Global economy is breaking apart

Morning Observers,

The Hormuz shock is splitting the global economy down the middle, and the early signs are showing up in one of the "nerdiest" trades.

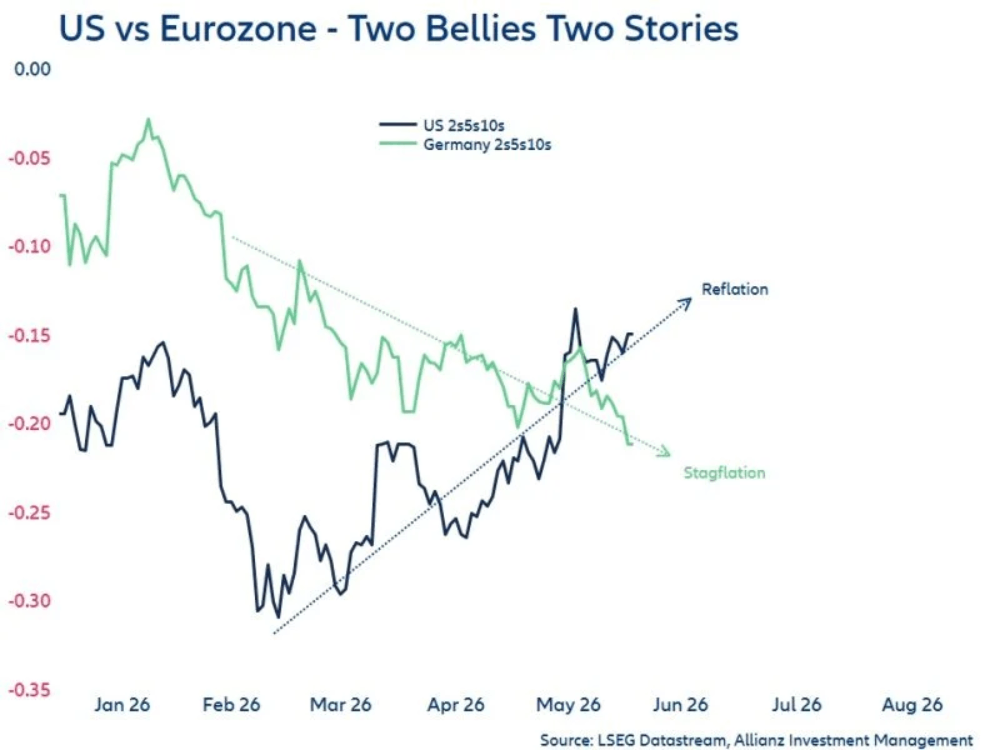

Below is a chart of the so-called 2s5s10 butterfly in U.S. debt and German debt:

What it shows in plain English is the difference between the 5-year yield (aka the “belly”) and the 2-year and 10-year yields (aka the “wings”) in both countries.

If 5-year yields are rising relative to 2s and 10s, the line plots higher in this chart. And vice versa.

The “belly” is important because this is the part of the bond market most sensitive to expectations for the next few years. Not the next Fed meeting, not the 30-year future, but things like rate changes, inflation, economic growth, etc.

And as you can see in the chart, the “bellies” of Germany and the U.S. are pointing to very different futures.

In the U.S. case, 5-years are rising relative to the wings. But in Germany, they’ve been moving down since the Iran war.

That means the market is betting that the U.S. will keep rates higher in the next few years. And that can only happen in one post-Hormuz scenario: reflation (where both inflation and economic growth are picking up).

That’s good news for the U.S.

On the other hand, the eurozone is expected to cut rates in the next few years. That means Europe may not be able to absorb inflation from Hormuz without falling into a recession, aka stagflation.

That’s bad news for Europe.

This split isn’t unexpected. Europe’s growth is much slower, it’s more exposed to energy shocks because it imports most of its energy, and it doesn’t have the AI capex boom that most of U.S. growth is resting on.

Is the world outperformance of the U.S. over at this point?

