Iran deal rally is on!

Morning Observers,

Trump had three big red lines on Iran: no uranium enrichment, no ballistic missile program, and no access to frozen assets. Yet he walked back all three to land the deal yesterday.

At his G7 press conference in France, Trump said Tehran should be allowed to enrich uranium for civilian use, keep at least some ballistic missiles, and eventually regain access to frozen funds.

So what changed?

The simple answer is that Trump may have discovered the one thing more dangerous than looking soft on Iran: looking responsible for a global energy shock.

And that’s exactly what markets were pricing in.

Although oil reserves and inventories helped cushion part of the shock, one of the reasons markets didn’t go into full panic mode is that they knew Trump wouldn’t dare to let all hell break loose.

And that if Washington failed to hammer out a deal with Tehran, Trump at some point would give Iran all the concessions it wants to get the Strait reopened.

The second thing markets were pricing in, which I wrote about last month, was that Tehran had a much higher pain tolerance than Washington.

If Trump doesn’t change his mind in the next 60 days, apparently they were right. For all the risk of getting torched for one of the biggest foreign policy mistakes in decades, Trump chose the economy...

... or let's be honest, probably the stock market.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🏦 Fed leaves rates unchanged

As expected, the Fed left interest rates unchanged at Kevin Warsh’s first meeting as chair, but the bigger story was his decision to skip the central bank’s closely watched “dot plot” forecast. Warsh had previously argued that publishing individual rate projections limits the Fed’s flexibility. He also glossed over the path of rates and left a lot open to interpretation.

🚀 SpaceX snaps IPO winning streak

SpaceX shares fell 5% on Wednesday, ending a three-day surge that pushed the company past Amazon as the world’s fifth-largest by market value. Even after the pullback, the stock remains up 29% since last Friday’s IPO, with Elon Musk’s rocket and AI company now valued at roughly $2.5 trillion.

🛍️ U.S. retail sales exceed forecasts

Despite higher gasoline prices and persistent inflation worries, U.S. consumers continued to open their wallets in May. Retail sales rose 0.9%, beating forecasts for a 0.5% increase and marking a fourth straight monthly gain. Spending increased across a broad range of retailers, while gas station receipts climbed 3.4%.

📉 Dow hits record high, then reverses

The Dow Jones Industrial Average climbed above 52,000 for another record high, outperforming the broader market for a second straight session, but lost momentum in the final hours as markets reacted to the Fed rate decision and Warsh’s hawkish comments.

🔥 ECB official warns of inflation resurgence

ECB policymakers are growing more cautious about inflation. Official Olaf Sleijpen warned that a repeat of the 2022 inflation shock appears less likely but can’t be ruled out as higher energy costs continue to ripple through the economy. Eurozone CPI accelerated to 3.2% in May, the highest reading since 2023, forcing the central bank to raise interest rates.

Qualcomm: Last chip value play?

AI has made cheap chip stocks almost impossible to find, but Qualcomm may be one of the few exceptions. The reason: Wall Street still views it as a smartphone company.

The AI stock without the AI multiple

In April, Qualcomm revealed it had landed a mystery hyperscaler customer for its new data center chips, sending the stock up 40%. For a brief moment, the company looked like it was joining the data center club and was being priced accordingly.

Yet even after that rally, Qualcomm is up just 5% over the past two years. The PHLX Semiconductor Index has surged roughly 150% over the same period.

The result is one of the widest valuation gaps in the semiconductor industry.

