Iran deal is off to a bumpy start

Morning Observers,

Well, that didn’t take long...

The Iran deal is off to a bumpy start after the U.S. and Iran postponed Friday’s talks in Switzerland over a permanent peace agreement and new limits on Tehran’s nuclear program.

The official explanation is logistics, but the real reason may be Netanyahu.

Last night, Israel and Hezbollah traded fire in Lebanon, and Lebanon’s state media said 16 people were killed. Iran is still insisting that a Lebanon ceasefire is part of the deal it just signed with Washington.

That puts Trump in the exact spot he was trying to avoid.

He needs Iran to keep the Strait of Hormuz open. But Israel is still hitting Hezbollah, Netanyahu doesn’t want to pull troops back until he’s sure northern Israel is safe, and Trump is reportedly furious that Israeli strikes nearly blew up the MOU he just sold as a breakthrough.

So no, the deal isn’t dead. Brent is still near $80, and ships carrying stranded Persian Gulf oil are finally starting to move through Hormuz again. That’s the good news.

The bad news is that this whole arrangement now depends on Israel’s tolerance for restraint, Iran’s willingness to limit enrichment, and Trump not changing his mind.

In other words, the stock market may have gotten the relief rally. Now comes the part where everyone has to pretend this deal will actually come through.

P.S. Don’t skip your new favorite “Guess the chart” segment at the end. This one’s pretty tricky. Good luck!

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🛢️ Oil’s great unwind continues

Oil prices extended their decline Thursday. U.S. crude fell 3.5% to the low-$74 range while Brent dropped 3.1% to around $77, leaving prices roughly 35% below their recent highs. This morning, prices are slightly up after the news came out about postponed Iran talks in Switzerland.

🤖 Amazon takes on Nvidia

Amazon is exploring a bigger role in the AI semiconductor race, holding talks to sell its custom-designed chips for use in other companies’ data centers. The move would challenge Nvidia’s dominance in AI hardware and expand Amazon’s ambitions beyond its own cloud business. Shares rose nearly 2% after the news.

🏦 Bank of England stands pat

The Bank of England left interest rates unchanged at 3.75%, pointing to falling oil prices as an encouraging sign for inflation. Two policymakers pushed for a rate hike over stubborn inflation. The decision came one week after the European Central Bank hiked rates, citing growing inflation concerns.

📈 Stocks rebound after Fed selloff

U.S. stocks bounced back Thursday after the previous session’s selloff, when the Fed signaled that interest rate hikes were more likely than cuts later this year. Technology led the recovery, with the S&P 500 tech sector climbing more than 2.6% and the Nasdaq gaining 1.9%.

🎮 Take-Two gets a GTA boost

Take-Two Interactive shares climbed nearly 5% after the company announced Grand Theft Auto VI pre-orders will open June 25, kicking off the launch of arguably the most anticipated video game ever. The title is scheduled for release on Nov. 19 and is expected to provide a multibillion-dollar boost for the publisher. For perspective, Grand Theft Auto V has generated roughly $10 billion in revenue since its 2013 debut.

