Korea is becoming AI stress test

Morning Observers,

Korea is becoming an experiment (and potentially a stress test) of what happens when your entire economy hangs on the AI trade.

Its benchmark KOSPI index has risen 75% this year, and most of the gains have come from just two memory-chip giants: Samsung Electronics and SK hynix.

Together they now represent more than half of the country’s stock market. (Talk about market concentration.)

This is not merely a stock market story. Korea makes most of its money from exports, and chips now account for more than 42% of all its exports.

What that really means is that AI spending is driving not just Korea's stock market but also much of its economy, from business investment and tax revenue to consumer confidence and, increasingly, household wealth.

Korean President Lee Jae Myung is now seemingly attempting to talk the market down. At a policy meeting this morning, he called his own market “unstable.”

Lee effectively admitted that the stock market has gotten to a point where it can no longer absorb even ordinary changes in sentiment without violent consequences.

Korea may be an extreme example, but the parallels with the U.S. are hard to ignore.

AI capex spending is now a bigger U.S. GDP growth driver than consumer spending, and it contributed 39% of economic growth last year through Q3, more than dot-com spending at its peak.

Fed Governor Lisa Cook said there are $1.5 trillion worth of data-center projects in the pipeline, most of which haven’t even started yet. This backlog is driving construction, manufacturing orders, utility investment, regional employment, and state and local tax expectations.

Most bear markets come about because recessions destroy earnings. But the next downturn could work in reverse.

When AI spending drives economic growth while AI stocks inflate perceived wealth, a sudden loss of confidence on Wall Street can quickly ripple through the economy.

The irony is that you can see all the signs you want, but nobody knows where we are exactly in the cycle.

And if there’s one thing we learned from the dot-com bubble, it’s that staying on the sidelines too early can destroy even more wealth than the bubble itself.

- Dan Runkevicius, Editor

|

|

💻 Software stocks plunge following IBM’s “devastating blow”

Software stocks sold off after IBM released preliminary earnings that fell short of Wall Street’s expectations. IBM shares dropped as much as 26%, prompting Vital Knowledge founder Adam Crisafulli to call the earnings report a “devastating blow” for the software sector. The selling spread across the industry, with the iShares Expanded Tech-Software Sector ETF falling nearly 3%.

📉 Inflation drops the most since 2020

U.S. consumer prices fell 0.4% in June from the previous month, the largest monthly decline since May 2020, as lower energy costs provided much-needed relief. Annual inflation eased to 3.5%, while core inflation slowed to 2.6%, with both readings coming in below economists’ expectations. Prediction markets quickly scaled back bets on a July Fed rate hike, with odds falling from more than 35% to about 8%.

💰 Goldman cashes in on active markets

Goldman Sachs reported a record $7.42 billion in trading revenue for the second quarter as rising stock markets and geopolitical uncertainty kept clients active. Stock-trading revenue jumped 72% from a year earlier, while investment banking fees reached their highest level since 2021. The strong results point to improving conditions for large investment banks after several sluggish years for dealmaking.

🛢️ The old Hormuz order is over

President Trump’s decision to reimpose a U.S. blockade on Iranian shipping through the Strait of Hormuz sent crude prices up more than 10% at the start of the week, marking the biggest one-day gain since May 2020, according to The Wall Street Journal. After weeks of falling prices, investors are once again focused on supply risks; Rachel Ziemba of the Center for a New American Security says the chances of a return to the previous status quo in Hormuz are “effectively zero.”

🧠 ASML raises forecast as AI chip demand surges

ASML raised its annual sales forecast for the second time this year as booming AI investment drives demand for its chipmaking equipment. The company now expects 2026 revenue of €43 billion to €45 billion, well above its previous guidance of €36 billion to €40 billion. CEO Christophe Fouquet also announced plans to expand production of its advanced EUV machines to meet a growing backlog of orders extending into 2028.

The biggest investing mistake? Calling the top too early

History suggests that the biggest investing mistake isn’t buying into a bubble. Far more wealth has been destroyed by the belief that you can accurately predict when it will end.

