Alphabet just made history

Morning Observers,

Alphabet just made history with one of the biggest financing moves in the AI arms race.

The tech giant is raising $80 billion through a series of equity offerings. And what’s especially surprising is that Berkshire Hathaway will lead the charge, chipping in $10 billion of the total.

The surprising part is not so much the amount as the fact that Berkshire has largely been a naysayer on AI.

The only exception was Alphabet, which Buffett started building a position in last year. This $10 billion deal will increase Berkshire’s Alphabet position to 10% of its portfolio.

That means two things. The legend of value investing isn’t shying away from AI even at this point, but they are backing just one company: Alphabet. And not without reason.

Let’s start with data. Alphabet has something no AI startup and very few tech giants can replicate: a built-in audience of 4 billion people.

Every single day, these people feed Alphabet an unmatched stream of real-world behavioral data, teaching its models how people search, navigate, communicate, and reason at scale.

No standalone AI lab comes close to that advantage.

Then there’s software. Google’s early large language models, or LLMs, were, frankly, a joke. And for a while, Wall Street wrote the company off as the Kodak of AI. That story broke with Gemini.

By many benchmarks, Gemini is now one of the top reasoning models out there, beating even OpenAI’s latest releases. And Apple, which is by far the most important consumer hardware company in the world, is already working it into Siri.

But Alphabet’s biggest edge by far is hardware.

NVIDIA’s GPUs have been the default hardware for training and running large AI models. Companies like Anthropic and xAI trained their frontier models on GPUs because they’re flexible and general-purpose.

That versatility is why Nvidia became the industry standard.

Google took a different approach. More than a decade ago, Alphabet began building its own chips, Tensor Processing Units, or TPUs, designed specifically for AI.

They aren’t general-purpose like GPUs, but they are highly optimized for the kinds of models Alphabet builds and deploys internally.

Anthropic, Midjourney, and Salesforce are already training and running models on Google’s TPUs. But no large language model is better suited to that hardware than Gemini itself.

This is why Alphabet has such a massive moat in the AI race. It owns the data, the software, the distribution, and the silicon powering the AI revolution.

And that kind of vertical integration may be worth much more than the company is worth today.

— Dan Runkevicius, Editor

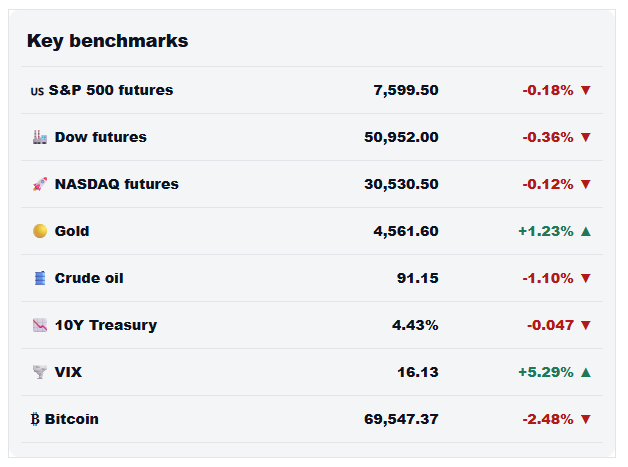

Five things to know before opening bell

🛢️ Oil surges as U.S.-Iran tensions flare up again

Oil prices surged more than 6% Monday after the U.S. and Iran exchanged strikes over the weekend, reversing expectations that the two sides were moving toward a ceasefire. Iran subsequently suspended talks with Washington, raising doubts about whether commercial traffic through the Strait of Hormuz can resume.

🏭 U.S. manufacturing activity reaches a four-year high

U.S. manufacturing expanded at its fastest pace in four years in May, largely thanks to businesses front-loading orders ahead of anticipated price increases and supply shortages. The Institute for Supply Management’s manufacturing PMI rose to 54 from 52.7 in April, marking its highest reading since 2022. Any reading above 50 signals expansion.

💻 Nvidia takes aim at Intel with new AI PC chips

Nvidia is making a major push into the PC market with a new generation of AI-powered processors designed for laptops and desktops. CEO Jensen Huang said the company’s RTX Spark Superchip will begin appearing in devices from manufacturers including Dell and Lenovo later this year. Investors took the announcement as a direct challenge to Intel’s longtime leadership in PCs, sending Intel shares lower.