— Dan Runkevicius, Editor

Five things to know before opening bell

🛢️ Oil climbs toward $100 a barrel

Oil prices pushed above $100 yesyerdya before coming down to $95 over new tensions between Iran and the United States, tempering hopes for a lasting ceasefire. While both sides have agreed to a preliminary framework to extend the truce and reopen the Strait of Hormuz, negotiations over final terms remain unresolved.

📉 Stocks pull back from record high

U.S. stocks pulled back from record highs, with software stocks extending losses for a second consecutive session and financial shares also moving lower. Strength in energy stocks helped offset bigger losses as investors rotated toward sectors benefiting from higher crude prices.

💼 U.S. employment growth accelerates

Private-sector hiring picked up in May, with employers adding 122,000 jobs, exceeding economists’ expectations. Unlike previous months, when gains were concentrated in healthcare and a handful of industries, hiring was more broadly distributed across sectors. The report suggests labor market conditions remain resilient despite ongoing economic uncertainty.

🏙️ U.S. services sector expands faster than expected

The U.S. services sector, which accounts for roughly three-quarters of economic activity, grew faster than expected in May. The ISM Services PMI rose to 54.5 from 53.6, remaining comfortably above the 50 threshold that signals expansion. However, some of the strength may reflect businesses pulling forward orders and building inventories ahead of potential supply disruptions and higher costs tied to the Iran war.

⚠️ Private credit fears coming back

Alternative asset managers sold off on Wednesday after Cliffwater’s flagship private credit fund reported redemption requests equal to 17% of assets. The news reignited concerns about liquidity across the private credit industry, sending shares of Blackstone, KKR, Blue Owl, Apollo, and Ares down more than 4% intraday. The selloff highlights a growing investor fear: private credit has never been tested by a prolonged wave of withdrawals.

Tariff inflation has become a self-fulfilling prophecy

When economists think about tariffs, they usually focus on prices. But according to a new Fed paper, the bigger story may be consumer behavior.

The Fed scoured transactions from more than 125,000 U.S. households following the 2025 “Liberation Day” tariffs and found an interesting phenomenon.

While tariffs did raise prices, the increase was surprisingly modest. Retailers passed through only about 15% to 20% of the tariff cost, resulting in consumer price increases of roughly 1% to 2%.

Yet spending on those same goods fell by around 4%.

In other words, households cut spending by roughly three to four times the size of the actual price increase.

The middle class pulled back

Contrary to what you’d expect, it wasn’t low-income households that led the pullback. In fact, middle-income consumers accounted for much of the adjustment.

Rather than absorbing higher prices, they started trading down to cheaper products and shifting spending toward essentials.

Lower-income households had less room to make those adjustments because a larger share of their budgets was already dedicated to necessities.

The findings suggest consumers weren’t simply responding to higher prices. They were responding to the fear of higher prices.

Tariffs may be disinflationary at first

The study also helps explain one of the more puzzling developments of 2025: why inflation initially remained relatively contained despite the largest tariff increase in decades.

If consumers immediately cut discretionary spending, demand weakens. And when demand weakens, companies have less ability to pass higher costs on to customers.

This aligns with separate research from the San Francisco Fed, which found that inflation often drops immediately after tariffs are imposed, then rises later as higher costs gradually work their way through the economy.

Whether that pattern ultimately plays out this time remains an open question.

📌 Bottom line: Tariffs have taken a back seat to the war in Iran, but they are still very much in play. The Fed’s research, however, suggests they may be less of an inflationary threat than a demand dampener.

