Is this all-talk, no hikes Fed?

Morning Observers,

Kevin Warsh is loosening up, reinforcing the thesis that he could be an all-talk, no-hikes Fed chair.

Before he was sworn in, Warsh had built a rep as a serious hawk. He called inflation “a choice,” criticized the Fed’s giant balance sheet, and made clear that price stability should come first.

But many experts who have followed his policy views for years, including Paul Krugman, say that is just the way he is. Warsh often talks like a hard-money hawk, but when it comes time to act, he sides with the politics.

At the European Central Bank’s annual Forum, Warsh is now seemingly hedging his stance on balance sheet reduction, saying effectively that it will be a “long road ahead.”

And here’s the most interesting part.

Warsh doubled down on his commitment to bring inflation back to the 2% target. The only problem is that he didn’t mention which “inflation” exactly he is trying to bring back down.

Core PCE, once the Fed’s main inflation gauge, is still way above the Fed’s target at 3.4%, the highest reading this year, even though it already strips out volatile energy and food prices.

And yet, Warsh was confident saying that “inflation risks have come down.”

So what exactly is he tracking as his inflation benchmark? He has said many times that he prefers trimmed-mean PCE, which is currently much lower at 2.4%.

Trimmed mean is an interesting spin on how you measure inflation. It is supposed to give you a less distorted picture of actual inflation because it strips away the categories that showed the most extreme changes (on both ends) that month.

On the other hand, it can overlook the beginning of a real inflation wave and give policymakers an excuse to keep rates lower for longer.

Either way, Warsh isn’t likely to rely on government data for long.

Yesterday he said he plans to bring in better, “more real-time” economic data within the next year, and he said he would appoint members to five new task forces, including one focused on new data-gathering techniques.

Whether that new methodology shows inflation at 3.4%, 2.4%, or 2%, nobody knows.

Warsh said inflation is “a choice.” So, apparently, is how you measure it.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🏭 U.S. manufacturing grows for sixth straight month

U.S. manufacturing activity expanded for a sixth consecutive month in June, suggesting the sector continues to weather higher prices tied to the Iran war. The Institute for Supply Management’s manufacturing PMI slipped 0.7 points to 53.3 but remained near a four-year high, with any reading above 50 signaling expansion.

🛢️ Oil falls below $69 as U.S.-Iran talks progress

Oil prices fell on Wednesday after reports that U.S. and Iranian officials made progress in talks held in Qatar, raising hopes that an interim ceasefire could evolve into a more permanent agreement. U.S. West Texas Intermediate crude dropped about 2% to an intraday low of $68.06 a barrel, while Brent crude fell more than 2% to $71.19.

🌐 AOL owner debuts at an $18 billion valuation

Italian software company Bending Spoons, which owns old internet brands including AOL, Vimeo, and Eventbrite, made its Nasdaq debut on Wednesday after raising $1.68 billion at $29 a share. The IPO valued the company at more than $18 billion. Bloomberg reported that the 10 largest investors received roughly 85% of the shares allocated in the offering.

🏛️ Hassett urges Fed to keep rates unchanged

White House economic adviser Kevin Hassett urged the Federal Reserve not to raise interest rates, arguing that stronger growth is being driven by supply-side improvements rather than overheating demand. Speaking on Fox Business, the National Economic Council director said hiking interest rates would be a “macroeconomic mistake” given what he described as a “supply-driven boom.”

💾 Chip selloff drags on global tech

Technology stocks are down for a second day led by chipmakers. Nasdaq 100 futures slipped 0.4%, while South Korea’s Kospi plunged 7.9%, with Korean chip giants SK Hynix and Samsung losing a combined $290 billion in value.

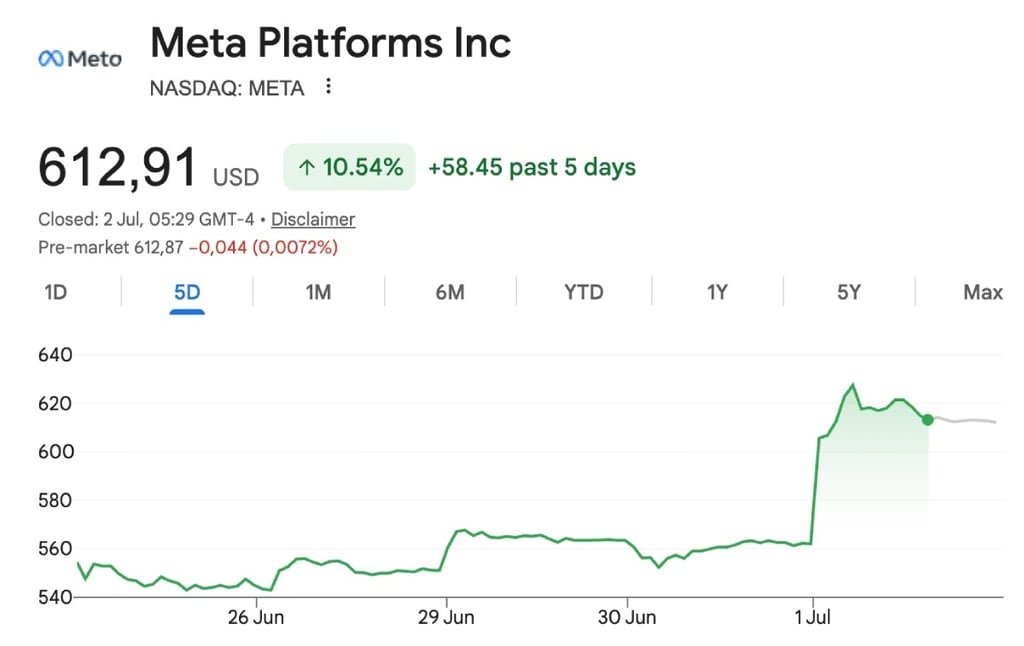

Meta may be borrowing Amazon’s greatest idea

Wall Street treats Meta’s AI spending as little more than a giant expense. But what if it’s actually the construction cost of an entirely new business?

