Is tech concentration really a problem?

Morning Observers,

Is tech concentration in your portfolio really something to worry about?

U.S. stocks are currently the most concentrated since 1932-1998 (depending on how you measure it), and that concentration is both at the sector level and among individual stocks.

Tech now makes up a larger share of the S&P 500 than it did at the peak of the dot-com bubble. And within tech itself, just a handful of stocks dominate the sector.

Interestingly, stocks followed an eerily similar pattern in the run-up to the dot-com bust. So, are we doomed?

There’s a recent paper titled "The Fallacy of Concentration" by Mark Kritzman and David Turkington that tackles this very question.

And their findings are almost the exact opposite of the doom and gloom you often hear in the media.

First, concentration alone had virtually no ability to predict what happened next. A sector’s concentration explained only 0% to 0.3% of the variation in its returns, volatility, and drawdowns the following year. That's about as useless as empirical finance gets.

Second, buying and selling stocks based on whether the market was becoming more or less concentrated produced lower returns and higher volatility than simply holding through.

Third, a handful of giants can be about as “diversified” as hundreds of smaller companies. Since 1926, it has taken an average of 230 small stocks to match the market value of just the three largest constituents. Yet the two groups had roughly the same volatility.

Why? There are a few economic reasons.

One is that concentration is a natural consequence of a power-law distribution in a well-functioning free-market economy. Successful companies grow, attract more capital, and become even larger.

Then there’s the fact that company concentration is not the same as economic concentration.

Today’s megacaps are so vertically integrated that they span dozens of industries, supply chain stages, and geos. Amazon is a great example: e-commerce and AWS sit under one ticker, but economically they are very different businesses.

And finally, dominant sectors naturally command larger market weights.

There are plenty of scary comparisons between tech-sector concentration today and 1999. But that analogy misses an important point: technology is no longer the narrow industry it was in the 1990s.

Just as energy accounted for nearly a third of the S&P 500 in 1980 because oil powered the economy, technology now sits underneath almost every major industry.

For some context, tech today accounts for roughly 10% of U.S. GDP and around one in every four dollars of S&P 500 earnings, which is more than twice its earnings share in 2000.

The bottom line is that nearly every bust involves some form of concentration. But very few periods of high concentration historically ended in a bust.

When they do, though, you’ll be damned...

- Dan Runkevicius, Editor

|

|

📈 Stocks head into earnings on a strong footing

Investors head into earnings season with growing confidence. Optimism around AI spending and corporate profitability continues to support markets, while an unusually high number of companies have issued positive earnings outlooks, bucking the typical wave of cautious forecasts that often precedes quarterly results.

🧊 Mag 7 loses momentum

The AI trade is still alive, but the biggest tech names are no longer leading it. Bloomberg data shows the Magnificent Seven, which include Nvidia, Amazon, and Alphabet, have underperformed 300 S&P 500 stocks this year, suggesting investors are becoming more selective as enormous AI spending plans begin to weigh on the group’s near-term performance.

🛢️ Oil remains at the mercy of geopolitics

Crude prices continue to swing on every development surrounding U.S.-Iran relations. Brent jumped more than 6% last week after President Trump declared the ceasefire was “over,” having risen more than 11% at one point during the week.

✈️ EasyJet takeover battle heats up

Budget airline EasyJet has received a $7.6 billion takeover proposal from Apollo Global Management, which tops a rival bid from Castlelake and sets the stage for a potential bidding war. EasyJet has already rejected four offers from Castlelake, arguing the firm was attempting to acquire the airline “on the cheap.”

🔥 Fed report signals inflation remains the priority

The Fed’s first Monetary Policy Report under Chairman Kevin Warsh emphasized rising inflation stemming from tariffs and higher energy prices. The report suggests policymakers remain cautious about declaring victory over inflation, with rate cuts off the table in the near term.

Can China pop the AI bubble?

DeepSeek's low-cost AI model, released in January 2025, erased hundreds of billions of dollars from U.S. tech stocks in a single day.

The concern wasn’t whether China was winning the AI race but whether AI was becoming so cheap that the expected payday from today’s spending might never arrive.

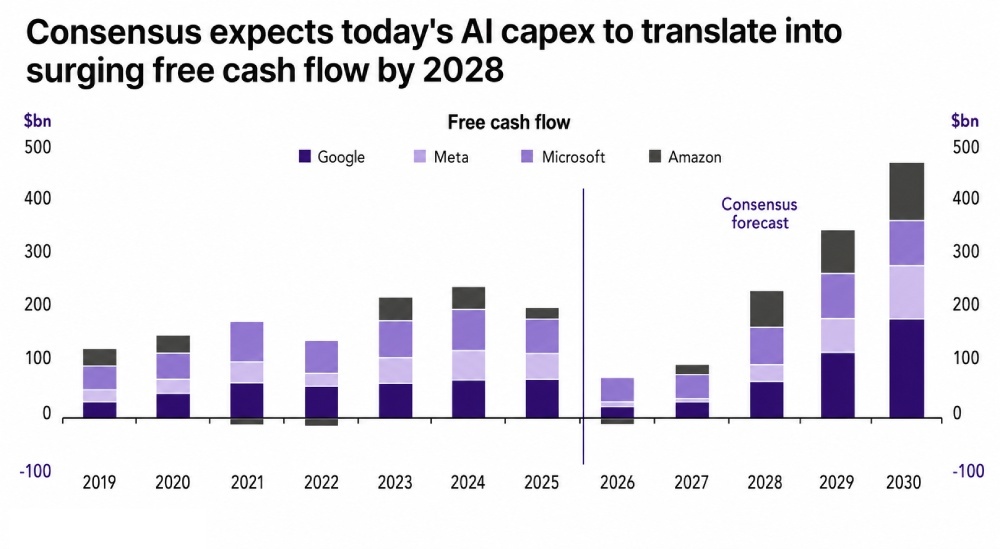

The market is pricing in a massive AI payday

Wall Street expects today’s AI investment boom to eventually become a cash machine.

The consensus estimate is for the combined free cash flow of Google, Microsoft, Meta, and Amazon to roughly double, from around $230 billion in 2028 to nearly $470 billion by 2030.

Much of that outlook depends on hyperscalers maintaining their pricing power after spending hundreds of billions of dollars on data centers, chips, and electricity.

DeepSeek changes the equation

DeepSeek suggests those assumptions may already be breaking down. Its models rival leading U.S. systems in reasoning and coding while costing a fraction as much to train and operate.

At the same time, AI token prices are falling. That is great for customers, but not so great for hyperscalers, because it means less revenue per AI query.

If AI becomes a commodity rather than a premium product, the biggest spenders may end up earning the weakest returns.

📌 Bottom line: The AI story has shifted from “Can we build it?” to “Can we earn enough from it?” DeepSeek has made that second question much harder to ignore.