Fed can "cut" rates today

Morning Observers,

Here’s how new Fed chair Kevin Warsh can “cut” or “raise” rates today without actually cutting or raising them.

As Trump’s (widely presumed) sock puppet, Warsh will chair his first Fed meeting from one of the trickiest positions imaginable.

Trump wants lower rates. Warsh may want lower rates, too. But even if he wanted to push for cuts today, he would struggle to find even the flimsiest reason to justify them.

Inflation is rising across the board, unemployment is surprisingly bouncing back, and the market is in full-on speculation mode. Just look at SpaceX.

Trump’s constant attacks against the Fed have already dented its credibility. But a Warsh cut in this environment would effectively destroy it and, counterintuitively, raise rates.

How so? That brings us to how Warsh can “cut” or “raise” rates without convincing the FOMC to make any changes.

The Fed controls the overnight rate. But the rates that matter most, like the 10-year Treasury yield, which is effectively the benchmark for everything from mortgage rates to corporate borrowing costs, are set by the market.

That rate is a combination of two things: expected Fed rates plus the term premium (or the extra compensation investors demand for holding long-term debt).

For example, since Trump’s election, the overnight rates have dropped by 1 percentage point. And yet the 10-year yield has barely budged because the term premium has risen.

That’s where Warsh’s balancing act gets interesting.

He can make money cheaper without cutting rates if he convinces investors that inflation is under control and that he is not Trump’s sock puppet, as many assume.

Or he can make money more expensive without hiking rates by scaring investors with his Fed reform plans and pandering to Trump.

So there may be a lot of hawkish comments today. But the real intention may not be to guide toward a much stricter policy but to control the term premium until inflation subsides.

- Dan Runkevicius, Editor

|

Five things to know before opening bell

🛢️ Oil sinks to three-month low

Crude prices continued to unwind after the U.S.-Iran peace deal, pushing Brent below $80 a barrel for the first time since early March. U.S. West Texas Intermediate fell nearly 5% to about $77 a barrel as traders priced in the prospect of additional Persian Gulf oil supplies returning to the market.

🚀 SpaceX takes over Cursor

Elon Musk’s SpaceX has agreed to acquire AI coding startup Cursor in a deal valuing the company at $60 billion. The transaction, expected to close in the third quarter, will give Cursor investors the option to receive SpaceX stock based on the startup’s equity value. The acquisition strengthens xAI’s coding capabilities as Musk looks to narrow the gap with AI rivals.

📈 Dow hits 52,000

The Dow Jones Industrial Average crossed 52,000 for the first time on Tuesday, outperforming a choppier broader market. Financials, industrials, and consumer staples led the advance, with JPMorgan, Home Depot, Caterpillar, and Procter & Gamble among the session’s biggest gainers as investors rotated into more defensive sectors.

💸 OpenAI’s losses multiply

OpenAI’s net losses increased eightfold in 2025 after the ChatGPT maker spent more than $34 billion on research, marketing, and other operating costs, according to the Financial Times. The figures underscore the enormous capital required to stay competitive in generative AI, suggesting that first-mover advantage may not guarantee a clear path to profitability.

🍕 Yum! Brands offloads Pizza Hut

Yum! Brands is selling Pizza Hut for $2.7 billion as it shifts its focus toward faster-growing chains KFC and Taco Bell. Private equity firm LongRange Capital will acquire the business outside China for $1.5 billion, while Yum China Holdings will purchase the remaining operations for $1.2 billion, marking the end of Pizza Hut’s decades-long run as one of the company’s flagship brands.