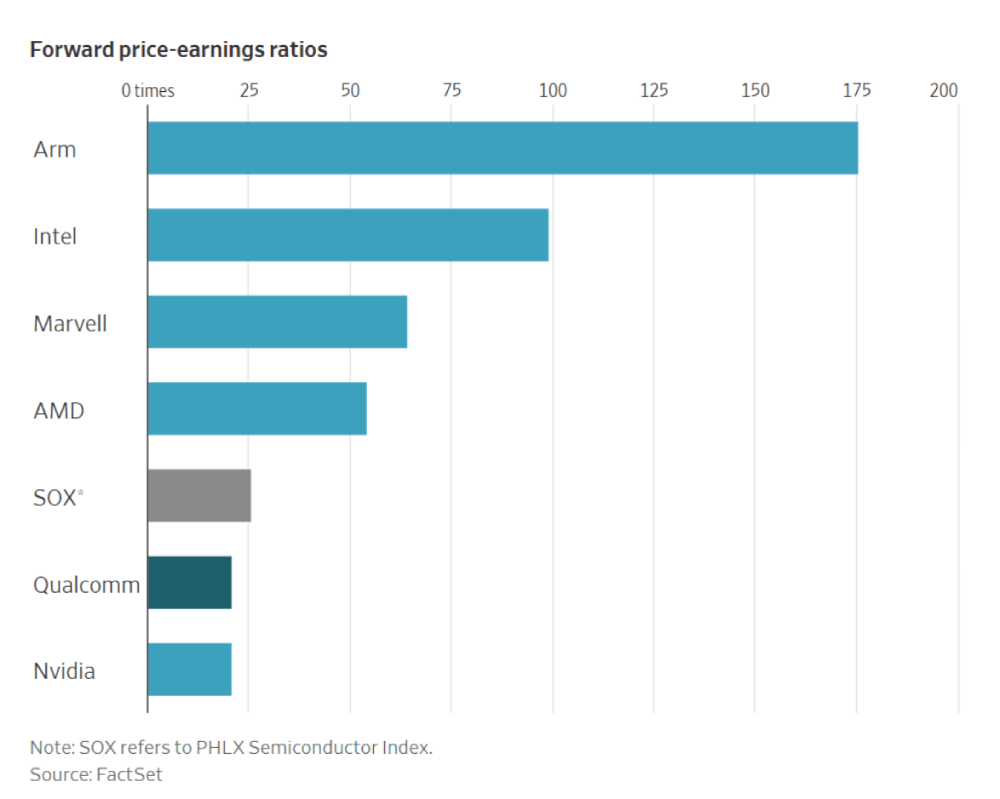

Qualcomm trades at just 21x forward earnings. That’s below the semiconductor index itself at 26x, and far below Arm at 175x, Intel at 100x, Marvell at 64x, and AMD at 54x.

The contrast is especially striking with Arm. It has also expanded into data center chips, yet investors value it at more than eight times Qualcomm’s multiple.

A valuation that assumes AI doesn’t matter

Investors still see Qualcomm as a smartphone-focused company, with handsets generating most of its revenue.

With IDC forecasting a 14% decline in global smartphone shipments this year, that perception continues to weigh on the stock despite the company’s expansion into other lucrative markets.

The irony is that Qualcomm’s diversification started years ago.

Since Cristiano Amon became CEO in 2021, Qualcomm has pushed aggressively into automotive chips. Automotive revenue has climbed to $1.3 billion from just $240 million five years earlier, giving the company another growth engine beyond smartphones.

📌 Bottom line: If Qualcomm’s data center business gains traction, the stock may have to catch up to AI multiples … and that gap is where the opportunity lies.

The dollar’s biggest backer isn’t the Fed

AI has made cheap chip stocks almost impossible to find, but Qualcomm may be one of the few exceptions. The reason: Wall Street still views it as a smartphone company.

The AI stock without the AI multiple

In April, Qualcomm revealed it had landed a mystery hyperscaler customer for its new data center chips, sending the stock up 40%. For a brief moment, the company looked like it was joining the data center club and was being priced accordingly.

Yet even after that rally, Qualcomm is up just 5% over the past two years. The PHLX Semiconductor Index has surged roughly 150% over the same period.

The result is one of the widest valuation gaps in the semiconductor industry.

Qualcomm trades at just 21x forward earnings. That’s below the semiconductor index itself at 26x, and far below Arm at 175x, Intel at 100x, Marvell at 64x, and AMD at 54x.

The contrast is especially striking with Arm. It has also expanded into data center chips, yet investors value it at more than eight times Qualcomm’s multiple.

A valuation that assumes AI doesn’t matter

Investors still see Qualcomm as a smartphone-focused company, with handsets generating most of its revenue.

With IDC forecasting a 14% decline in global smartphone shipments this year, that perception continues to weigh on the stock despite the company’s expansion into other lucrative markets.

The irony is that Qualcomm’s diversification started years ago.

Since Cristiano Amon became CEO in 2021, Qualcomm has pushed aggressively into automotive chips. Automotive revenue has climbed to $1.3 billion from just $240 million five years earlier, giving the company another growth engine beyond smartphones.

📌 Bottom line: If Qualcomm’s data center business gains traction, the stock may have to catch up to AI multiples … and that gap is where the opportunity lies.