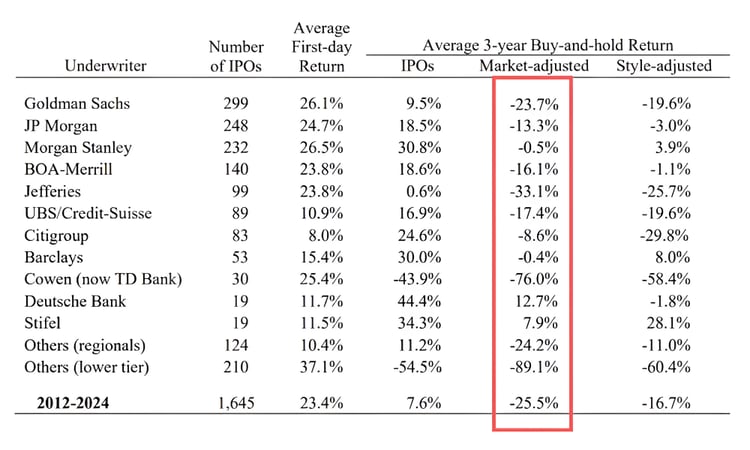

IPO returns are terrible

Morning Observers,

If you have your sights set on SpaceX, or any IPO for that matter, the table above is one of the biggest reality checks.

But to really get why this happens, let’s talk about how an IPO comes together and what it’s really for because it’s as much a liquidity event as it is a capital raise.

When a company wants to go public, it goes to a big investment bank like Goldman Sachs or JPMorgan, which becomes the underwriter.

The underwriter has three main tasks: do all the paperwork, help the company set the price, and find big investors willing to put in money at that price before the company is listed

Now this is where things get interesting. Take a look at the average first-day return in the table.

With just one exception, every IPO cohort in the table jumped double digits on its first day on public markets. Most of them were up 20%+.

This is called the “pop,” and it’s deliberately engineered by how underwriters set the price.

Investment banks often price IPOs at a discount to create more demand than supply, reward their initial investors, and help the deal hit the headlines as a success.

So when a stock jumps 20% on day one, that does not necessarily mean the company is successful. More often than not, it means underwriters correctly “lowballed” the stock.

The average investor doesn’t get to buy at the offer price because the stock has usually popped by the time they can place an order. So their more realistic buy price is the stock’s first-day closing price.

If we use that as the entry point to measure long-term returns, IPOs are one of the worst investments you can make.

Take a look at the average three-year returns in the table, which are calculated not from the offer price but from the first closing price.

From that entry point, the average IPO underperforms the market by 25.5% over three years. That means you are much, much better off just buying an ETF that tracks a broad index.

Interestingly, if we use the offer price as the entry point, the average IPO only slightly underperforms the broader market, but that’s a far cry from 25.5%. Besides, institutional investors can exit much earlier.

So while IPOs can be a great deal for underwriters and their clients, they rarely are for investors like you and me.

