Amazon's quiet AI warning

Morning Observers,

On July 7, Amazon flashed an AI warning, but few investors noticed because it had nothing to do with its stock.

After raising $37 billion in debt just four months earlier, the company unexpectedly returned to the market with an additional $25 billion bond sale to finance its AI spending.

But the market pushed back.

BofA reported that Amazon had to offer an additional 18–21 basis points of yield to sell its longer-term bonds. And struggling to raise cash, investors had to sell other bonds to make room for Amazon’s new debt.

Even then, it was the weakest new debt issuance by a hyperscaler since Meta’s $30 billion sale in October 2025.

So why are hyperscalers having a harder time raising debt? Two things.

The first is supply and demand. Hyperscalers are flooding the debt market with unprecedented amounts of new issuance.

This year alone, big tech has raised $270 billion in debt, nearly double the amount raised over the same period last year. And last year was roughly five times higher than the year before.

This snowball of paper is hitting the market all at once, and investors simply are not raising cash fast enough.

The second reason is that investors are seriously questioning the economics of AI spending.

Hyperscaler free cash flow is basically gone, and nobody yet knows how those hundreds of billions of dollars will ultimately pay off.

One good representation of this concern is the difference in 10-year versus 30-year spreads between hyperscalers and other issuers.

In plain English, the difference shows how much additional yield investors are demanding to hold a hyperscaler’s 30-year bond vs its 10-year bond compared with companies in other industries.

That gap is now at its widest since the AI debt issuance boom began.

This may be the best proxy for what investors really think about AI spending because the bond market is ultimately about financial discipline. And a 30-year lender in particular has to price in everything.

They’re considering things like how quickly GPUs and networking equipment will become obsolete, whether AI-driven productivity gains and commoditization will destroy hyperscaler pricing power, and how much refinancing will be required before the original assets have paid for themselves.

Oracle is the first canary in the coal mine for what happens when spending goes out of hand.

On July 9, the company was downgraded to just one notch above speculative grade. S&P said AI spending is diluting Oracle's core business and that it had underestimated how much investment this would require.

What all this says is that the most pragmatic market is already pushing back against AI spending. Whether the stock market will follow suit remains to be seen.

Let's dig in!

- Dan Runkevicius, Editor

|

|

🚀 SpaceX is coming for Big Telecom

Bernstein analysts lowered their price targets on AT&T, T-Mobile, and Verizon by 10% to 17%, arguing that Elon Musk’s SpaceX is becoming a bigger competitive threat. The firm noted that roughly 70% of SpaceX’s revenue now comes from Starlink, underscoring how the satellite broadband service is expanding into markets long dominated by traditional wireless carriers.

🚢 Hormuz’s alternative shipping route remains open

Iran has again moved to block transit through the Strait of Hormuz, though the Joint Maritime Information Center said the critical shipping lane remains open via the southern route along the Omani coastline. The agency nevertheless rated the threat level as “severe,” with vessels slowing their transit and commodity markets beginning to re-price supply shortages.

🏰 Wells Fargo’s fix for Disney

Disney stock has lagged for years despite record box office results and packed theme parks. In a recent analyst note, Wells Fargo said streaming is the company’s biggest drag. The bank estimates that spinning it off or exiting streaming could unlock 40% upside in the stock by allowing investors to better value Disney’s intellectual property and experiences segments.

💾 TSMC reinforces the AI story

Taiwan Semiconductor Manufacturing Co., the world’s largest contract chipmaker and the primary manufacturer of Nvidia’s AI chips, reported a 36% jump in quarterly sales, reinforcing expectations that global AI demand remains strong. The results reinforce the case for Big Tech’s planned $725 billion in AI spending this year, even though investors debate whether the industry is overbuilding.

🪙 China could provide a floor for gold prices

Gold has pulled back toward the $4,000 level, but China’s central bank is accelerating its purchases. Monthly buying has climbed from around 5 metric tons to 15 metric tons in recent months, the fastest pace since early 2024, potentially providing a floor for prices.

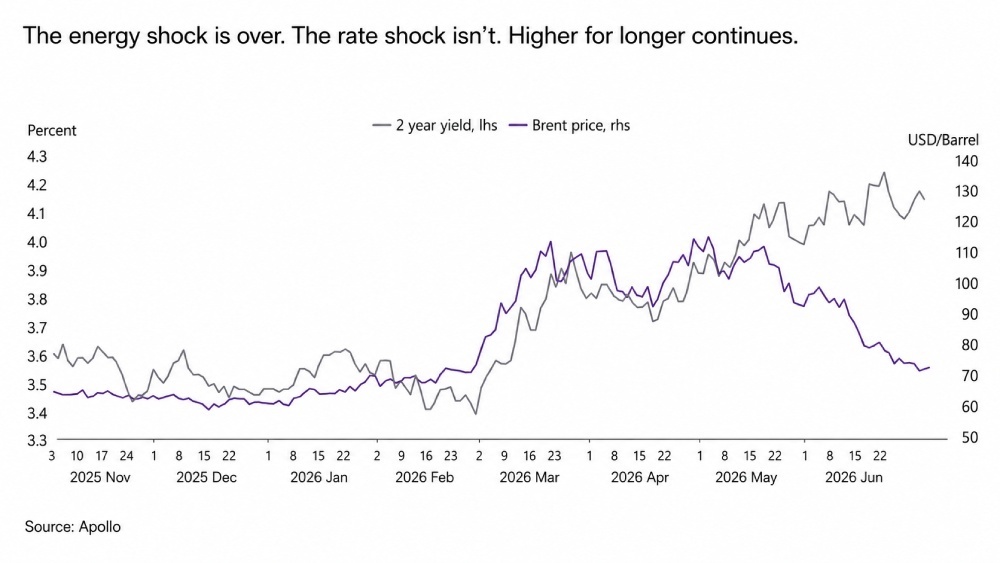

Bond investors just broke one of the oldest inflation patterns

Falling oil prices used to bring down bond yields. This time, cheaper oil is no longer translating into lower Treasury yields simply because investors are not convinced it will solve the inflation problem.