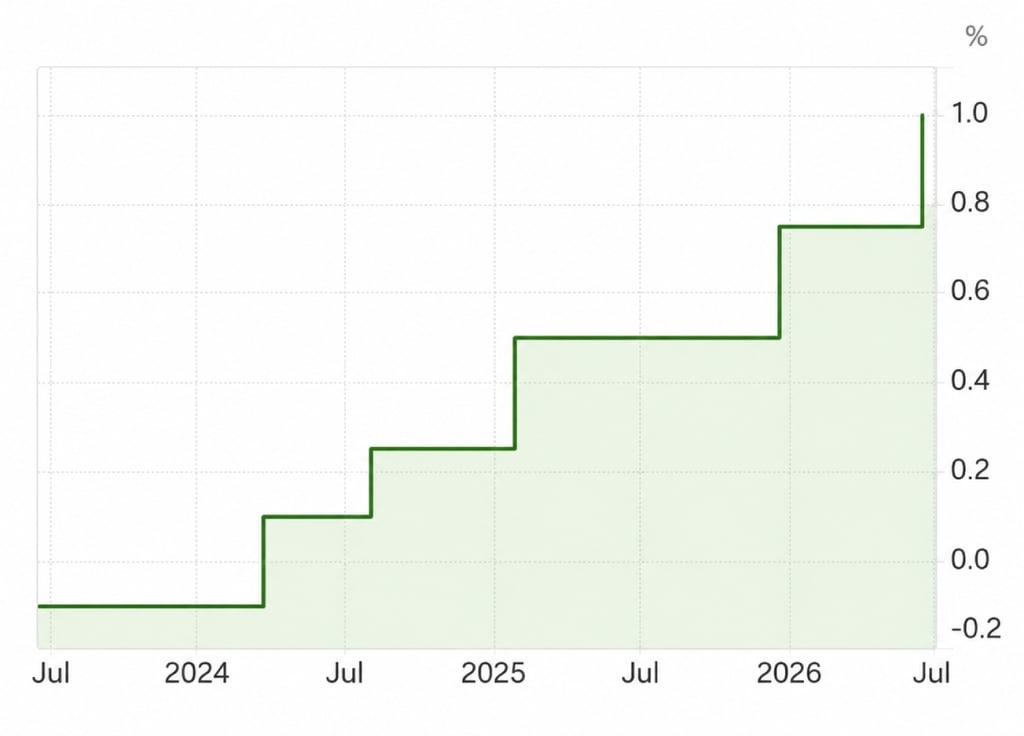

Why 1% rates in Japan could matter more than 5% in America

For decades, investors didn’t have to ask where to find cheap money. The answer was always Japan.

While the rest of the world chased growth and fought inflation, the Bank of Japan kept rates pinned near zero, quietly financing everything from U.S. Treasurys to tech stocks.

That assumption was tested on Tuesday, when the BoJ raised rates for the fifth time since 2024 and signaled that more hikes were on the way.

When 1% changes everything

On Tuesday, the BoJ raised its short-term rate to 1%, the highest in 31 years. Compared to Europe and the U.S., that’s still very low. But by Japanese standards, it’s a regime change.

The immediate casualty is the so-called yen carry trade: borrowing yen at almost no cost, converting it into dollars, and buying higher-yielding assets elsewhere.

For example, you could borrow 1 billion yen at 0.25%, convert it into dollars, and buy a U.S. Treasury yielding 4.5%. If exchange rates stay stable, you collect a spread of roughly 4.25% with relatively little effort.

For decades, the trade almost financed itself. But if borrowing costs rise and the yen strengthens, that math starts to break down.

The other side of the carry trade nobody talks about

The bigger story isn’t hedge funds closing positions. It’s Japanese investors deciding they no longer need to leave home in the first place.

The country’s pension funds, insurers, and asset managers collectively own trillions of dollars in overseas assets because domestic returns have been so low.

No one should expect trillions of dollars to flood back overnight. But even a gradual shift could take away important marginal buyers from U.S. assets, which have benefited for years from Japanese capital flight.

📌 Bottom line: If Japanese money starts staying at home instead of funding the rest of the world, the effects will be felt everywhere, from Treasury yields to tech stocks.