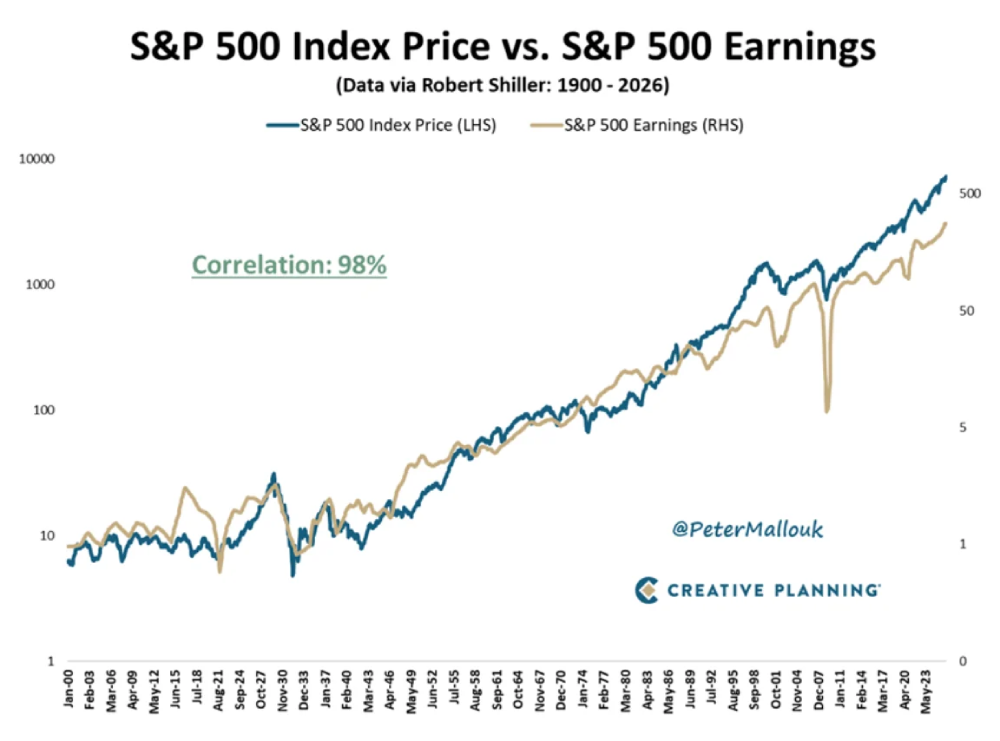

The stock market’s biggest driver hasn’t changed in 120 years

Wall Street spends a ridiculous amount of time forecasting interest rates, tariffs, and elections. But more than 120 years of market history suggest investors should spend more time reading earnings reports.

That matters because the S&P 500 is in the middle of one of its strongest earnings expansions in years.

98% correlation

Creative Planning CEO Peter Mallouk compared more than 120 years of stock prices and corporate earnings using Robert Shiller’s historical dataset and found something remarkable:

A 98% correlation between the two.

Stocks are ultimately claims on business profits, not headlines. Revenue growth grabs attention, but earnings growth is what has tracked stock prices for more than a century.

As companies generate more profit, investors have historically been willing to pay higher prices for their stock.

That’s why Warren Buffett has always prioritized profitability. Highly profitable businesses can fund their own growth, survive downturns, and widen their moats over time.

The S&P 500 earnings boom

That long-term relationship matters now more than ever because we are in one of the strongest earnings periods in decades.

S&P 500 companies delivered 29.4% year-over-year earnings growth in the first quarter, according to LSEG, extending a sixth consecutive quarter of double-digit growth.

At the same time, revenue grew 11.4% on average, showing that earnings aren’t being driven by cost cuts alone.

This earnings growth runs against widespread concerns that elevated interest rates and tariffs would squeeze margins. But the reality is that AI spending is translating into higher productivity, while Big Tech continues to capture an outsized share of corporate profits.

📌 Bottom line: Investors spend countless hours trying to predict the next Fed meeting or geopolitical headline, yet more than a century of market history suggests a simpler approach: follow earnings.

The Fed stopped giving hints… but markets guessed anyway

Kevin Warsh’s first statement as Fed chair was just 132 words, the shortest since Alan Greenspan and barely a third the length of April’s.

Stocks fell, bond yields jumped, and the consensus was immediate: the new chair is more hawkish than expected. But several veteran investors argue the market is solving the wrong puzzle.

Markets are reading yesterday’s Fed the old way

For more than a decade, investors were trained to treat every Fed statement as a puzzle. Every word mattered because the Fed wanted markets to know where interest rates were heading.

Warsh appears to be rejecting the game altogether.

Altus Wealth Management strategist James E. Thorne argues investors are still searching for rate signals even as Warsh questions whether the Fed should be sending them at all.

“The result is a growing mismatch between what markets think they are hearing and what is actually being said,” Thorne wrote.

If he’s right, investors aren’t just misreading sentences; they are misreading the institution itself.

Premature reaction?

There’s another problem with the hawkish narrative: the bond market may be getting ahead of itself.

After the meeting, Treasury breakeven rates, the bond market’s best real-time estimate of future inflation, had their biggest drop in two years. That means investors are betting inflation will fall off a cliff.

Azuria Capital founder Otavio Costa argues that this makes the market’s reaction to Warsh look premature.

Costa compares the reaction to the early excitement around DOGE, when investors priced in permanently smaller deficits before any meaningful spending cuts had occurred.

And yet Washington soon returned to business as usual, and the deficit kept growing.

The same logic applies to rates. With U.S. debt at historic levels, the economy is far more sensitive to higher borrowing costs than in the past. This limits how much hiking the Fed can actually do.

📌 Bottom line: Coming across as hawkish may be more about managing expectations and protecting the Fed’s credibility than signaling the future path of interest rates.