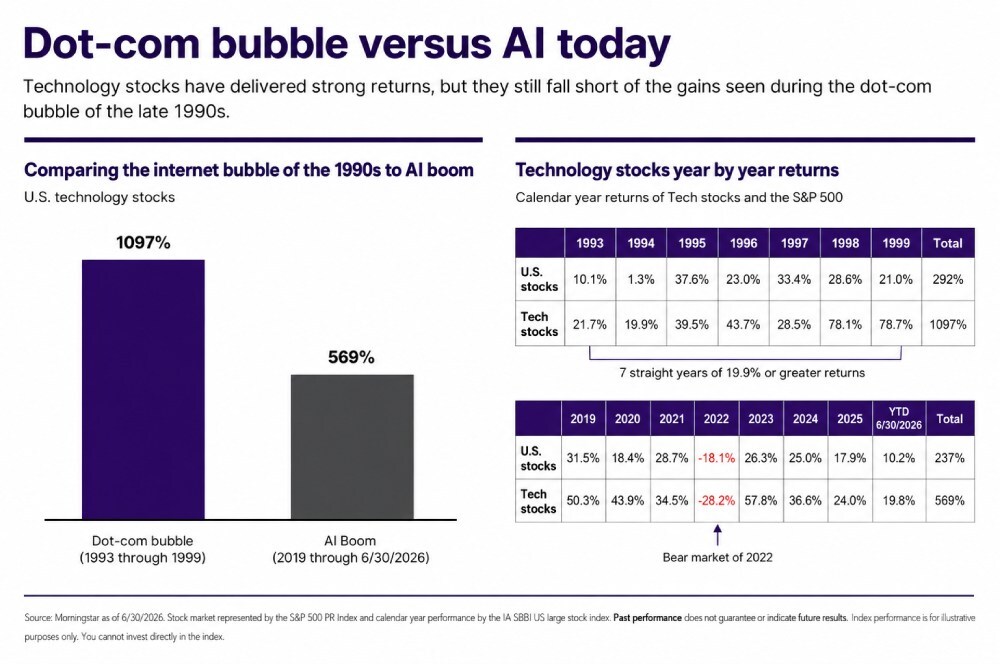

Every technology bubble is also an adoption story

The last time investors encountered a truly transformative technology, the internet, valuations looked absurd years before the rally finally peaked.

And investors who sold because stocks looked “too expensive” missed the strongest gains of the entire cycle.

According to BlackRock, U.S. technology stocks returned 1,097% between 1993 and 1999, with most of those gains occurring while valuations were far above historical averages.

Since the AI boom began in 2019, tech stocks have returned roughly 569%, or about half the gains recorded during the dot-com era.

That doesn’t mean AI stocks will repeat the dot-com playbook exactly. Today’s AI leaders are far larger and more profitable than the internet companies of the 1990s.

What it does challenge is the assumption that expensive valuations automatically mean the rally is over.

The infrastructure story is still getting started

History isn’t the only reason to think the AI boom has further to run. Current demand points in the same direction.

Goldman Sachs believes hyperscaler AI investment could reach $1.4 trillion by 2027 in its most optimistic scenario. The bank’s thesis rests on the assumption that demand for AI computing is still in its infancy.

One way to measure that demand is through token consumption, a number of units of text, images, or data processed by AI models. Every AI prompt consumes tokens, making token growth one of the clearest measures of real-world AI adoption.

Goldman expects AI usage to increase roughly 24-fold by 2030 as more businesses roll out AI tools across their everyday operations. If it is right, the market still has plenty of room to run.

📌 Bottom line: As long as AI demand and infrastructure spending continue to accelerate, expensive valuations alone aren’t a reliable signal that the rally is over.