- Dan Runkevicius, Editor

Five things to know before opening bell

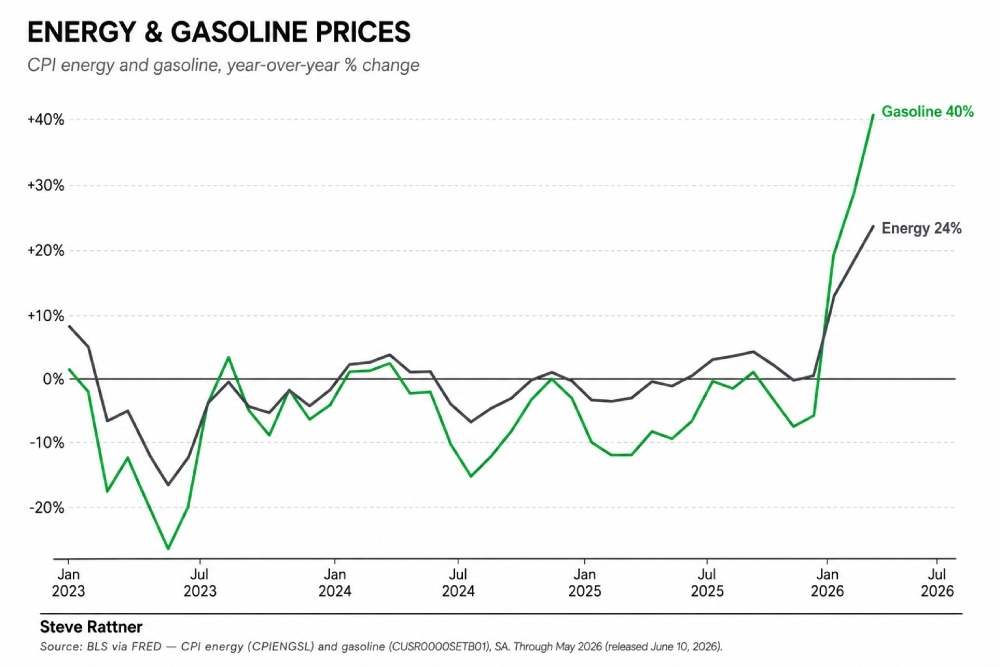

🔥 U.S. CPI climbs to 4-year high

U.S. inflation reached 4.2% in May, the fastest pace in four years, driven by higher energy prices linked to the Iran war. Core inflation, however, remained relatively restrained, rising 0.2% on the month and 2.9% annually. The reading adds another complication for the Federal Reserve, which has now spent more than five years with inflation above its 2% target.

🏦 Bank of Canada holds rates steady

The Bank of Canada left its benchmark interest rate unchanged at 2.25%, even as the economy slipped into a technical recession during the first quarter. After aggressively cutting rates over the past two years, policymakers are now pausing amid renewed inflation concerns. Governor Tiff Macklem said the central bank is closely monitoring its preferred core inflation measures, which have been trending higher and complicating the outlook for future cuts.

🚚 Amazon shakes up the trucking industry

Trucking stocks tumbled on Wednesday after Amazon unveiled an expansion of its shipping business, raising concerns that the e-commerce giant is becoming an even bigger force in logistics. Shares of Old Dominion Freight Line, FedEx, and Saia each fell roughly 10% in early trading. Morgan Stanley analyst Ravi Shanker said Amazon could capture meaningful market share even before matching competitors on service quality.

🛢️ U.S. crude inventories keep falling

U.S. crude and distillate inventories dropped by nearly 7.3 million barrels last week, marking a seventh straight weekly decline and exceeding expectations for a 4 million barrel draw. Including strategic reserves, total inventories have fallen by roughly 79 million barrels since late February.

🏭 Chinese wholesale inflation nears 4-year high

China’s producer price index climbed 3.9% in May from a year earlier, reaching its highest level since July 2022 as higher raw material costs pushed wholesale prices higher. Consumer inflation, however, held steady at 1.2%, suggesting companies are absorbing much of the increase instead of passing it on to shoppers.

The case against the inflation panic

4%+ inflation is supposed to send markets into a tailspin. Historically, it has. But May’s CPI report raises a different possibility: What if headline inflation is getting worse while underlying inflation is subsiding?

Underlying inflation is rolling over

With energy driving roughly 60% of May’s CPI surge, the rest of the report told a very different story:

- Core inflation, excluding food and energy: +0.2%

- Commodities excluding food and energy: -0.11%

- New vehicles: -0.26%

- Medical care commodities: -0.71%

- Used cars: 1.99% lower year over year

This is the furthest thing from an economy mired in a broad-based inflation shock.

“Inflation has peaked, and we will slowly but surely see that reflected in the data over the coming months,” said Real Vision macro analyst Andreas Steno Larsen.

By his estimates, headline inflation is currently running at around 0.45% month-over-month, versus roughly 0.24% for core inflation.

There are two reasons for this. First, producers aren’t yet passing higher costs on to consumers. Second, inflation expectations are destroying demand in what looks like a self-fulfilling prophecy.

Goldman Sachs largely agrees, but expects inflation to peak closer to 4.4% before rolling over. If the war ends sooner than expected, the bank sees inflation falling back toward 2% next year.

“Our economists have not seen any signs that the inflation shock from the war is broadening out,” Goldman said.

That should give the Fed some breathing room after 63 consecutive months of inflation above its 2% target.

📌 Bottom line: Energy inflation is eroding purchasing power, but it isn’t the same thing as broad inflation. The consensus may be overestimating how high prices ultimately go.

The $19 trillion productivity bet

AI-linked tech stocks are now worth roughly $19 trillion, according to Goldman Sachs.

And while many investors are pouring money into what they expect to become the defining technology of the century, the real bet isn’t that AI changes the world…

It’s that it does so in just a few years instead of a few decades.

If the expected productivity surge takes longer to arrive, today’s AI boom could become one of the largest capital misallocations in history.