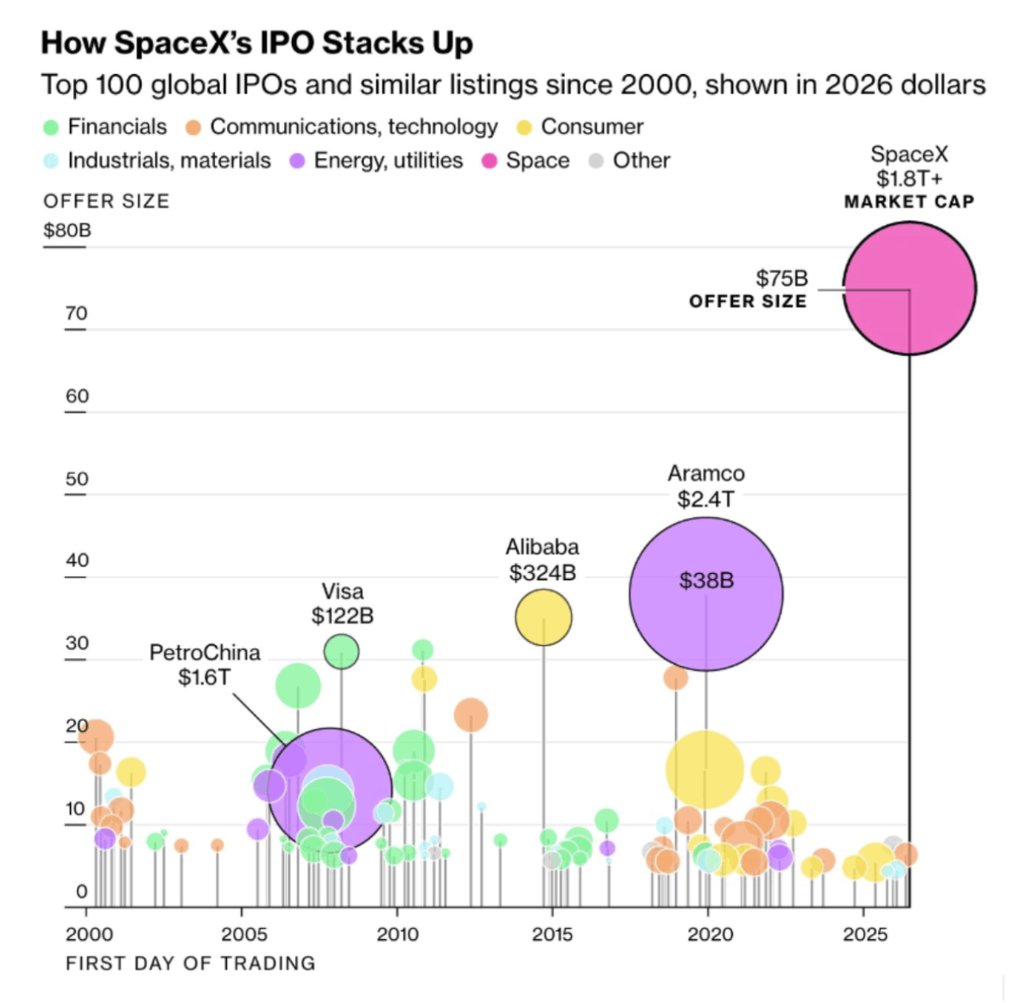

The world’s biggest IPO has a problem

Elon Musk’s SpaceX is preparing what could become the largest IPO in history.

At a targeted valuation of more than $1.8 trillion, the company would surpass the scale of Saudi Aramco’s record-setting debut and immediately become one of the world’s most valuable public companies.

There’s just one catch: unlike Aramco, SpaceX isn’t making money.

Aramco earned it… SpaceX still has to prove it

When Saudi Aramco went public in 2019, it generated roughly $330 billion in annual revenue and $88 billion in profit. Its valuation was about $1.7 trillion.

And yet, SpaceX wants an even higher valuation despite losing money.

To be fair, one part of the business is already working. Starlink, SpaceX’s satellite internet division, generated about $11.4 billion in revenue and $4.4 billion in operating income last year.

The problem is that SpaceX’s other businesses are still consuming cash. Space and rocket launch operations lost roughly $657 million, while xAI lost another $6.4 billion.

That means SpaceX would rank among the ten most valuable companies on Earth despite only one major segment producing an operating profit.

And based on Starlink’s earnings alone, investors would be paying hundreds of times current operating income.

📌 Bottom line: SpaceX could become one of the most important companies of the next decade and still be a disappointing investment at the wrong price.