Meet the new “central bank of oil”

Morning Observers,

For decades, China exported deflation to the West by flooding the world with cheap manufactured goods.

Now, it may be stabilizing the global oil market by buying less oil at exactly the moment everyone else is scrambling for more.

A wave of commentary recently focused on China’s crude imports plunging to levels not seen since 2016. At first glance, that looks like another warning sign for China’s slowing economy. But there’s another explanation.

China spent years building a 1-billion-barrel strategic petroleum reserve while oil markets were relatively calm. So now, as geopolitical tensions threaten global supply chains, Beijing can afford to step back from crude markets while the rest of Asia competes for supply.

That’s a major reason why oil prices haven’t exploded past $120 a barrel.

Thanks to its massive stockpiles, China may have quietly become what Council on Foreign Relations senior fellow Brad Setser called “the new central bank of oil, replacing Saudi Arabia.”

And according to Setser, that may have “helped save the U.S. and Europe from a much bigger oil shock.”

For months, analysts have warned that disruptions tied to the Strait of Hormuz were being temporarily offset by strategic reserve releases and rising U.S. exports. But many believe the buffer won’t last much longer if the Iran war continues.

Ninepoint Partners analyst Eric Nuttall recently called this the “great oil repricing,” warning that energy markets may still be underestimating how quickly crude prices could move higher if the war isn’t resolved soon.

For now, however, China’s stockpiles may be buying the global economy something incredibly valuable: time.

Time for supply chains to adjust. Time for diplomacy to work. Time for Washington and Tehran to avoid a larger energy shock.

But even the world’s new “central bank of oil” doesn’t have unlimited reserves… and the clock is ticking on diplomacy.

Let’s dive in.

— Sam Bourgi, Interim Editor

Five things to know before opening bell

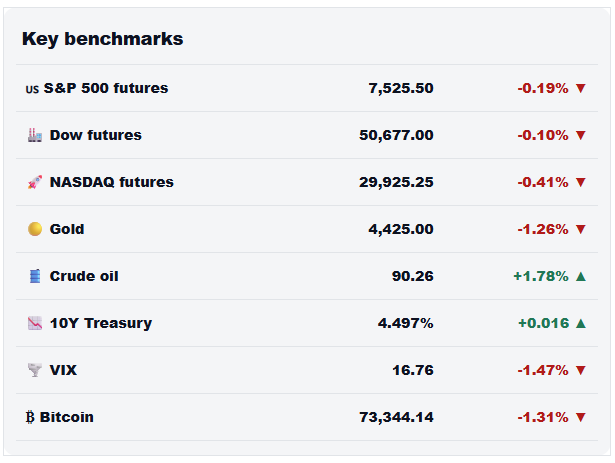

📊 Markets swing as Iran ceasefire rumors whipsaw investors

U.S. stocks traded unevenly on Wednesday after conflicting reports emerged about a possible ceasefire agreement with Iran. Iranian state media claimed that a draft deal had been proposed to reopen maritime traffic through the Strait of Hormuz, but the White House later denied the reports, highlighting how sensitive markets remain to geopolitical headlines. The uncertainty kept investors cautious, with the S&P 500 pulling back slightly from record highs.

🛢️ Oil prices tumble on hopes of Hormuz reopening

Crude prices dropped sharply as traders reacted positively to speculation surrounding a potential U.S.-Iran truce. West Texas Intermediate fell more than 4%, slipping below $90 a barrel, while Brent crude declined over 3% to roughly $96.25. Energy markets remain closely focused on the Strait of Hormuz, which carried nearly 20% of global oil exports before the conflict began.

📈 Goldman Sachs boosts S&P 500 forecast again

Goldman Sachs raised its year-end target for the S&P 500 to 8,000, implying roughly 6% upside from current levels. The bank said stronger-than-expected corporate earnings continue to drive the market higher, with analysts now forecasting earnings per share of $340 in 2026 and $385 in 2027. According to Goldman, profit growth has been the primary force behind the index’s rally this year.

🤖 AI-fueled semiconductor boom reshapes the market

Semiconductor and chip-equipment companies now make up a record 18% of the S&P 500’s total market capitalization, according to new Bloomberg data. That share has more than tripled since the 2022 bear market, underscoring how aggressively investors continue to pile into AI-related stocks. The sector’s rapid growth is increasingly reshaping the broader market and driving a significant portion of index performance.