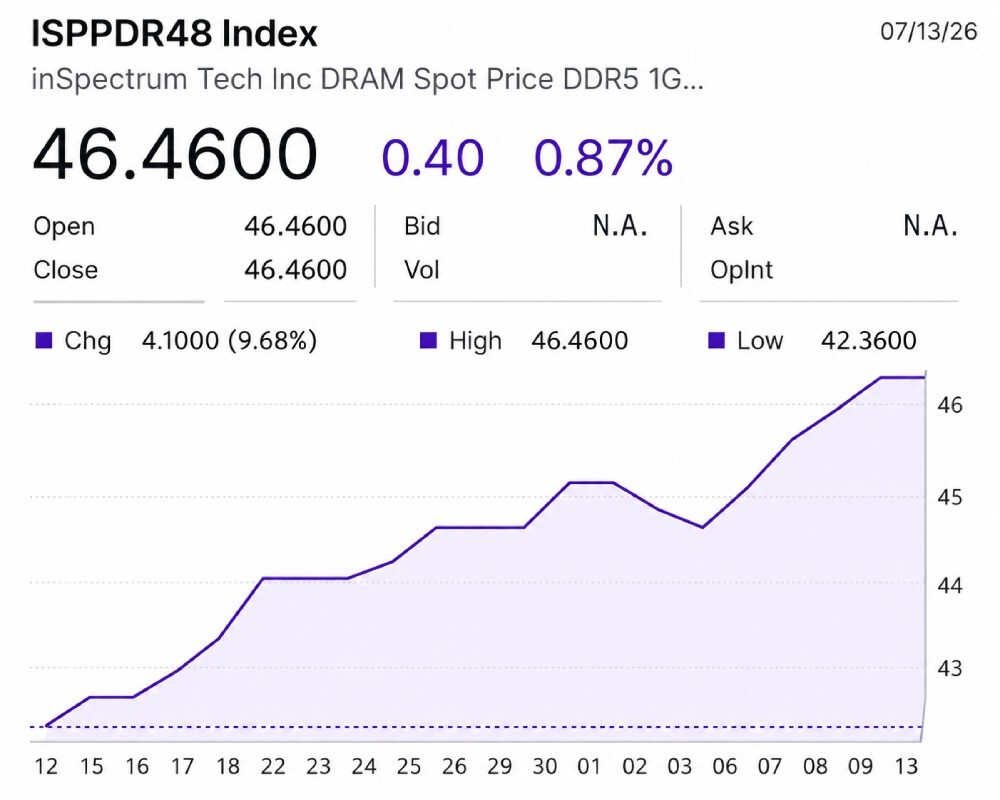

Why DRAM pricing matters more than SK Hynix’s earnings

SK Hynix lost billions in market value this week after analysts warned quarterly profits could miss expectations, dragging AI-related semiconductor stocks lower.

The company’s American depository shares (ADRs) plunged 9.3% in a single day, after the stock fell a record 15% in South Korea.

But while investors are panic-selling SK Hynix, the price of the memory chips that drive much of SK Hynix’s business kept climbing.

DRAM spot prices

The inSpectrum DDR5 DRAM spot price index tracks the daily market price of DDR5 memory chips, which go into data centers alongside AI chips. The index climbed nearly 10% over the past month.

The gains have been gradual rather than explosive, suggesting sustained demand instead of a temporary shortage.

Every AI server needs DRAM. So when memory prices rise, companies like SK Hynix and Micron usually gain more pricing power. So why are memory stocks falling if memory prices are rising?

Looking past the next quarter

The answer comes down to timing.

SK Hynix sold off after Korea Investment & Securities projected quarterly operating profit could miss consensus by roughly 8%. That forecast is based on the next earnings report.

DRAM spot prices are looking further ahead.

Most memory is sold through quarterly or annual contracts, meaning today’s spot prices take time to feed into reported revenue and margins.

A stronger pricing environment today may not show up in company results until future quarters.

The two aren’t necessarily contradictory. Stocks are pricing the next quarter, while DRAM may be pricing the next cycle.

📌 Bottom line: If DRAM spot prices continue rising, contract prices are likely to follow over the coming quarters, boosting margins for memory makers.