🏦 Glenmede says the Fed’s next move could be a rate hike

Investment and wealth management firm Glenmede warned that the Iran war could complicate the inflation outlook and further diminish the odds of near-term rate cuts. The firm said higher energy prices could eventually push the Fed toward another rate hike, adding to a growing chorus of analysts who believe the next move may not be a cut after all.

🤖 Anthropic files for IPO

Anthropic, the developer of the Claude family of AI models valued at $965 billion, has officially filed for an initial public offering, setting the stage for a closely watched market debut later this fall. The company joins OpenAI and SpaceX, also pursuing paths to raise more money in the public markets.

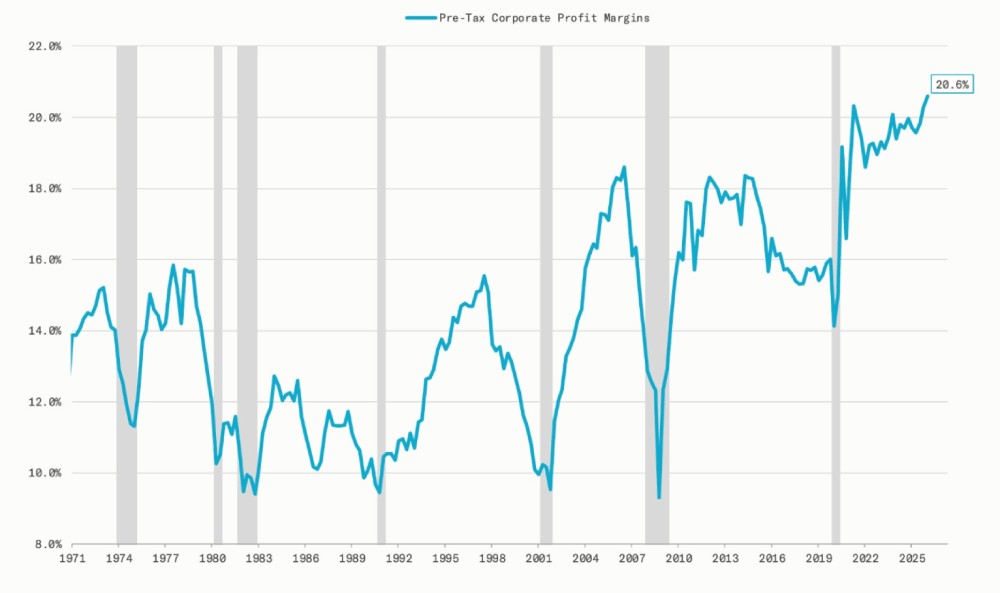

America’s new wealth divide

Americans spent the last four years complaining about inflation. Corporate America spent the last four years cashing in on it, with profit margins climbing to their highest level on record.

And because those profits mostly end up in the pockets of people who already own stocks, the surge is quietly widening America’s wealth divide.

The old ceiling is gone

For most of the last half-century, corporate profit margins followed a pretty reliable pattern.

According to EPB Research, economy-wide pre-tax profit margins usually hovered in a range of roughly 10% to 16%, no matter what was happening in the economy.

Then the pandemic broke the pattern.

Margins have now surged to 20.6%, smashing through a ceiling that held for decades. “The old ceiling looks gone for good,” EPB founder Eric Basmajian wrote.

A big part of that surge appears to be tied to the post-pandemic inflation shock.

Research from the Economic Policy Institute found that rising corporate profits accounted for more than 40% of price growth between the end of 2019 and mid-2022, compared with a historical norm closer to 11% or 12%.

In plain English, corporations weren’t just victims of inflation. In many cases, they helped drive it.

The people paying for inflation don’t benefit from it

Record profits would matter less if the gains were spread around more evenly, but they’re not.

When companies raise prices and protect their margins, shareholders benefit through higher earnings, rising stock prices, and buybacks.

On the other end are consumers, who pay the bill through groceries, rent, insurance, cars, and basically every other part of daily life. And increasingly, those are not the same people.

America’s wealthiest households own the vast majority of financial assets, with the top 10% holding more than two-thirds of the country’s wealth.