✈️ Boeing takes another step toward a turnaround

Boeing cleared a major regulatory hurdle after completing a capstone review with the Federal Aviation Administration, allowing the company to move closer to increasing monthly 737 Max production. The production ramp-up is viewed as a key piece of Boeing’s effort to improve profitability and cash flow after several difficult years. The company recently reported full-year 2025 revenue of $89.46 billion and returned to annual profitability following a steep loss in 2024.

Commercial real estate’s “not 2008” moment

Everyone keeps saying this isn’t 2008.

That may be true… but parts of the commercial real estate market are behaving as if investors have forgotten what caused the 2008 financial crisis in the first place.

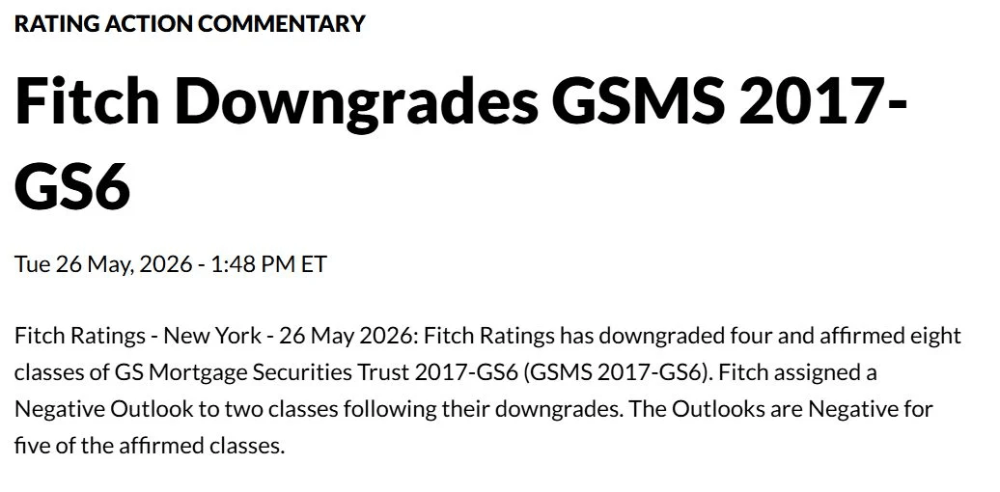

Fitch Ratings just downgraded several bonds tied to a Goldman Sachs commercial mortgage deal, adding to growing signs that problems are spreading through commercial real estate credit markets.

The slow-motion unwind in commercial real estate

The downgrade involved GS Mortgage Securities Trust 2017-GS6, a commercial mortgage-backed security (CMBS) backed by loans tied to hotels, condos, office buildings, and multifamily properties.

Several lower-rated bond classes were pushed deeper into distressed territory, while Fitch assigned Negative Outlooks to multiple other tranches, signaling that conditions may worsen further.

The key issue is that the stress is no longer contained in the weakest parts of the market.

Even some higher-rated bonds are now carrying negative outlooks despite still holding investment-grade ratings. One loan portfolio inside the deal is already showing roughly 14% defaults.

At the same time, commercial real estate conditions are weakening across the board.

Office vacancies remain elevated. Hotel demand is weakening. Multifamily landlords are losing pricing power. And many properties financed during the zero-rate era now face refinancing at dramatically higher borrowing costs.

Commercial mortgage-backed securities delinquency rates have now climbed above 7.5%, according to Trepp data. Office delinquencies remain the highest at nearly 11.7%.

The shadow banking problem nobody wants to talk about

A growing share of commercial real estate lending now sits inside private credit funds, securitized products, and non-bank lenders that expanded aggressively during the low-rate boom.

That structure works well when money is cheap and property values keep rising. It becomes far more fragile when refinancing dries up.

The real risk is not whether a few risky bonds fail. It’s whether lenders begin pulling back across the system at the same time.

That’s what made 2008 so dangerous. Once investors lost confidence in commercial real estate loans, CMBS issuance collapsed from roughly $229 billion in 2007 to just $3 billion by 2009, according to data from the University of Pennsylvania’s Wharton School.

