AI equity supply shock

Morning Observers,

Last Friday, Trump said that the U.S. government may invest in some AI software giants, including OpenAI, Anthropic, and xAI. This follows Bernie Sanders’ idea to take 50% equity stake in AI companies and create a sovereign wealth fund.

Seems like a wholesome bipartisan effort, but the brainchild behind this move is none other than one of the companies at the receiving end of it: OpenAI.

Both WSJ and FT verified that Sam Altman had been privately lobbying for a government ownership stake in AI companies and that he himself came up with the wealth fund idea.

Now you can make an argument that nationalizing AI companies is the only way to compete in the AI arms race with a communist superpower like China, and that the means justify the cause.

But AI is not a case of national security.

AI software giants like OpenAI are becoming a commodity. We have a dozen comparably good LLMs in the West, which are only a couple of months of R&D apart, and China is already opening the floodgates with open-source models.

So xAI, Anthropic, and OpenAI have little to do with China.

Nor does it have anything to do with redistribution of wealth because, if anything, all these companies are losing billions and have no idea how to turn a profit.

So what is a plausible explanation for federal intervention in increasingly commoditized AI models?

A probable lack of capital in what's going to be a make-or-break year for AI IPOs.

The problem is not so much that investors don’t want to put money into AI. It’s that all these companies are scrambling to raise historically large sums at sky-high valuations at the same time.

- SpaceX/xAI IPO — $75B at ~$1.7T valuation

- OpenAI — $60B+ on the low end at ~$1T valuation

- Anthropic IPO — $65B+ based on last round at ~$1T valuation

- Alphabet Inc. equity raise — $80B

That’s on top of hyperscalers also raising debt to fund AI infrastructure. So the concern is whether there is enough appetite for all this new equity.

If a sovereign wealth fund buys half of your equity, not only is half of your demand virtually guaranteed, but it also creates hype that can pull in even more private capital.

A good example is Intel. Since the federal equity stake announcement last year, Intel has gone up about 300%, while its top line and bottom line barely budged.

But is a company expected to burn through $115 billion through 2029, and whose model is set to be commoditized and even potentially replaced by Chinese open source, a good investment for American taxpayers?

That’s a hard case to make.