Why cheaper oil isn’t enough

While Brent crude prices have fallen from their May peak, 2-year Treasury yields have remained firmly in place, suggesting markets no longer view energy as the primary inflation risk.

Instead, investors expect inflation outside food and energy, driven by tariffs, strong hiring, and services such as housing, healthcare, and insurance, to keep price pressures elevated.

The implication is that lower oil prices alone are unlikely to pave the way for rate cuts until the Fed sees broader evidence that underlying inflation is cooling.

Apollo chief economist Torsten Slok calls this the “decoupling.” His point is that the Fed now cares less about gasoline prices and more about core inflation.

FOMC minutes highlight the Fed’s divide

Last week’s FOMC minutes reflected that uncertainty. They showed that policymakers still expect inflation to cool, but there is little agreement on when interest rates can come down.

Some officials expect modest rate cuts, while others believe rates may need to remain higher for longer. The disagreement highlights how uncertain the inflation outlook remains.

📌 Bottom line: Oil prices are no longer the main driver of inflation expectations. All eyes are now on core inflation, which reveals how tariffs and the fallout from Hormuz are spreading through the broader economy.

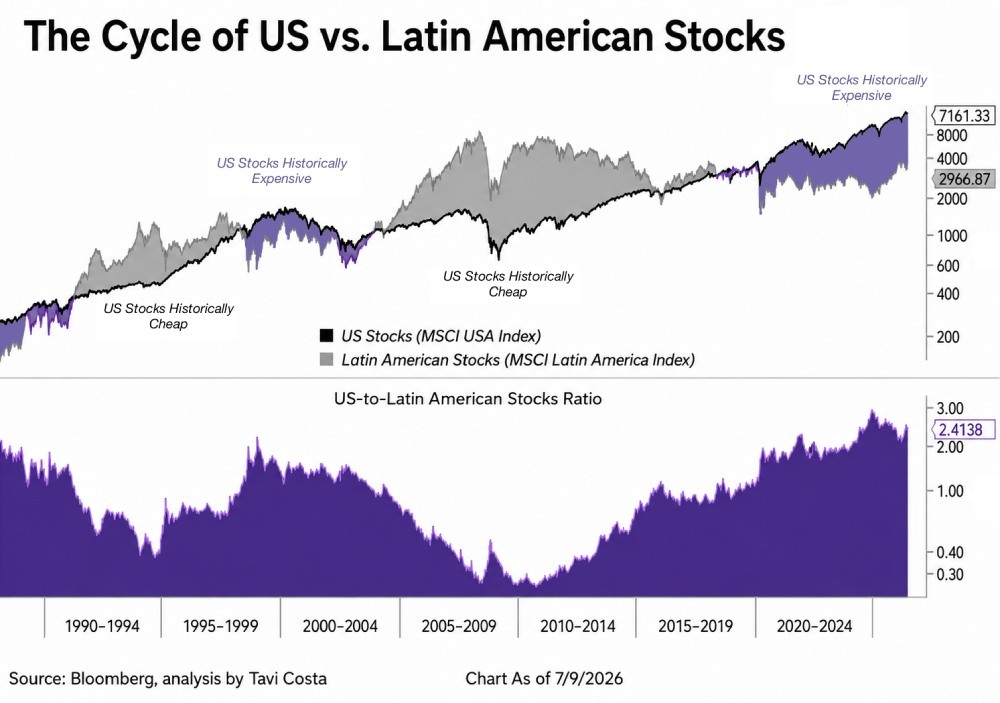

Latin America and the 35-year market rule

With U.S stocks increasingly concentrated around AI, investors are beginning to ask whether emerging markets now offer a more attractive risk-reward tradeoff.

History suggests the next region to outperform U.S. stocks could be Latin America.

The forgotten cycle

Over the past 35 years, U.S. and Latin American stocks have repeatedly taken turns outperforming each other.

The MSCI Latin America Index outperformed during the early 1990s and again throughout much of the 2000s, while the MSCI USA Index dominated after the dot-com boom and for most of the past 15 years, driven first by technology and more recently by AI.

That long stretch of U.S. dominance has left one of the widest valuation gaps in decades. Even after Latin America’s recent rally, its stocks remain far cheaper than their U.S. counterparts.

Unlike the U.S., where technology dominates stock indexes, the MSCI Latin America Index is concentrated in banks, energy producers, and mining companies.

Those sectors tend to benefit from economic growth, higher commodity prices, and rising demand for raw materials.

AI needs Latin America

Data centers, power grids, electric vehicles, and semiconductors all require enormous amounts of copper and lithium. Latin America is one of the world’s richest sources of both.

“Commodities were a big part of the fuel behind the rally in Latin American equity markets,” said Pedro Fabregat, an analyst at INCA Investments, who expects investment in the region to remain strong as demand for data center infrastructure continues to grow.

The turnaround is already underway. The MSCI Latin America Index returned 56% in 2025 and another 15% during the first quarter of this year in U.S. dollar terms.

📌 Bottom line: The MSCI Latin America Index could be entering a new period of outperformance after spending much of the past 15 years trailing U.S. stocks.