📌 Bottom line: While this isn’t a 2008-style panic, higher rates are making commercial real estate loans harder to refinance, forcing lenders to pull back and putting pressure on property values, construction, hiring, and regional banks over time.

AI may be keeping rates higher for everyone else

If the market is right, the Federal Reserve’s next move will be a rate hike, not a rate cut.

In many ways, bond markets are already doing the job. Treasury yields have surged, mortgage rates remain elevated, and borrowing costs across the economy are climbing again.

Normally, that would be enough to slow growth.

Instead, Corporate America is still spending aggressively on AI infrastructure and data centers… giving the Fed more room to keep fighting inflation while households absorb the damage.

The Fed may be fighting AI FOMO

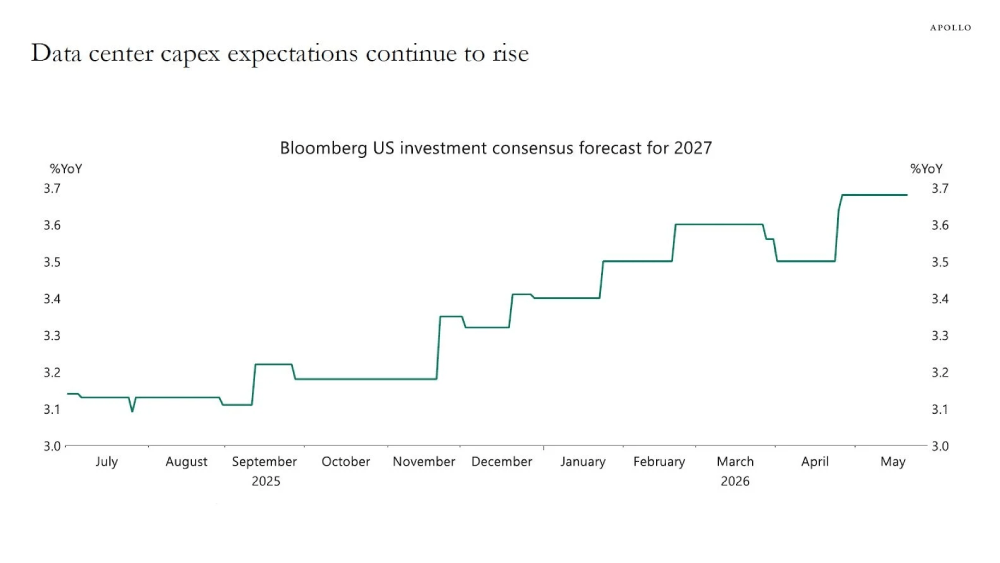

In a recent note, Apollo chief economist Torsten Slok argued that the Fed’s real battle is no longer just inflation. It’s AI spending.

Despite higher borrowing costs, companies continue pouring hundreds of billions into AI infrastructure and data centers.

“In fact, despite the move higher in rates in recent months, the consensus forecast for capex in 2027 continues to rise,” Slok wrote, referring to the anticipated 3.7% year-over-year growth in data center expenditures over the next 12 months.

The Magnificent Seven alone — companies like Amazon, Microsoft, Alphabet, and Meta — are expected to spend roughly $650 billion on AI infrastructure this year.

So, while higher rates are supposed to slow corporate investment, the AI spending boom may be overpowering the normal economic cycle.

“The bottom line is that rates can continue to move higher because rate hikes are not slowing the economy and inflation the way the textbook would predict,” Slok said.

Consumers are the collateral damage

While Big Tech keeps spending, households are absorbing the consequences of higher rates.

Freddie Mac’s average 30-year fixed mortgage rate was 6.51% last week. Auto loan delinquencies are also climbing sharply, with nearly 7% of subprime borrowers now at least 60 days behind on payments.

In other words, AI investment may be keeping the economy strong enough for the Fed to justify higher rates, even as consumers fall further behind on mortgages, car payments, and other debt.

📌 Bottom line: AI investment may be unintentionally giving the Fed cover to keep interest rates higher for longer. Corporate America can still spend aggressively on data centers and infrastructure, but households are the ones absorbing the fallout through higher borrowing costs and rising debt stress.