and getting an extra boost in dollar terms because of the weaker dollar.

Second, and perhaps most important, the market is betting on the so-called “reflation trade,” which means inflation picks up, but not to the point where it chokes off the economy.

The biggest giveaway is the rise of cyclicals this month.

Cyclicals are among the biggest beneficiaries of reflation because they have the most operating leverage. When nominal revenue rises, their earnings can rise even faster because a big chunk of their cost base is already fixed.

With all that said, AI remains the single biggest failure point even if investors are diversifying away from the hottest AI names.

Unlike the dot-com bubble, this emerging technology is no longer confined to the market. The real economy is increasingly leaning on AI investment, from chips and data centers to power equipment, grid upgrades, and corporate capex.

If there is any unwinding in AI capex spending or even talk of capital discipline, the AI/reflation trade could fall apart like a house of cards.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🪙 Gold loses its shine

Gold is coming off its third straight weekly loss after the Fed’s latest statement pushed investors deeper into higher-for-longer mode. The metal finished last week below $4,200 an ounce, with rising real yields and a stronger dollar doing most of the damage. As market analyst Nikos Tzabouras put it, “Higher-for-longer Fed expectations are toxic for non-yielding assets” like gold.

💵 Dollar bulls are back

The Fed’s hawkish outlook sent the U.S. dollar to its strongest level of the year, with the Dollar Index closing above 101 for the first time in 2026. The greenback gained against the euro, pound, yen, and Canadian dollar as traders increasingly bet the Fed’s next move will be a hike. According to LSEG data, futures markets are now fully pricing in a hike by October.

🇯🇵 Yen flirts with a 40-year low

The yen stayed under pressure after the dollar climbed to 161.8 yen, its highest level since 1986. The widening gap between U.S. and Japanese rates continues to hammer the currency, even after the Bank of Japan lifted rates to their highest level in 31 years. That has revived speculation that Japanese authorities could step in if the yen’s slide gets uglier.

🚀 U.S. stocks get flooded with cash

Investors poured a record $119.2 billion into U.S. equity funds in the week ending June 17, according to new Bank of America data. Tech enthusiasm is still doing the heavy lifting, with U.S. stock funds now on pace to attract a record $739 billion this year. So much for inflation anxiety and geopolitical nerves.

🍎 Intel gets the Apple bump

Intel jumped more than 14% last week after Trump announced that the chipmaker will work with Apple to design and manufacture semiconductors in the U.S. The deal strengthens Intel’s role in domestic chip production and comes after the U.S. government took an equity stake in the company. Translation: investors are betting Intel may finally matter again in America’s chip race.

Your “diversified” index fund is making one giant bet

Passive investing has never been more popular. And yet, ironically, passive investors have rarely been this concentrated.

The S&P 500 Index has climbed to multiple record highs this year, but all of its gains have come from a tiny sliver of the market.

According to an analysis from Apollo chief economist Torsten Slok, the S&P 500’s entire 2026 gain has been driven by just two sectors: AI and energy. Everything else is underwater.

The concentration gets even more extreme beneath the surface.

Nineteen of the 20 S&P 500 stocks that have doubled this year are AI-related, according to investment strategist Charlie Bilello. Semiconductor companies now account for roughly 19% of the entire index, twice their weighting at the peak of the dot-com era.

That’s the paradox of passive investing: every new dollar automatically buys more of the market’s biggest winners, reinforcing the very concentration investors think they’re avoiding.

When diversification becomes an illusion

None of this means the AI trade is about to unwind.

Markets have a tendency to become concentrated, and narrow leadership can last for years. Besides, this concentration mostly holds within the S&P 500.

Beyond the index, investors are rotating into different factors, including value, sectors that are less tied to AI, and geographic regions that are not priced to perfection like the U.S.

That said, buying the S&P 500 once meant owning America’s economy. Today, it increasingly means owning a handful of mega-cap AI companies and hoping they keep outperforming everyone else.

📌 Bottom line: The S&P 500 still looks diversified on paper, but its returns are increasingly driven by a handful of companies and themes.

Gold’s tug of war: Interest rates vs. central bank buying

Gold went from the world’s hottest trade to a losing investment in just a few months. After peaking above $5,600 in January, it’s now down for the year.

Yet the world’s biggest buyers, central banks, haven’t backed away.

Central banks aren’t done

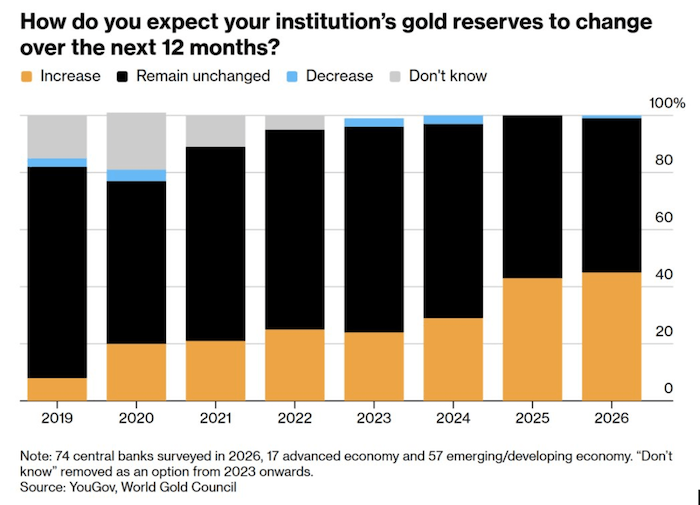

After a brief net sale in April, largely driven by Turkey raising cash to support the lira, global central banks returned as buyers in May, adding a net 20 tonnes of gold.

The longer-term trend is even more striking. World Gold Council surveys show that 45% of central banks expect to increase their own gold holdings over the next 12 months, four times the share seen seven years ago.

Another 89% believe global central bank gold reserves will continue growing. That's a structural shift because gold is increasingly being treated as a reserve asset rather than merely a macro hedge.

Bond markets have entered the chat

However, the bullish case isn’t uncontested.

Bloomberg commodity strategist Mike McGlone argues gold’s rally may have already peaked, noting that prices have become more detached from their long-term trend than at almost any point in the past four decades.

The other major challenge is higher interest rates.

Gold pays no income, so every increase in bond yields raises the opportunity cost of holding it. That’s becoming a bigger hurdle as U.S. 10-year yields climb to their highest level since early 2025.

📌 Bottom line: Gold is caught in a tug of war between two powerful forces. Central banks continue to provide steady structural demand, but higher interest rates make the metal less attractive to private investors.