Meanwhile, Bank of America data shows that wage growth for higher-income households has been roughly double that of middle- and lower-income households.

The result is a form of inequality that gets far less attention than income inequality: ownership inequality.

📌 Bottom line: If the old profit ceiling is truly gone, the biggest divide in America may not be between workers and corporations, but between those who own assets and those who don’t.

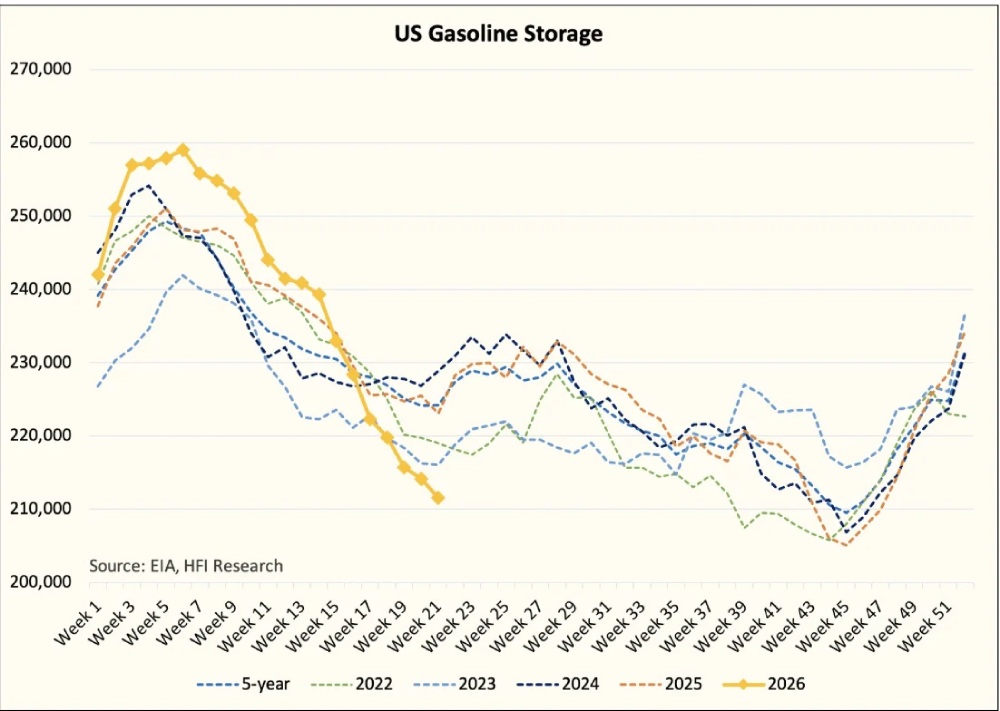

We got 1970s oil shocks all wrong

While governments are releasing emergency oil reserves to prevent an energy crisis, the reality is that they may be making one more likely...

The lesson from the 1970s wasn’t what most people think

Many Americans remember the oil embargo. Others read about it in textbooks. Either way, Ross Hendricks of Stansberry Research thinks most people have the story backward.

His argument is that the infamous gas lines of the 1970s weren’t caused by the OPEC oil embargo alone. They were made worse by policies that prevented prices from rising enough to balance supply and demand.

Cheap fuel encouraged consumption even as inventories were being drained. Eventually, shortages showed up in the real world.

“The artificially suppressed price led to excess consumption relative to supply, which ultimately gave rise to physical shortages,” Hendricks wrote.

Inventories are getting dangerously thin

Governments may be repeating the same mistake and the warning signs are already here.

U.S. distillate inventories recently fell below 101 million barrels, their lowest level in more than two decades. Gasoline inventories have plunged for 15 consecutive weeks, according to EIA data.

According to HFI Research, U.S. fuel inventories are now within 9 million barrels of what amounts to a paycheck-to-paycheck level, leaving almost no buffer if another supply disruption hits.

At that point, the system becomes fragile.

A refinery outage, weather event, or shipping disruption that would normally be manageable can suddenly create visible shortages and long queues at the gas station, HFI said.

📌 Bottom line: If inventories keep falling, that’s the part of 1970s oil-shock history investors should be paying attention to.