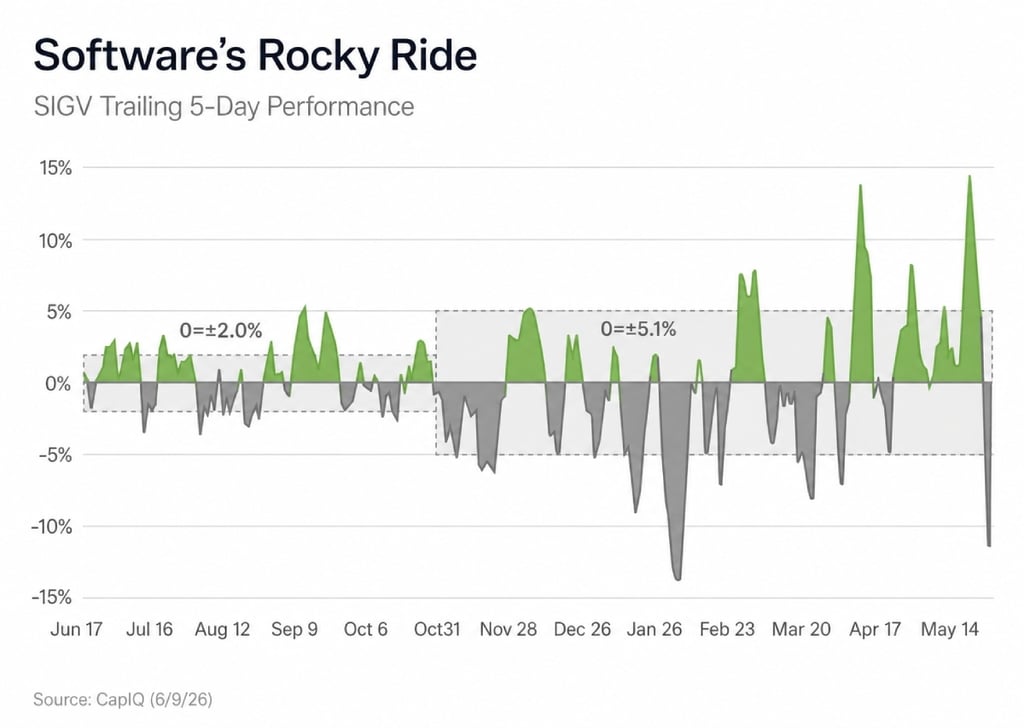

AI gave software stocks a biotech makeover

Software companies used to be some of the market’s most predictable businesses. They sold subscriptions, generated recurring revenue, and steadily grew earnings quarter after quarter.

Today, they’re trading more like biotech stocks as investors debate which companies AI will supercharge... and which it will replace.

AI broke the software playbook

Andreessen Horowitz looked at the performance of the iShares Expanded Tech-Software ETF (IGV) and found a striking shift.

From June through October, the fund’s rolling five-day moves stayed mostly within 2%. Since late October, that range has widened to roughly 5%, with repeated swings of 10% to 15% in either direction.

The market is trying to answer a simple question: Will AI make these software companies dramatically more valuable or completely replace them?

The result has been a series of violent “V-shaped” moves as investors repeatedly change their minds about the same companies:

- -6%, then +5%

- -9%, then +7%

- -14%, then +14%

- -11%, then +15%

Software falls out of favor

The irony is that software used to be one of Wall Street’s safest growth trades. Now it’s falling badly behind.

While the S&P 500 has climbed to multiple record highs this year, IGV is down roughly 15%. Meanwhile, the PHLX Semiconductor Index, a proxy for AI infrastructure spending, has surged 86%.

Institutional investors are positioning accordingly. By Goldman Sachs’ estimates, mutual funds ended the second quarter with their lowest software exposure since 2012.

📌 Bottom line: Before AI, investors could buy almost any software company and let the industry’s growth do the work. Now the sector is a mixed bag, and passive capital is fleeing.