- Dan Runkevicius, Editor

Five things to know before opening bell

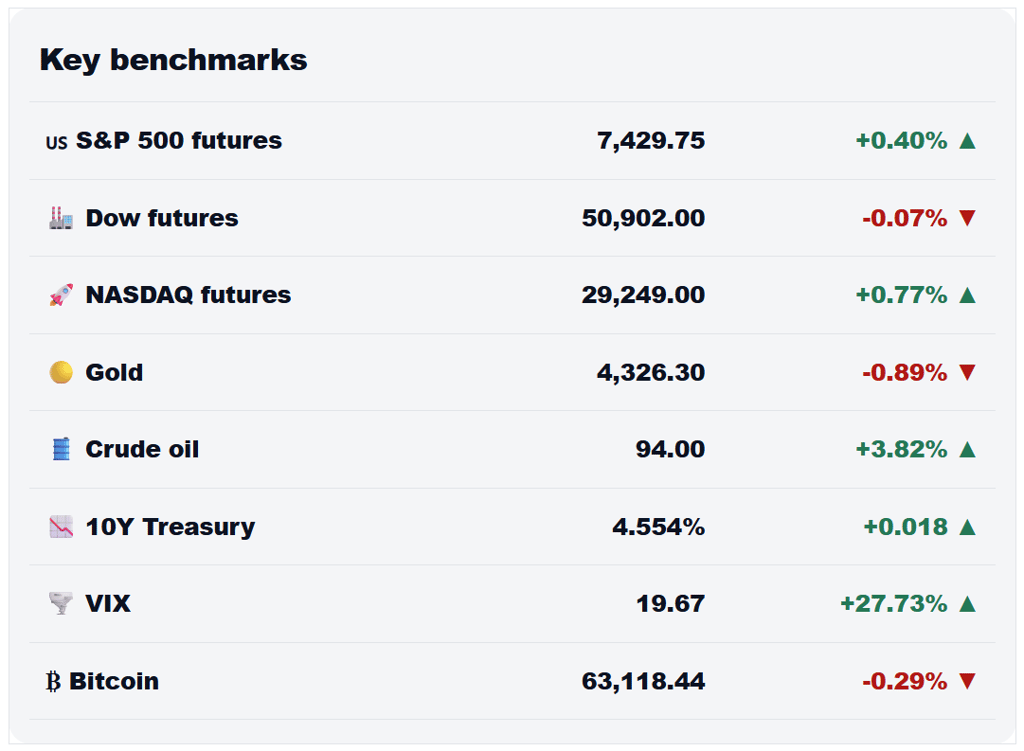

📉 S&P 500 snaps nine-week winning streak

A selloff in technology stocks on Friday dragged the S&P 500 lower for the week, ending a remarkable nine-week winning streak that was one of the longest stretches of gains in recent memory. The benchmark index has still rallied more than 19% from its March lows and remains firmly higher for the year, but the strength of the rebound appears to be triggering profit-taking, especially in the semiconductor industry.

💼 Nonfarm payrolls shatter expectations

The U.S. economy added 172,000 jobs last month, nearly double economists’ expectations, while April payroll growth was revised higher by 64,000 to 179,000. The unemployment rate held steady at 4.3%, reinforcing signs that the labor market is picking up. The report is another sign of reflation, with both the economy and inflation continuing to grow.

🏦 Fed rate hike bets grow

Investors are becoming increasingly convinced that the Federal Reserve’s next move could be a rate hike rather than a cut. According to Bloomberg data, swap markets are now pricing in a rate increase before year-end, while Fed funds futures imply a 63% chance of a hike by October and nearly a 96% probability by December.

📈 Treasury yields spike

Expectations for higher interest rates pushed Treasury yields higher at the end of last week, with the 10-year Treasury yield rising more than 6 basis points to 4.54% and the 2-year yield climbing 12 basis points to 4.16%. Higher yields make borrowing more expensive across the economy and could weigh on valuations.

🚀 SpaceX IPO hysteria begins

Demand for SpaceX’s $75 billion IPO, which is set to become the largest public offering in history, is already exceeding available shares, according to Bloomberg sources. Elon Musk said the company is seeking a valuation of roughly $1.8 trillion, a figure that would place the space and AI giant among the world’s 10 most valuable publicly traded companies.

Is the economy running on panic buying?

For months, investors have pointed to rising PMI surveys as evidence that the U.S. economy is still growing. But that may be the wrong conclusion.

A closer look suggests businesses aren’t so much responding to stronger demand as preparing for higher costs and looking for ways to pass more of them on to consumers.

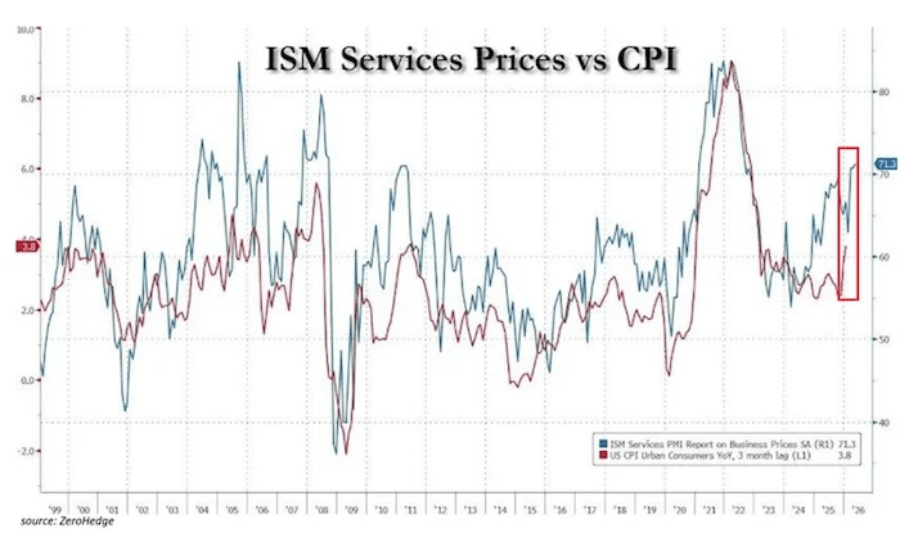

Inflation warning hiding in plain sight

The latest ISM Services PMI rose to 54.5 in May, comfortably above the 50 level that separates growth from contraction. At first glance, that’s good news.

