End of S&P 500 as we know it

Morning Observers,

There are two main rules for a public company to get into the S&P indexes.

First, it has to make money. Before inclusion, the company must be profitable in both the most recent quarter and the sum of the past four quarters.

Second, it has to be public for at least one year (aka the “seasoning period”).

Both rules are going into the dumpster on June 8. After a recent consultation, S&P Dow Jones decided to waive the profitability requirement and cut the seasoning period to six months.

What's surprising is that this isn’t a universal rule. The waiver only applies to mega caps, most of which are Big Tech.

That means ETFs tracking S&P indexes could soon be forced to buy large, unprofitable tech companies. Those include the S&P 500, S&P MidCap 400, S&P SmallCap 600, S&P Composite 1500, and a few others.

What’s even more surprising is the timing. The rule will go into effect only days before SpaceX’s IPO. OpenAI and Anthropic could also get a shot at the waiver later this year.

This also comes after Nasdaq adopted its own “Fast Entry” rule in March, allowing large IPOs to enter the Nasdaq-100 after just 15 trading days. That rule became effective May 1.

That means many ETFs will soon be forced buyers of giant, unprofitable tech companies immediately after they go public.

Now all conspiracy theories aside, this move points to another big change in the market: This is the end of Big Tech as we know it.

For most of this century, Big Tech was a low-capex, high-margin sector that could grow fast, carry little debt, and consistently increase earnings.

AI broke that story. Now tech has little choice but to spend hundreds of billions just to keep up. Even Google is issuing equity and diluting shareholders to bankroll its AI infrastructure.

In other words, tech companies have gone from printing money to burning it. And index providers are likely adjusting in advance to keep passive ETF money flowing.

— Dan Runkevicius, Editor

Five things to know before opening bell

📈 Job openings surge, hiring slows

US job openings jumped by 731,000 to 7.6 million in April, their highest level in nearly two years, according to the latest JOLTS report. Hiring moved in the opposite direction, suggesting employers are still looking for workers but aren’t rushing to fill positions. The increase in openings also pushed available jobs above the number of unemployed Americans, which signals labor demand remains surprisingly strong despite a slowing economy.

💻 Tech lifts S&P 500 above 7,600

Tech stocks continue to power the market higher on Tuesday, lifting the S&P 500 above the 7,600 mark for the first time. Semiconductor companies led the gains, with the Philadelphia Semiconductor Index jumping more than 5%. The move underscores how enthusiasm around AI and Big Tech earnings outweighs concerns about inflation.

🛢️ Oil prices fall

Oil prices settled down on Tuesday after President Trump said he remains hopeful about reaching an interim peace agreement with Iran. The comments came after another weekend of strikes between the two sides that pushed crude higher. Brent crude trades near $95 a barrel while West Texas Intermediate hovers around the $96 mark.

🤖 OpenAI expands Codex beyond software development

OpenAI is broadening the reach of its Codex AI agent beyond programming, introducing new tools designed for professionals in fields such as investing, banking, and sales. The expansion is in response to AI providers scrambling to demonstrate real-world business applications. OpenAI also said additional capabilities targeting legal, finance, and other knowledge-based professions are expected soon.

🧾 US proposes new forced-labor tariffs

The US is proposing new tariffs of at least 10% on imports from 60 trading partners after an investigation into goods allegedly produced with forced labor. Canada, Mexico, the EU, Taiwan, and the UK would face a 10% tariff, while imports from China, India, Japan, South Korea, Brazil, and Switzerland would face a 12.5% levy. The tariffs won’t take effect immediately; written comments are due July 6, and public hearings begin July 7.

All-time illusion?