On Wednesday, Meta said it is exploring a cloud infrastructure business that would sell access to its AI models and excess computing capacity. If that strategy sounds familiar, it should.

Amazon’s most profitable business wasn’t the original plan

Before Amazon Web Services became the backbone of the internet, it was simply the infrastructure Amazon built to run its own retail business.

Amazon later realized that infrastructure could become a business in its own right. By renting out its servers to outside developers, it transformed what had been a massive operating expense into one of the most profitable businesses in corporate America.

Meta’s plan isn’t identical, because AI compute is a different business from cloud hosting. But the underlying economics are strikingly similar.

Rather than treating AI infrastructure as a permanent cost of competing with OpenAI and Google, Meta is looking for ways to make that investment pay for itself.

Maybe Wall Street has been looking at Meta the wrong way

The Wednesday announcement sent Meta shares up more than 10%, reversing part of the recent selloff.

The prevailing narrative had been that Meta was spending too much with little visibility into how it would make money from it. That skepticism may be missing the bigger picture.

Morgan Stanley estimates Meta’s AI investments could add between $1 and $3 to earnings per share by fiscal 2028. The bank also projects Meta AI could generate roughly $10 billion in annual revenue if it reaches 1 billion users and monetizes just 10% of them.

Although that is no small feat, Morgan Stanley considers it achievable given Meta’s massive global user base.

📌 Bottom line: Investors have largely viewed Meta’s AI buildout as an expensive race to keep up with rivals. But if Mark Zuckerberg is following Amazon’s playbook, those data centers could become a business in their own right.

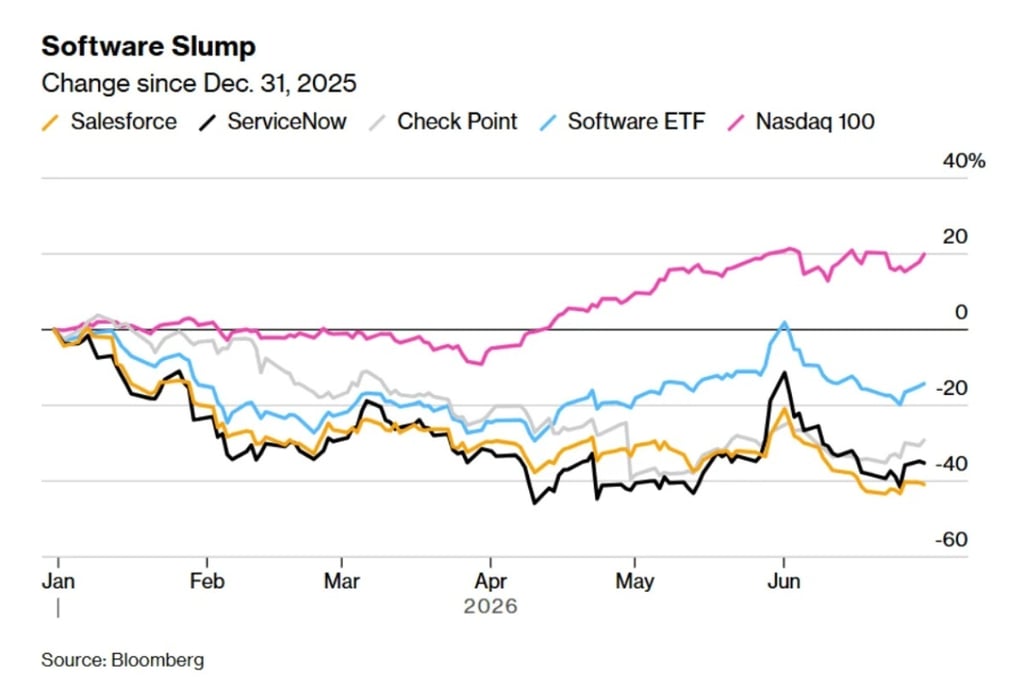

Are software bears hallucinating?

Wall Street has developed a habit of finding new reasons to hate software stocks.

First, AI was supposed to replace them. Now the fear is that AI won’t generate enough revenue to justify the industry’s enormous spending spree.

When the bear case keeps changing, it’s often a sign that the market is approaching a bottom, according to analysts at Guggenheim.

The market is pricing software for extinction

In a recent note, Guggenheim upgraded Salesforce, ServiceNow, and Check Point Software Technologies, arguing that their valuations imply a level of permanent decline that is difficult to justify.

The numbers help explain why. The three stocks were all trading between 47% and 57% below their all-time highs in June. Meanwhile, the iShares Expanded Tech-Software Sector ETF was down roughly 15% this year, even as the Nasdaq gained nearly 19%.

“Valuations imply many software companies will decline into perpetuity because of AI,” Guggenheim analyst John DiFucci wrote. “We don't believe that to be true.”

DiFucci acknowledged that AI will disrupt the industry but argued that the idea it will broadly destroy software companies is “a hallucination.”

“The task now is to identify where disruption is likely to reshape economics and where fears may be running ahead of fundamentals,” said AllianceBernstein analysts.

📌 Bottom line: Markets usually get the direction of technological change right but the timing wrong. For now, software is being indiscriminately deemed dead, which is objectively not the case.