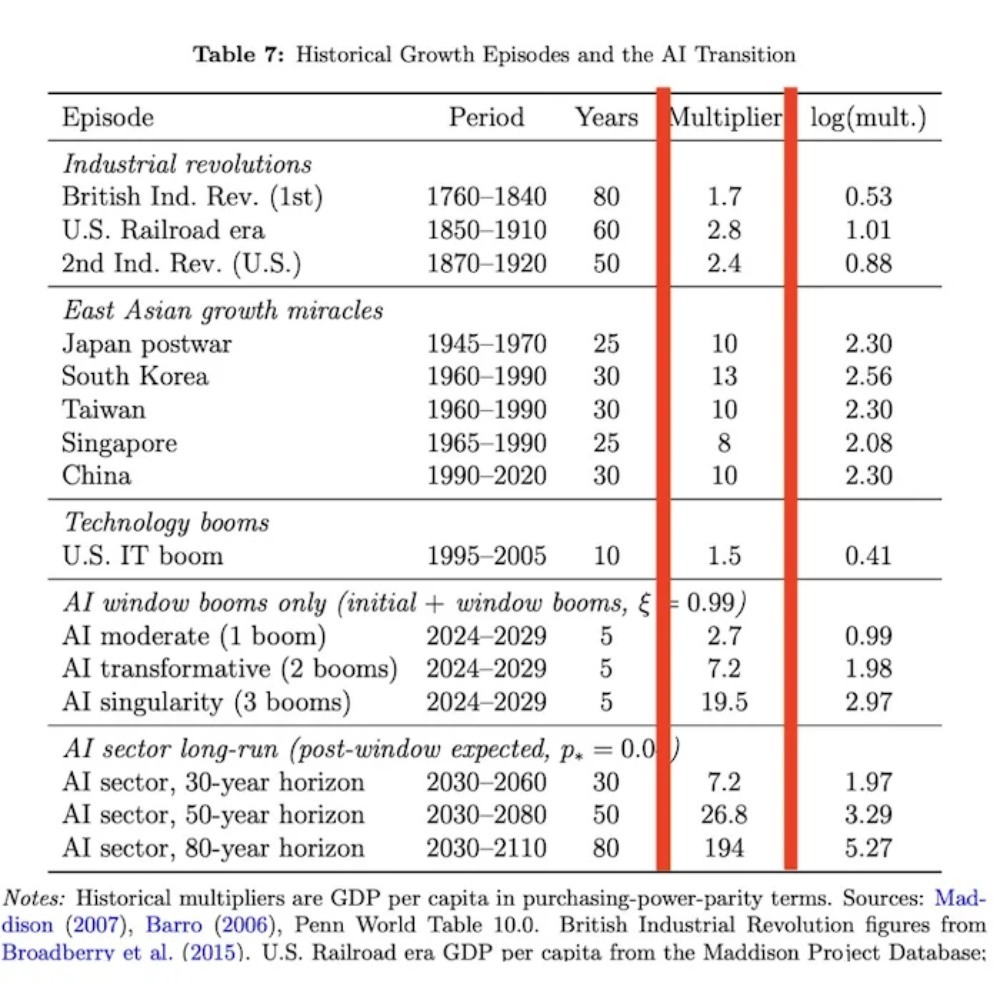

Big Tech is betting on a once-in-history outcome

In a recent paper, Wharton researchers called AI a trillion-dollar gamble for Big Tech because today’s spending assumes the technology will deliver a 2.7x productivity boom in just five years.

For context, that’s roughly equivalent to the entire U.S. railroad era or the British Industrial Revolution compressed into a single presidential term.

More aggressive scenarios imply productivity gains of 7.2x or even 19.5x. None of these assumptions looks realistic.

This means AI investors aren’t really paying up for better chatbots or smarter search engines. They are effectively banking on the fastest productivity acceleration in modern economic history.

So far, Goldman Sachs says the productivity payoff hasn’t shown up in the data.

“We still do not find a meaningful relationship between productivity and AI adoption at the economy-wide level,” Goldman said after analyzing fourth-quarter corporate earnings results.

OpenAI could be the canary in the coal mine

There are already signs that the productivity story isn’t unfolding as quickly as investors hoped. OpenAI has reportedly complained internally that it’s missing revenue and usage targets.

That’s why recent reports about the company discussing a government equity stake deserve attention.

Sam Altman first floated the idea with the Trump administration last year, proposing that equity could seed a “public wealth fund” outlined in OpenAI’s April policy proposal.

But considering that OpenAI is losing billions and has no clear path to profitability, it looks less like an investment for taxpayers and more like a bailout at their expense.

📌 Bottom line: AI has become a $19 trillion productivity bet. As that bet gets tested, investors are likely to place a much higher premium on companies that can point to higher margins, lower costs, and faster growth rather than bigger AI budgets.