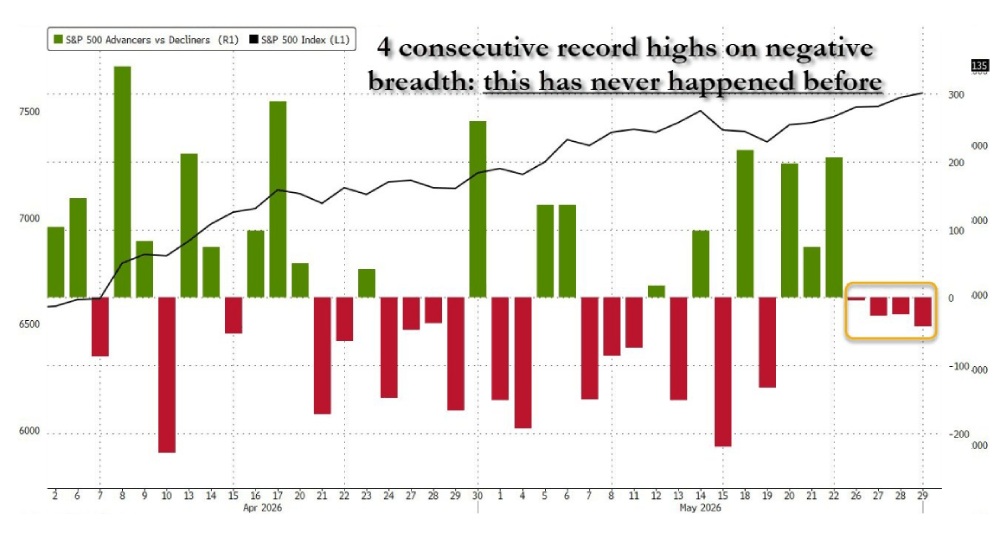

There has arguably never been a bigger disconnect between the S&P 500’s price and the performance of its members. The index keeps hitting record highs, but fewer and fewer stocks are helping it get there.

An all-time high, or an all-time illusion?

The S&P 500 is up roughly 19% from its March low, but an unusually small group of companies is responsible for much of the advance.

Only 21 stocks also reached new highs when the index hit a fresh record last week. That’s less than 5% of the index.

For comparison, just 20 stocks made new highs when the S&P 500 peaked in March 2000, shortly before the dot-com bubble burst. But the divergence doesn’t stop there.

Last week, the S&P 500 posted four consecutive record highs even though more stocks fell than rose each day. That level of negative market breadth had never happened before.

In other words, investors are buying the same handful of stocks, many of which are tied to AI.

The market has never looked more expensive

Normally, concentration becomes less concerning when valuations are reasonable. Today’s market has the opposite problem.

Bloomberg recently combined several valuation measures, including price-to-earnings ratios, price-to-sales ratios, and market-cap-to-GDP. And the result was striking.

U.S. stocks are no more expensive than they were at the peak of the dot-com bubble and even the 1929 market top before the Great Depression.

That doesn’t mean a crash is imminent.

Expensive markets can stay expensive for years, especially when investors believe a transformative technology is rewriting the economy. That’s the argument many bulls are making about AI today.

What's unusual this time is that investors are paying record prices for an increasingly narrow market.

📌 Bottom line: The AI trade is no longer confined to a handful of stocks. It's increasingly driving the performance of index funds, pension funds, and retirement accounts. Whether investors realize it or not, many are making the same bet.

