Is Mag 7 the next AI trade?

Morning Observers,

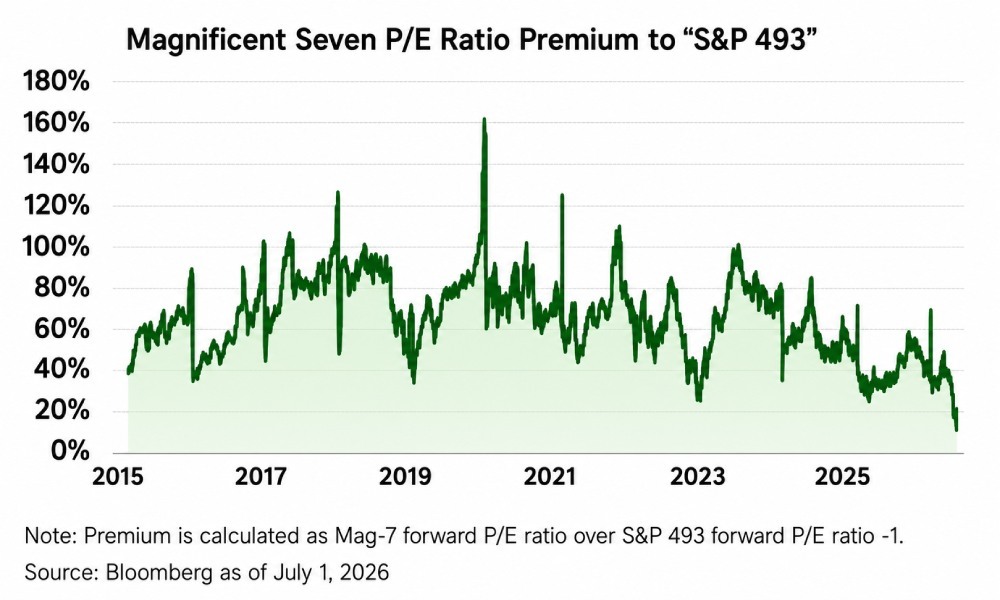

Magnificent 7 stocks have not been this cheap since 2015, and Wall Street has two bold theories about what that means.

For most of the past decade, Big Tech was a low-capital-intensity business that could grow with relatively little marginal cost and print money left and right.

That combination of margins and scale potential commanded a hefty premium for Big Tech versus the rest of the S&P 500.

See the chart below. Since 2015, investors have typically paid between 40% and 100% more for every dollar of Mag 7 earnings than for every dollar of earnings from the rest of the S&P 500.

Now, the Mag 7 (including Nvidia) is effectively trading like an average stock. So what happened? Two theories.

Morgan Stanley’s Lisa Shalett thinks this is an AI maturation phase where investors no longer blindly buy everything tied to AI. Instead, they are lurching between bottlenecks, trying to pinpoint which companies are actually making money from AI.

The problem is that this hopping around the AI supply chain has morphed into one recurring theme: Sell AI spenders and buy AI receivers. And the Mag 7 became the poster kid for the former.

Big Tech capex has already absorbed much of the free cash flow, pushing some companies to raise debt, and in some cases, even issue new shares for the first time in decades.

That is one reason Mag 7 stocks are now trading like the average stock.

In Lisa's view, though, this overlooks Big Tech's earnings growth and their important role as "AI orchestrators," which is more immune to LLM commoditization and productive gains than the rest of AI stocks.

The other theory is that this is the final leg of the AI bubble.

J.P. Morgan’s Jason Hunter argues that this rotation out of spenders and into the stocks on the receiving end of their spending is exactly what happened in the lead-up to the dot-com bust.

In 1999, telecom equipment suppliers ripped higher, while the companies making the huge capital investments were the first to drop. A few years later, the whole bubble unraveled.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🔻 Chipmakers tumble as AI doubts deepen

Chip stocks led the market lower on Tuesday as investors continued questioning whether massive AI spending will generate enough returns to justify lofty valuations. The Philadelphia Semiconductor Index, a closely watched benchmark for the sector, tumbled 4.7% and is now down 17% from its recent peak, adding fresh pressure to the broader market.

🚀 Nasdaq drops despite SpaceX debut

The tech sell-off pushed the Nasdaq-100 down 1.2% on Tuesday, overshadowing SpaceX’s addition to the index. Shares of Elon Musk’s rocket and AI company fell more than 6%, sending its market capitalization below $2 trillion. The stock is now down roughly 25% from its post-IPO closing high as investor enthusiasm around high-growth tech continues to cool.

📦 U.S. trade deficit hits one-year high

The U.S. trade deficit widened sharply in May, reaching its largest level in more than a year as imports jumped. The gap increased 42.2% from the previous month to $77.6 billion, according to Commerce Department data. Economists say businesses may be accelerating imports ahead of potential new tariffs after President Donald Trump’s trade policies prompted companies to reshuffle supply chains.

⚡ Rivian sinks after announcing share sale

Rivian stock plunged more than 18%, its biggest one-day decline in over a year, after the electric vehicle maker announced plans to sell 75 million new shares. Rivian said the capital will help fund its obligations under an amended U.S. Department of Energy loan agreement, raising cash needed to access federal financing for its manufacturing expansion. The share sale will also dilute existing shareholders, adding to the stock’s decline.