The problem is that the survey’s prices index rose to 71.3, its highest level since August 2022. Since February, it has surged 8.3 points, marking the largest three-month increase since the inflation shock of 2021.

Businesses cited diesel, gasoline, oil, and other energy-related inputs as some of the fastest-rising costs.

Historically, increases in service prices have preceded higher CPI readings by roughly three months. If that relationship holds, inflation may be far less contained than recent data suggests.

Growth today, inflation tomorrow?

The manufacturing data tells a similar story. ISM’s Manufacturing PMI jumped to 54 in May from 52.7, its highest level in four years.

While factory activity has improved, much of it appears to be driven by managers pulling orders forward and stocking shelves in anticipation of supply disruptions and higher costs.

As Trepp chief economist Rachel Szymanski recently said, manufacturers aren’t building new factories or ramping up investment. They’re mostly buying more stuff.

That means businesses aren’t behaving like they expect a boom. Companies preparing for stronger demand build factories. Companies preparing for higher prices fill warehouses, which is what appears to be happening right now.

📌 Bottom line: If PMIs are rising because companies are rushing to buy before prices climb further, today’s growth may be foreshadowing tomorrow’s inflation.

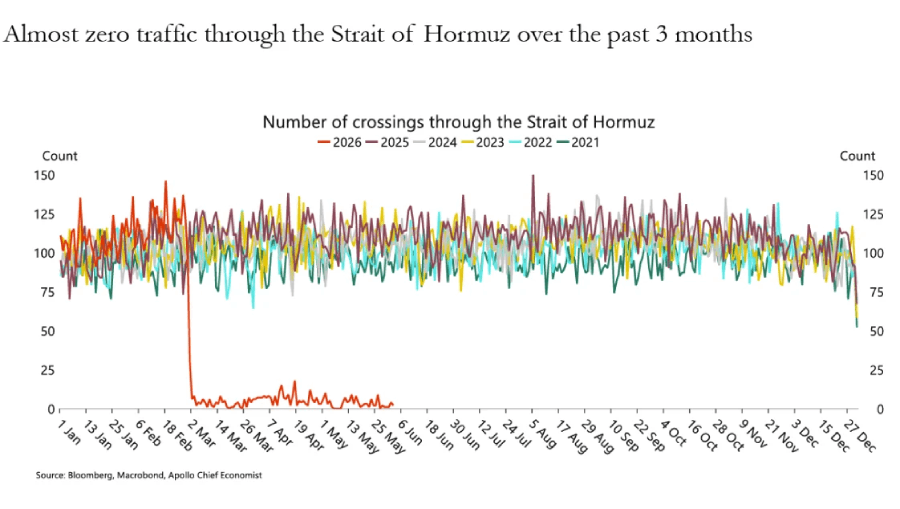

What happens if Hormuz never returns to normal?

Many investors assume shipping through the Strait of Hormuz will return to normal once the Iran war ends. History suggests it won’t be that simple.

The Red Sea says don’t expect a comeback

After Houthi attacks disrupted shipping in the Red Sea in early 2024, vessel traffic collapsed. More than two years later, traffic remains nowhere near pre-crisis levels.

After averaging more than 70 crossings per day, Red Sea traffic is now running at less than half that level, according to UN and IMF data.

Hormuz matters far more than the Red Sea.

Washington has largely avoided the worst of the oil shock so far, but the effects are already showing up in imported products such as aluminum, pharmaceutical ingredients, and petrochemical feedstocks.

A supply chain problem disguised as a shipping problem

There’s a bigger problem than the energy crunch.

When ships stop moving, inventories stop moving with them. Companies are forced to carry larger safety buffers, tie up more money in stockpiles, and wait longer to get paid.

One way to see this is through inventory-to-sales ratios, which measure how much inventory businesses hold relative to what they’re selling. According to Apollo, that ratio has collapsed, suggesting businesses are selling inventory faster than they can reliably replace it.

Eventually, those inventories have to be rebuilt. That requires working capital, cash tied up in inventory, supplier payments, and day-to-day operations.

According to Apollo chief economist Torsten Slok, a partial reopening of Hormuz could require roughly $35 billion in additional working capital across the global economy.

If traffic never returns to normal, that figure could rise toward $80 billion.

📌 Bottom line: Investors are focused on whether Hormuz reopens. The more important question is whether shipping companies ever trust it again. If the Red Sea is any guide, the real cost will be tens of billions in extra working capital.