Gold has quietly replaced Treasurys

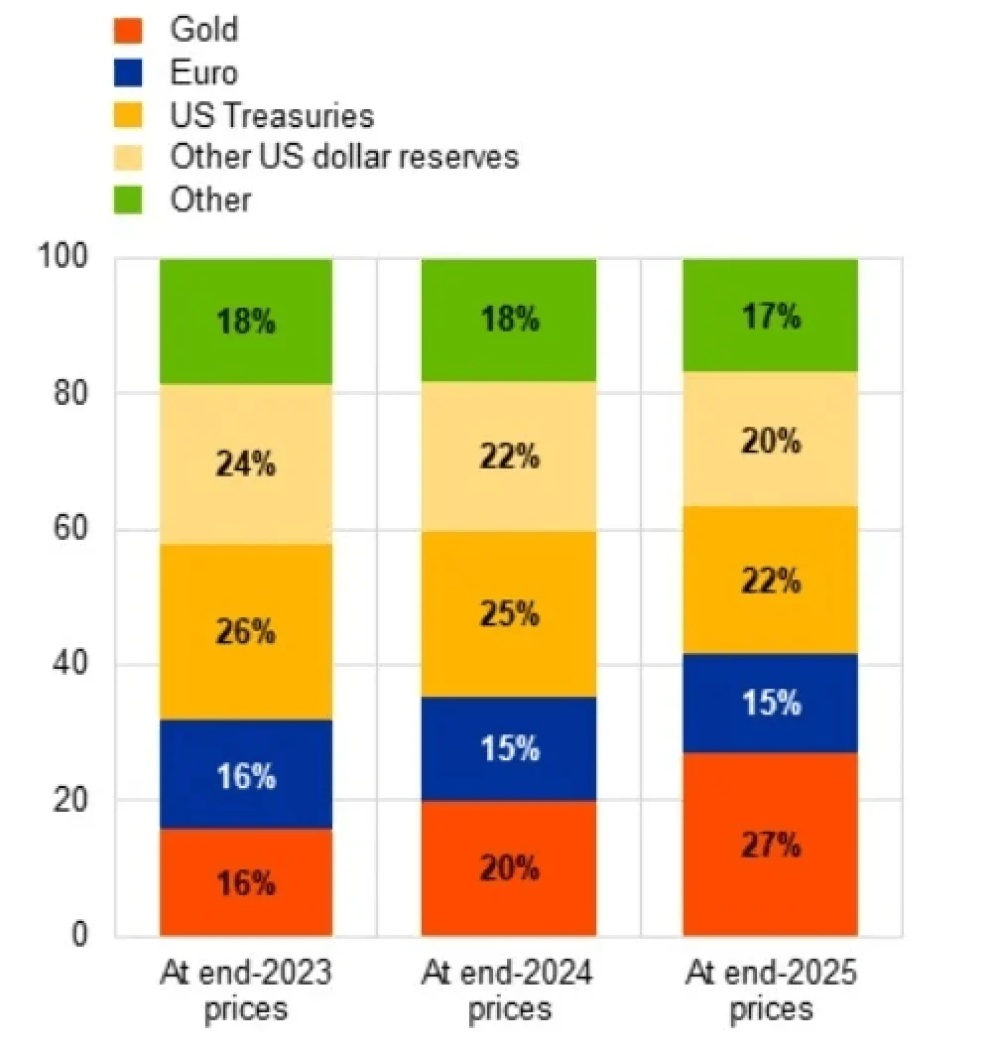

For 50 years, central banks swapped gold for U.S. debt. Now they’re starting to swap back. Although the U.S. dollar remains the world’s reserve currency, gold has quietly become the largest reserve asset.

Not since Bretton Woods

According to new European Central Bank data, gold accounted for more than 27% of global foreign reserves at the end of 2025, surpassing U.S. Treasury bonds and other dollar-denominated reserve assets.

In dollar terms, central banks now hold roughly $4 trillion worth of gold.

The last time governments accumulated gold this aggressively was during the Bretton Woods era, when currencies were directly linked to the metal and gold sat at the center of the global financial system.

That system died in 1971. For the next half-century, reserve managers piled into dollars.

That trend is starting to reverse again. Foreign investors still hold a massive pile of U.S. Treasurys, but their share of America’s debt has been shrinking for years.

Foreign accounts now hold roughly 30% of publicly held U.S. debt, down from nearly 50% in the early 2010s, according to the Bipartisan Policy Center.

That matters because weaker end-investor demand can force primary dealers to absorb more Treasury issuance at auction.

The trust test

Gold’s rally explains part of the shift, but the buying started long before the latest surge. Central banks have been net buyers for years, especially since Russia’s invasion of Ukraine.

The biggest buyers are countries trying to reduce their exposure to geopolitical risk, including China, Poland, Kazakhstan, Brazil, and Turkey.

That’s where gold comes in. There is no government behind it. It can’t be sanctioned, frozen, or inflated away by another country’s central bank.

In a world that's becoming less cooperative and more fragmented, that matters because reserve managers are increasingly favoring assets that don’t depend on another government’s promises.

📌 Bottom line: If central banks keep shifting reserves out of Treasurys, Washington will eventually have to offer higher yields to attract buyers. That means higher borrowing costs not just for the government, but for households and businesses too.