🛢️ Oil jumps as Hormuz tensions flare

Oil prices climbed more than 2% Tuesday after reports of an Iranian attack on commercial vessels in the Strait of Hormuz, underscoring the fragile state of the U.S.-Iran ceasefire. WTI crude rose back above $70 a barrel, while Brent crude approached $74 a barrel, as traders weighed the risk of further disruptions to the world’s most important energy shipping route.

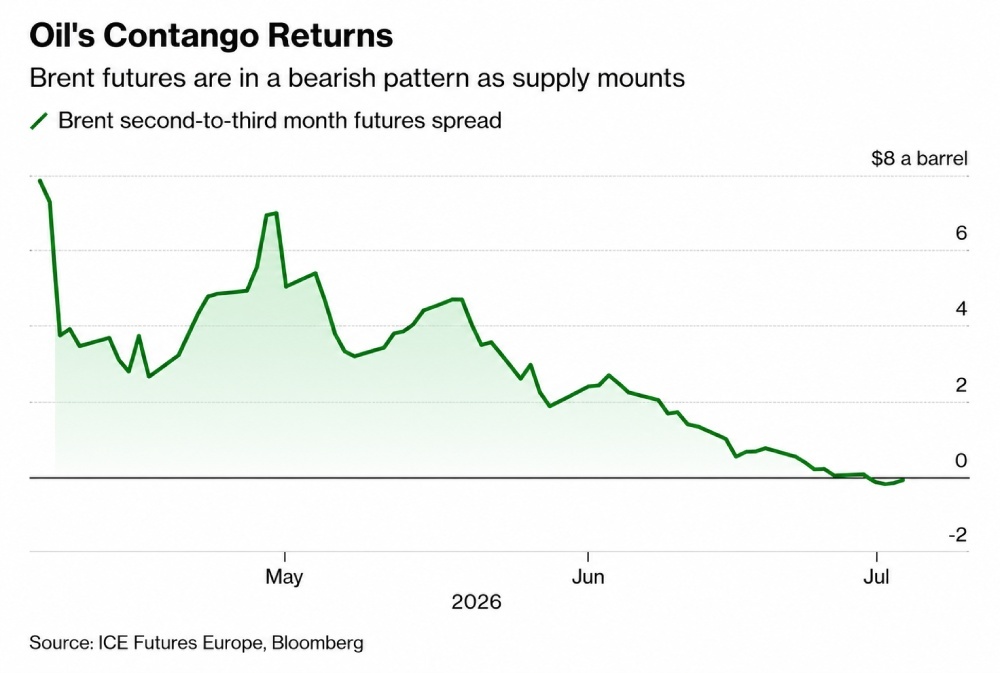

Oil suddenly has a new problem

Instead of worrying about finding enough oil, the market is starting to worry about finding enough buyers, according to JPMorgan commodity strategist Natasha Kaneva.

“A wave of oil is about to enter the market,” she wrote in a recent note. “And here lies the paradox. The surge in oil supply is about to collide with a market that, at least for now, simply does not need it.”

The futures market is already pricing in that shift.

Brent’s second-to-third-month spread has collapsed from roughly $7 a barrel in April to around zero, pushing the market back toward contango.

Contango simply means traders are no longer paying a premium for oil today because they expect plenty of it tomorrow.

That shift is one reason U.S. crude has recently fallen back below $70 a barrel, roughly where it traded before the U.S. and Israel launched strikes on Iran in late February.

The market is looking past the war.

The physical market is telling the same story.

Roughly 14 million barrels of oil moved through the Strait of Hormuz on July 1, a sign that the world’s most important shipping lane is gradually returning to normal.

Saudi export flows have recovered to about 90% of their pre-conflict pace, while alternative routes through the Red Sea and the UAE’s Fujairah port continue moving another 6.2 million barrels per day.

The contingency plans built during the Iran war never disappeared.

Now they are operating alongside traditional export routes, adding even more supply to a market that is already well stocked.

Unless demand rises, particularly from China, or governments step in to rebuild strategic reserves, the market could struggle to absorb the extra crude.

📌 Bottom line: Unless global demand surprises to the upside, geopolitics may no longer be the biggest driver of crude prices. Basic supply and demand may be taking over.

Did China just fix its housing affordability problem?

For decades, policymakers assumed housing bubbles had to be rescued. China may have just challenged that assumption.

The bubble burst, but the economy didn’t

China’s real residential property price index,has fallen from roughly 113 in 2021 to about 84 today, leaving inflation-adjusted home prices below their mid-2000s levels.

In other words, much of China’s housing boom has now been erased in real terms. Macro analyst Kathleen Tyson called it “a success for the history books.”

Normally, housing corrections of this size end in a banking crisis or recession. Yet China still reported 5% economic growth in 2025, hitting its official target despite a property downturn that many thought would cripple the economy.

Instead of trying to rescue housing, Beijing shifted focus toward manufacturing, exports, infrastructure investment, and fiscal support.

The real lesson for America

The U.S. faces a unique problem: home prices remain at historically elevated levels, mortgage rates are high, and affordability is near multi-decade lows.

For America, the challenge isn’t just that housing is expensive but that home prices have become one of the economy’s main growth engines.

That leaves the Fed with an uncomfortable tradeoff. Lower home prices would improve affordability, but they could also weigh on consumer spending, construction, lending, and household wealth.

Unlike China, the U.S. is still trying to bring inflation down without meaningfully bringing home prices down, too.

📌 Bottom line: China didn’t show that housing busts are harmless. It showed that fixing affordability is survivable when the entire economy isn’t built on ever-rising property values.